Commercial auto fleet insurance setup is the process of organizing required documentation, selecting appropriate coverage types, and submitting a complete application to secure insurance for your business vehicles. Personal auto insurance does not cover commercial use of vehicles, making a dedicated commercial policy non-negotiable for any business operating a fleet. Whether you run five delivery vans or fifty long-haul trucks, the right policy protects your assets, satisfies legal requirements, and limits your liability exposure. This guide walks you through every step, from gathering documents to binding coverage.

What documents do you need for commercial auto fleet insurance setup?

Preparation is the single biggest factor in how fast your policy gets bound. Missing loss runs are the number one cause of underwriting delays during commercial auto insurance setup. That means the work you do before you contact an insurer directly determines how quickly your fleet gets covered.

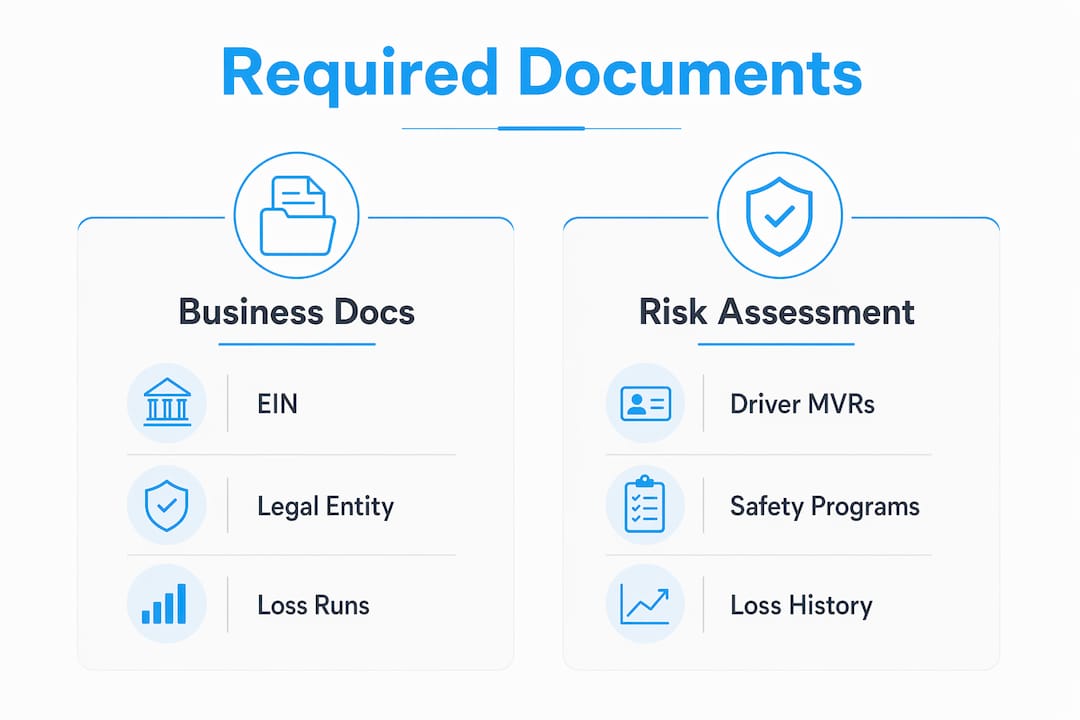

Organize your documentation into four categories before you submit anything:

Business documents:

- Employer Identification Number (EIN) and legal entity formation documents

- State business licenses and operating authority certificates

- USDOT number and MC number for regulated motor carriers

- Cargo type descriptions and haul radius details

Vehicle information (for each unit in the fleet):

- Vehicle Identification Number (VIN), year, make, and model

- Current title and registration

- Stated value or replacement cost for physical damage coverage

- Any vehicle modifications or specialized equipment

Driver information:

- Valid commercial driver’s licenses (CDL or standard, depending on vehicle class)

- Motor Vehicle Records (MVRs) for every driver, pulled within the last 12 months

- Driver history including accidents, violations, and claims

Loss history:

- Five years of loss runs from your current or prior insurer

- Documentation of any open claims and their current status

| Document Category | Why Underwriters Need It |

|---|---|

| EIN and legal entity docs | Confirms business structure and ownership for policy issuance |

| VIN and vehicle schedule | Establishes the exact units being insured and their replacement values |

| Driver MVRs | Assesses individual driver risk, which directly affects premium |

| 3-5 years of loss runs | Shows claims history and helps underwriters price the risk accurately |

| USDOT / MC numbers | Required for regulated carriers to verify operating authority |

Pro Tip: Request your loss runs from your current insurer at least 30 days before your renewal or new application date. Insurers are legally required to provide them, but processing can take time. Having them ready eliminates the most common underwriting bottleneck.

Underwriters pull driver MVRs, loss history, and safety program documentation to assess risk before quoting. A clean, organized submission package signals a well-managed fleet and often results in better pricing.

