Commercial auto insurance is a policy that provides liability and physical damage coverage for vehicles used for business purposes, protecting your company from financial losses that personal auto policies cannot cover. If your business owns, leases, or regularly uses vehicles to haul equipment, make deliveries, or transport clients, a standard personal auto policy will not protect you. Commercial auto coverage fills those gaps with higher liability limits, coverage for multiple drivers, and protections built around business operations. Understanding what this policy covers and when you need it is the first step toward protecting your business assets in 2026.

What is commercial auto insurance and what does it cover?

Commercial auto insurance is defined as a business insurance policy that covers vehicles owned, leased, or used by a company for work-related purposes. It fills the coverage gaps left by personal auto policies, which exclude business activities entirely. The policy applies to cars, vans, trucks, and specialty vehicles your business operates.

Standard commercial auto coverage includes several core components:

- Liability coverage: Pays for bodily injury and property damage your drivers cause to others. Recommended liability limits start at $500,000, with $1,000,000 common for businesses seeking stronger protection.

- Collision coverage: Pays to repair or replace your business vehicle after an accident, regardless of fault.

- Comprehensive coverage: Covers non-collision losses such as theft, fire, vandalism, and weather damage.

- Medical payments coverage: Pays medical expenses for your driver and passengers after an accident, no matter who caused it.

- Uninsured/underinsured motorist coverage: Protects your business when the at-fault driver carries no insurance or insufficient coverage.

- Hired and Non-Owned Auto (HNOA) coverage: Extends liability protection to vehicles your business rents or employees use for work in their personal cars.

One important exclusion: commercial auto insurance does not cover personal items carried inside the vehicle. A separate business owner’s policy or inland marine coverage handles those losses.

Pro Tip: If your employees occasionally use their personal cars for business errands, add HNOA coverage to your commercial policy. Without it, your business has no liability protection if one of those trips ends in an accident.

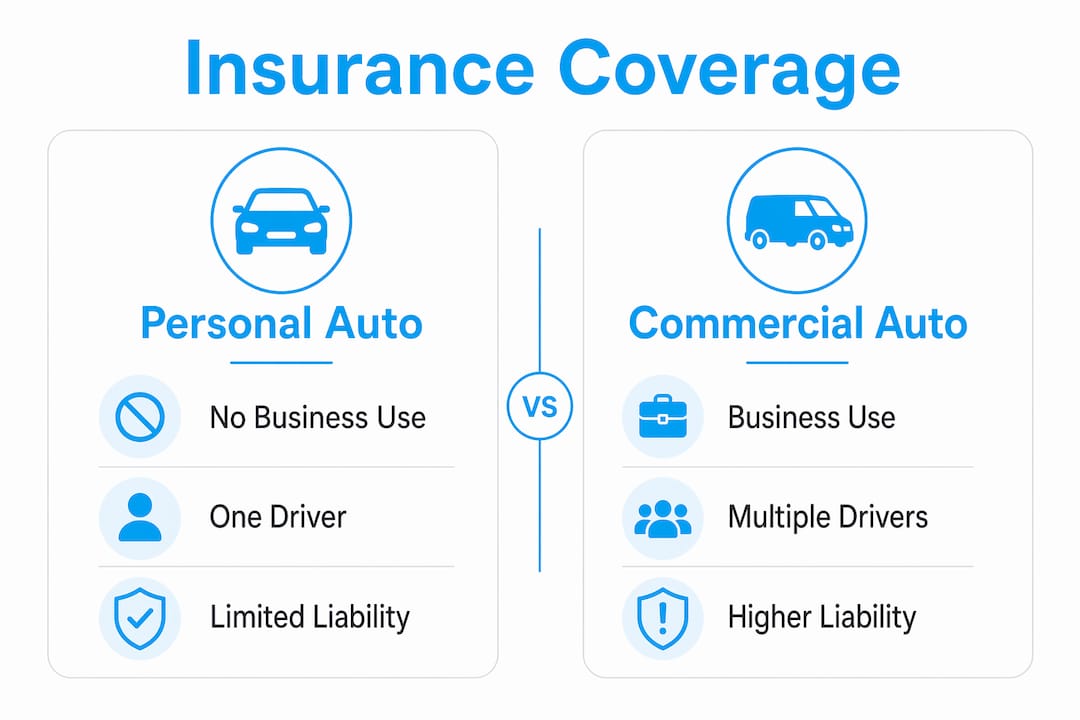

How does commercial auto insurance differ from personal auto insurance?

