Homeowners insurance is designed to cover sudden, accidental damage, not the slow deterioration that comes from skipping repairs. Understanding why insurance requires home maintenance protects you from one of the most common and costly surprises in the claims process: a denied claim. Standard policies like the HO-3 exclude damage caused by neglect, gradual wear, and deferred upkeep. That distinction is not buried in fine print. It is the foundation of how insurers calculate risk, price premiums, and decide whether to renew your policy.

Why insurance requires home maintenance: the policy basics

Standard HO-3 policies exclude damage from gradual wear and tear and maintenance neglect while covering sudden, accidental losses. This is called the maintenance exclusion, and it appears in virtually every homeowners policy sold in the United States. The logic is straightforward: insurance is meant to protect you from unpredictable events, not from the predictable consequences of skipping repairs.

Maintenance exclusion exists because insuring predictable wear would make premiums cost-prohibitive for every policyholder. If insurers had to pay for every aging roof, rusting pipe, and rotting deck, the risk pool would collapse under the weight of entirely avoidable losses.

Adjusters are trained to tell the difference between sudden damage and pre-existing conditions. They look at rust patterns, rot depth, and the age of the affected material to determine whether damage developed over time. Insurance policies are not maintenance contracts, and adjusters make that distinction on every claim they review.

What counts as neglect under your policy

Insurers define neglect as failing to take reasonable steps to maintain your home in good condition. Common examples include:

- Clogged gutters that cause water to back up and damage the fascia or foundation

- Slow plumbing leaks left unaddressed for weeks or months

- Pest infestations that go untreated until structural damage occurs

- Cracked or missing roof shingles that allow water intrusion over time

- Deteriorating caulk around windows and doors that lets moisture in

Pest damage, mechanical breakdowns, and gradual deterioration are all explicitly excluded from standard coverage. You bear those costs entirely.

Pro Tip: Read your policy’s exclusions section before you need to file a claim. Knowing what is not covered is just as valuable as knowing what is.

What does neglecting home maintenance actually cost you?