Which coverage types belong in a commercial fleet policy?

Fleet insurance is a stack of coverages including liability, physical damage, and cargo, which vary based on your FMCSA authority and the type of cargo you haul. Understanding each layer helps you build a policy that actually covers your exposures rather than leaving gaps.

Core coverages every fleet needs:

- Commercial auto liability: Covers bodily injury and property damage you cause to others. This is the legal minimum and the foundation of any fleet policy.

- Physical damage (comprehensive and collision): Covers damage to your own vehicles from accidents, theft, weather, and other perils.

- Uninsured/underinsured motorist: Protects your drivers when the at-fault party has no insurance or insufficient coverage.

- Medical payments or personal injury protection (PIP): Covers medical costs for your drivers regardless of fault, depending on your state.

Specialty coverages based on your operation:

- Cargo insurance: Required if you haul freight for others. Covers loss or damage to the goods in transit.

- Bobtail and non-trucking liability (NTL): Covers owner-operators when driving without a load or outside of dispatch.

- Occupational accident insurance: A cost-effective alternative to workers’ compensation for owner-operators classified as independent contractors.

FMCSA requires motor carriers to carry minimum financial responsibility limits of $750,000 for general freight, $1,000,000 for oil and hazardous materials, and $5,000,000 for certain hazmat loads. Most brokers and shippers push carriers to carry $1,000,000 to $5,000,000 in combined liability limits regardless of cargo type. Meeting the minimum keeps you legal. Meeting shipper requirements keeps you working.

For businesses wondering about the difference between personal and commercial coverage, this breakdown of commercial vs. personal auto policies clarifies exactly where personal coverage ends and commercial coverage begins.

Comparison: traditional fleet insurance vs. self-insurance

| Factor | Traditional Fleet Insurance | Self-Insurance Program |

|---|---|---|

| Who pays claims | Insurer | Business from its own reserves |

| Best for | Fleets of any size | Large fleets with strong cash flow |

| Regulatory approval | Standard licensing | State approval and financial proof required |

| Premium flexibility | Market-driven | Controlled by internal loss experience |

| Setup complexity | Moderate | High |

Large fleets often consider self-insurance programs once they meet state thresholds for financial ability. Self-insurance works best for operations with 50 or more vehicles and a disciplined internal claims management process.

Pro Tip: Do not assume your commercial auto policy covers tools, equipment, or personal belongings stored in your vehicles. Commercial vehicle policies often exclude personal belongings and tools carried in vehicles. A separate inland marine or commercial property policy fills that gap.

How to apply for and set up your fleet insurance policy

A systematic approach to the application process saves time and avoids the back-and-forth that delays coverage. Follow these steps in order.

- Compile your full documentation package. Use the four-category checklist from the documentation section above. Do not submit until every item is ready. Incomplete submissions go to the bottom of the underwriting queue.

- Choose a broker with fleet experience. General insurance agents handle personal lines well. Fleet policies require a broker who works with commercial auto markets regularly, understands FMCSA requirements, and has relationships with carriers that specialize in trucking or commercial vehicles. Mfandtna has over 30 years of experience placing commercial coverage for businesses across multiple states.

- Submit a detailed application. Your application should include your full vehicle schedule, driver list with MVRs, loss runs, and a description of your operations. The more complete your submission, the faster underwriters can respond.

- Respond to underwriting requests quickly. Underwriters will often ask follow-up questions about specific drivers, prior claims, or safety programs. Delays in responding extend your timeline. Assign one person internally to manage all underwriting communications.

- Implement telematics before you bind. Telematics programs can reduce insurance premiums by 10 to 25% for safer-than-average fleets. Presenting telematics data at the time of application, rather than after binding, gives underwriters a concrete reason to price your fleet more favorably.

- Review the policy before signing. Confirm that every vehicle on your schedule is listed, that coverage limits meet your contractual and regulatory requirements, and that all endorsements you requested are included.

Typical timelines run from five business days for straightforward fleets to three or four weeks for large or complex operations. Regulated carriers with FMCSA authority tend to take longer because underwriters verify safety scores and operating history. Maintaining clean FMCSA Safety Measurement System scores is critical for competitive pricing and insurer willingness to provide coverage at all. Some insurers refuse to quote carriers with above-threshold BASIC scores on the FMCSA Safety Measurement System.

For businesses in the Arlington area looking to protect their fleet, this resource on commercial fleet protection in Arlington covers local risk factors and documentation practices worth reviewing before you apply.

Common mistakes that delay or inflate your fleet insurance costs

Most problems during fleet insurance setup trace back to a small number of avoidable errors. Knowing them in advance puts you ahead of most applicants.

- Submitting incomplete loss runs. Five years of loss history is the standard. Submitting two or three years, or submitting loss runs with open reserves not explained, raises red flags with underwriters and slows the process.