The core difference is scope. Personal auto insurance covers you for everyday driving, but it excludes business use in most circumstances. If you file a claim after an accident that happened during a business delivery, your personal insurer can deny it.

Here is a direct comparison of the two policy types:

| Feature | Personal auto insurance | Commercial auto insurance |

|---|---|---|

| Business use covered | No | Yes |

| Multiple employee drivers | No | Yes |

| Liability limits | Lower (typically $100K–$300K) | Higher (often $500K–$1M+) |

| Vehicle types | Personal cars | Cars, vans, trucks, specialty vehicles |

| Legal defense costs | Limited | Included for business accidents |

| HNOA coverage | Not available | Available as an add-on |

Commercial policies also cover multiple drivers on one policy, which personal policies do not accommodate well. If three employees share a delivery van, a commercial policy covers all of them under a single agreement.

Personal insurance might suffice if you occasionally drive your own car to a client meeting and your insurer knows about it. But the moment your vehicle is titled to your business, used for deliveries, or driven by employees, you need a commercial policy.

Pro Tip: Check your personal auto policy’s business-use exclusion language before assuming you are covered. Many policies void coverage the moment a vehicle is used to generate income, even part-time.

For a detailed breakdown of how these two policy types compare, see Mfandtna’s guide on commercial vs. personal auto coverage.

When do business owners and fleet managers need commercial auto insurance?

The short answer: if a vehicle touches your business operations, you need commercial coverage. Here is a clearer breakdown of the specific situations that require it.

- Your business owns or leases vehicles. Any vehicle titled to your company requires a commercial auto policy. Personal insurance does not apply to business-owned assets.

- Employees drive for work. If staff members drive to job sites, make deliveries, or visit clients on company time, your business carries liability for their actions behind the wheel.

- You haul equipment or goods. Business use scenarios like hauling tools, making deliveries, and operating mobile services increase risk and require commercial coverage to protect your assets.

- You operate a fleet. Fleet managers overseeing multiple vehicles need a single commercial policy that covers all drivers, all vehicles, and all routes under one agreement.

- State or federal law requires it. Nearly all states mandate commercial auto insurance for business vehicles, with New Hampshire as the one exception that allows financial responsibility as an alternative. Federal regulations apply to commercial trucks operating across state lines.

- You operate heavy-duty trucks. Commercial truck insurance is a specialized form of commercial auto coverage with higher liability limits and Federal Motor Carrier Safety Administration (FMCSA) compliance requirements. Limits typically range from $1,000,000 to $5,000,000 or more, depending on cargo type.

Relying on a personal policy for business driving is not just a coverage gap. It is a financial risk that could expose your business assets, your employees, and your company’s reputation to uncovered losses. The 2026 insurance requirements for commercial operations reinforce that compliance is not optional for most businesses.

What are the benefits and cost factors of commercial auto insurance?

Commercial auto insurance delivers concrete financial and operational benefits for businesses of every size.

Financial protection:

- Covers repair or replacement costs for damaged business vehicles.

- Pays medical bills for injured drivers and third parties.

- Protects your business bank account from large out-of-pocket accident costs.

Legal and liability protection:

- Business vehicle liability insurance covers legal defense costs when your company faces a lawsuit after an accident. That protection alone can save a small business from financial collapse.

- Higher liability limits mean your business stays protected even in serious multi-vehicle accidents.

Operational continuity:

- Rental reimbursement coverage keeps your fleet moving while a damaged vehicle is being repaired.

- Consistent coverage across all drivers reduces administrative gaps when employees change.

Cost factors to understand:

- Vehicle type and size: Heavier vehicles and specialty trucks cost more to insure.

- Business use: High-mileage routes and hazardous cargo increase premiums.