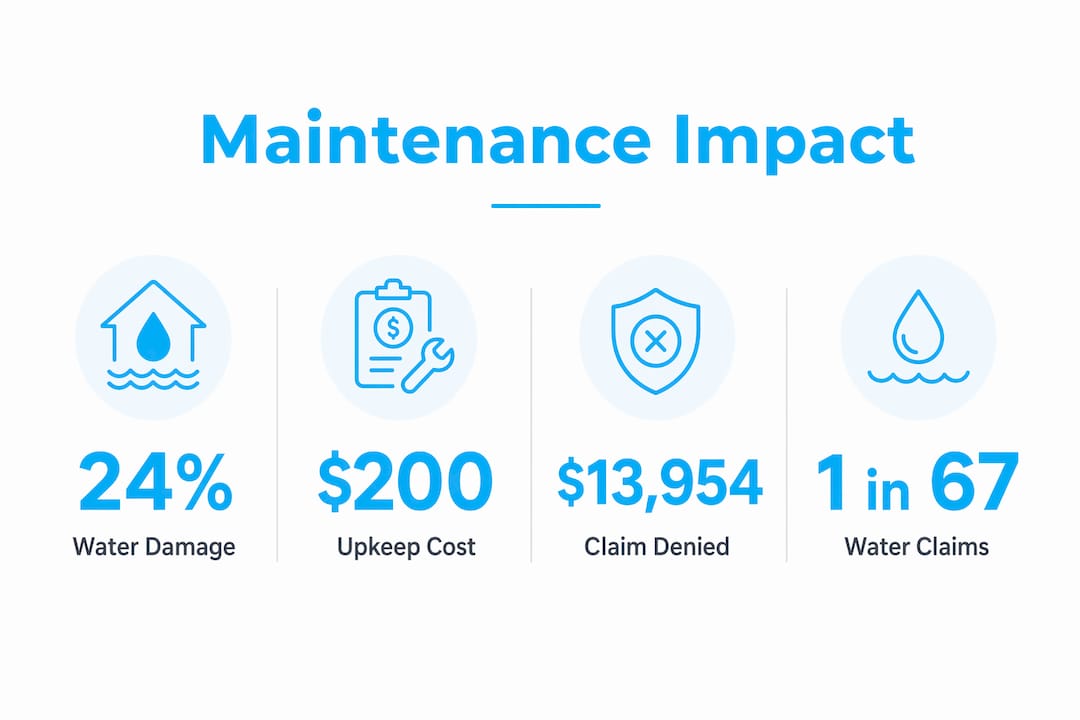

The financial consequences of skipping upkeep go far beyond the repair bill. Water damage accounts for about 24% of all homeowners insurance claims annually, yet many of those claims are denied because the damage traces back to a maintenance issue the homeowner ignored. That is a significant share of claims that pay out nothing.

The cost asymmetry is striking. Neglecting a $200 maintenance task can escalate to a $13,954 denied claim, with premiums increasing for 5–7 years afterward. A clogged gutter cleaning that costs $150 in the fall can prevent thousands of dollars in water damage that your insurer will refuse to cover.

Premium increases are not the only consequence. Insurers can also choose not to renew your policy if they identify visible signs of neglect during an inspection or after a claim. Losing coverage forces you into the high-risk insurance market, where premiums are substantially higher and options are limited.

| Deferred task | Approximate repair cost | Insurance outcome |

|---|---|---|

| Gutter cleaning ($150) | Water damage: $3,000+ | Likely denied as maintenance neglect |

| Roof shingle repair ($300) | Interior water damage: $8,000+ | Denied if neglect is documented |

| Plumbing leak fix ($200) | Mold remediation: $10,000+ | Denied if leak was gradual |

| Pest treatment ($250) | Structural repair: $15,000+ | Excluded from all standard policies |

Pro Tip: Keep receipts for every maintenance task you complete. A paper trail showing regular upkeep is your best defense if an adjuster questions whether damage was sudden or gradual.

1 in 67 insured homes files a water damage or freezing claim each year. That frequency means insurers scrutinize these claims closely, and documentation of your maintenance history can be the deciding factor between approval and denial.

How does regular maintenance influence your premiums and coverage?

Consistent upkeep directly shapes your risk profile, and your risk profile directly shapes your premium. Insurers reward homeowners who reduce risk, and a well-maintained home signals lower likelihood of a large claim. The relationship between home maintenance and insurance costs is not theoretical. It shows up in your renewal quote every year.

Updating your insurer about major home improvements can lower premiums and make sure your coverage stays adequate. A new roof, updated electrical panel, or replaced HVAC system all reduce your insurer’s risk exposure. Failing to report these improvements means you miss out on potential discounts and may be underinsured if you need to rebuild.

Homeowners must notify their insurer of improvements like new roofs or finished basements to adjust coverage and potentially reduce premiums. This is one of the most overlooked ways to save money on your policy. You can learn more about how these updates affect your coverage by reviewing the types of homeowners insurance coverage available to you.

Regular upkeep also keeps your policy in good standing at renewal time. Insurers review claim history and sometimes conduct exterior inspections before renewing. Visible neglect, such as a sagging roof or peeling paint on wood siding, can trigger a non-renewal notice. The benefits of staying current with maintenance include:

- Lower premiums tied to a reduced risk profile

- Eligibility for discounts when you update major home systems

- Smooth renewals without inspection-triggered policy reviews

- Adequate coverage limits that reflect your home’s current condition and value

- Fewer claim disputes because damage is clearly sudden rather than gradual

Routine maintenance and homeowner-insurer communication prevent surprises at claim time and keep your policy in good standing. That communication is free and takes minutes. The cost of skipping it can run into thousands of dollars.

What practical steps meet your insurer’s maintenance expectations?