- Underestimating your coverage needs. A contractor fleet hauling tools and equipment needs inland marine coverage in addition to commercial auto. A fleet with owner-operators needs bobtail or NTL coverage. Skipping specialty endorsements to save money creates gaps that cost far more at claim time.

- Neglecting driver MVRs. A single driver with a DUI or multiple at-fault accidents can make your entire fleet uninsurable with standard carriers. Pull MVRs before you apply so you know what you are working with.

- Failing to shop competing quotes. Shopping for competing quotes every two to three years can save 10 to 20% on premiums and provides negotiation leverage with your current carrier. The commercial auto market shifts significantly year to year, and loyalty does not always translate to savings.

- Ignoring telematics and safety program documentation. Telematics and driver safety programs directly impact premium pricing and underwriter appetite. Fleets without documented safety programs are priced as higher risk by default.

Providing a complete submission package with loss runs, fleet driver data, and telematics information signals a well-managed fleet to underwriters and consistently produces better quotes.

Pro Tip: Before your next renewal, request quotes from at least three carriers. Give each one the same complete submission package. The variation in quotes will surprise you, and the process itself often reveals coverage gaps in your current policy.

Key takeaways

A successful commercial auto fleet insurance setup depends on three things: complete documentation submitted upfront, a coverage stack matched to your actual operations, and a broker who understands commercial fleet markets.

| Point | Details |

|---|---|

| Documentation drives speed | Missing loss runs are the top cause of underwriting delays; gather five years before applying. |

| Coverage must match operations | Regulated carriers, cargo haulers, and owner-operators each need different endorsements beyond basic liability. |

| FMCSA limits are the floor | Minimum limits start at $750,000 but most shippers and brokers require $1,000,000 or more. |

| Telematics reduces premiums | Documented telematics programs can cut fleet insurance costs by 10 to 25% at renewal. |

| Shop every two to three years | Competing quotes save 10 to 20% and reveal whether your current coverage still fits your fleet. |

What I’ve learned after years of placing commercial fleet policies

After working with dozens of fleet operators across Massachusetts and beyond, the pattern I see most often is this: businesses that struggle with fleet insurance setup are not struggling because the process is complicated. They struggle because they underestimate how much preparation matters before they ever contact an insurer.

The fleets that get the best rates and the fastest approvals are the ones that walk in with a complete package. Clean MVRs, organized loss runs, telematics data, and a documented safety program. Underwriters are pricing uncertainty. When you remove the uncertainty with solid documentation, the price reflects that.

I also think too many fleet operators treat insurance as a once-and-done transaction. The commercial auto market is volatile. Rates for trucking and commercial fleets have moved significantly over the past several years due to nuclear verdicts, rising repair costs, and driver shortages. Shopping your coverage every two to three years is not disloyalty to your broker. It is responsible risk management.

One trend worth watching in 2026 is usage-based insurance (UBI). Usage-based insurance programs relying on telematics data are expanding rapidly, giving fleets direct control over their premiums through driver behavior. If your fleet is not already using telematics, the insurance savings alone often justify the investment within the first year.

The businesses I see overpaying consistently are the ones that set up their policy once and never revisit it. Your fleet changes. Your routes change. Your drivers change. Your policy should keep pace with all of it.

— Mike

How Mfandtna helps businesses set up commercial fleet coverage

Mfandtna is an independent insurance agency based in Arlington, MA, with over 30 years of experience placing commercial auto and fleet coverage for businesses across multiple states. When you work with Mfandtna, you get a broker who understands FMCSA requirements, knows which carriers specialize in fleet risks, and will help you build a coverage stack that fits your actual operations. Whether you are setting up coverage for the first time or shopping your renewal, Mfandtna compares options across multiple carriers to find you the right fit at a competitive price. Get a commercial auto quote and see what a properly structured fleet policy looks like for your business.

FAQ

What is commercial auto fleet insurance?

Commercial auto fleet insurance is a policy that covers two or more business-owned vehicles under a single contract, including liability, physical damage, and specialty coverages based on the fleet’s operations and regulatory requirements.

How much does fleet insurance cost per vehicle?

Average commercial auto liability costs run $8,000 to $12,000 per truck annually, with total fleet insurance ranging from $9,000 to $20,000 or more per vehicle depending on cargo type, driver history, and coverage limits.

How many vehicles do you need to qualify for fleet insurance?

Most insurers define a fleet as two or more vehicles, though some carriers require a minimum of five. Larger fleets typically access better per-unit pricing and broader coverage options.

Does commercial auto insurance cover tools and equipment in the vehicle?

No. Commercial vehicle policies typically exclude tools, equipment, and personal belongings stored in the vehicle. A separate inland marine or commercial property policy is required to cover those items.

How long does it take to set up fleet insurance?

Simple fleets with complete documentation can be quoted and bound in five to seven business days. Complex or regulated fleets with FMCSA authority typically take two to four weeks, depending on underwriting review and how quickly you respond to information requests.