- Driver history: Clean driving records across your fleet lower your rates.

- Fleet size: Larger fleets may qualify for volume discounts.

- Coverage limits: Higher liability limits raise premiums but reduce financial exposure significantly.

You can manage costs by maintaining a strong fleet safety program, requiring driver training, and reviewing your policy annually. Bundling commercial auto with a business owner’s policy or general liability coverage often produces savings as well. Mfandtna’s fleet insurance setup guide walks through the steps for structuring coverage efficiently across multiple vehicles.

Key Takeaways

Commercial auto insurance is the only policy that fully protects business vehicles, drivers, and operations from liability and physical damage losses that personal auto policies exclude.

| Point | Details |

|---|---|

| Personal policies exclude business use | Any business-related driving voids personal auto coverage, making commercial insurance necessary. |

| Liability limits are higher | Commercial policies commonly offer $500,000 to $1,000,000 in liability, far above personal policy limits. |

| Multiple drivers are covered | One commercial policy covers all employees who drive business vehicles, unlike personal policies. |

| HNOA fills a critical gap | Hired and Non-Owned Auto coverage protects your business when employees use personal or rented vehicles for work. |

| Most states require it | Nearly all states mandate commercial auto insurance for business vehicles; federal rules apply to interstate trucks. |

What I’ve learned after 30 years of placing commercial auto policies

Most business owners I work with underestimate their exposure until after an accident. They assume their personal auto policy will handle it, or they think their general liability coverage extends to vehicles. Neither is true.

The biggest mistake I see is businesses waiting until they are legally required to get commercial coverage before they actually get it. By then, they have often already driven thousands of miles unprotected. The second biggest mistake is choosing the lowest available liability limit to save money. A $100,000 limit sounds like a lot until a serious accident produces $400,000 in medical bills and legal fees.

My advice: buy at least $500,000 in liability coverage from day one, and talk to a licensed agent who understands your specific industry. A contractor’s coverage needs look very different from a caterer’s. State regulations also change, and what was compliant last year may not meet 2026 requirements. Review your policy every year, not just when it renews. And if you manage a fleet, build a written fleet safety program. Insurers reward documented safety practices with lower premiums, and it gives you legal protection if a driver’s behavior ever comes into question.

Working with an independent agency means you get someone who shops multiple carriers on your behalf, not just one company’s products. That difference shows up in both price and coverage quality.

— Mike

Commercial auto coverage from Mfandtna

Mfandtna has helped businesses across Massachusetts and beyond find the right commercial auto coverage for over 30 years. Whether you run a single work truck or a multi-vehicle fleet, the team at Mfandtna compares options from multiple carriers to find coverage that fits your operation and your budget.

Getting a quote is straightforward. You share details about your vehicles, drivers, and how you use them, and Mfandtna’s agents build a policy around your actual needs. No guesswork, no one-size-fits-all packages. Get your free commercial auto quote today and see what the right coverage looks like for your business.

FAQ

What is commercial auto insurance used for?

Commercial auto insurance covers vehicles used for business purposes, including liability for accidents, physical damage to vehicles, and medical costs for injured parties. Personal auto policies exclude these situations entirely.

Is commercial auto insurance required by law?

Nearly all states require commercial auto insurance for business vehicles, with New Hampshire as the only state that allows financial responsibility as an alternative. Federal regulations also apply to commercial trucks crossing state lines.

How much liability coverage does a business need?

Insurance professionals recommend a minimum of $500,000 in liability coverage, with $1,000,000 being the standard for businesses that want stronger protection against serious accident claims.

Does commercial auto insurance cover employees driving their own cars?

Standard commercial auto insurance does not cover employees’ personal vehicles. HNOA coverage is the add-on that extends liability protection when employees use personal or rented vehicles for business tasks.

What is the difference between commercial auto and commercial truck insurance?

Commercial truck insurance is a specialized form of commercial auto coverage designed for heavy-duty trucks. It carries higher liability limits, often $1,000,000 to $5,000,000, and must meet FMCSA compliance requirements that standard commercial auto policies do not address.