Meeting your insurer’s expectations does not require a full renovation schedule. It requires a consistent, documented approach to keeping your home in reasonable condition. Here is how to build that habit:

-

Inspect your roof twice a year. Check for missing, cracked, or curling shingles every spring and fall. Address any damage before the next weather season arrives.

-

Clean gutters at least twice a year. Clogged gutters are one of the most common causes of denied water damage claims. Clear them in late fall after leaves drop and again in spring.

-

Check plumbing for slow leaks monthly. Look under sinks, around toilets, and near your water heater. A slow drip that goes unnoticed for months becomes a mold problem that your insurer will not cover.

-

Service your HVAC system annually. A professional tune-up keeps your system running efficiently and creates a service record that documents your upkeep.

-

Treat pest activity immediately. Do not wait to see if a problem resolves itself. Pest damage is excluded from standard policies, so the cost of treatment is always cheaper than the cost of structural repair.

-

Budget 1% to 3% of your home’s value annually for maintenance. Experts recommend this range to protect coverage continuity and preserve your home’s equity. On a $400,000 home, that is $4,000–$12,000 per year set aside for upkeep.

-

Call your insurance agent after any major repair or improvement. Report a new roof, updated plumbing, or finished basement. Your agent can adjust your coverage and check whether you qualify for a premium reduction.

-

Keep a maintenance log. Record every task with the date, cost, and contractor name. Store receipts digitally. This log is your primary evidence if an adjuster questions the timeline of any damage.

Understanding how home insurance works gives you the context to make these steps count. Knowing the claims process before you need it means you are never caught off guard.

Key Takeaways

Home maintenance is a direct insurance requirement because policies cover sudden accidents, not gradual neglect, and skipping upkeep puts your claims, premiums, and coverage eligibility at risk.

| Point | Details |

|---|---|

| Maintenance exclusion is standard | HO-3 policies exclude gradual wear, neglect, and pest damage from all coverage. |

| Neglect creates denied claims | A skipped $200 repair can result in a $13,954 denied claim and years of higher premiums. |

| Upkeep lowers your premium | Reporting improvements like a new roof can reduce your risk profile and unlock discounts. |

| Budget 1%–3% of home value annually | This range protects coverage continuity and prevents costly deferred repairs. |

| Document everything | A maintenance log with receipts is your best defense against adjuster disputes. |

Why I think most homeowners misunderstand what insurance actually covers

After working with homeowners for over 30 years, the most common misconception I see is this: people believe their insurance policy is a home warranty. It is not. A home warranty covers mechanical breakdowns and aging systems. Homeowners insurance covers sudden, accidental losses. Those are two completely different products, and confusing them is expensive.

The homeowners who get burned are almost always the ones who deferred a small repair because they assumed their policy would cover whatever went wrong. A slow leak under the kitchen sink turns into a mold claim. The adjuster pulls out a moisture meter, finds rot that took months to develop, and denies the claim. The homeowner is shocked. The insurer is not.

What I tell every client is this: treat your maintenance budget as part of your insurance strategy. The money you spend on upkeep is money you save on denied claims, premium increases, and policy non-renewals. The impact of neglect on insurance is not abstract. It shows up as a check you do not receive when you need it most.

The homeowners who fare best are the ones who stay proactive, communicate with their agents, and treat their home like the financial asset it is. That mindset does not require a big budget. It requires consistency and a basic understanding of what your policy actually promises.

— Mike

How Mfandtna helps you protect your home and your coverage

Mfandtna has spent over 30 years helping homeowners in Massachusetts and beyond find coverage that fits their property and their budget. Whether you have recently completed a major renovation, want to review your current policy for maintenance-related gaps, or are shopping for a new policy, the team at Mfandtna can walk you through your options clearly and without pressure.

Getting your coverage right starts with understanding what your policy requires. Mfandtna’s homeowners insurance FAQ answers the most common questions about exclusions, claims, and upkeep expectations. When you are ready to compare options or adjust your coverage after a home improvement, you can request a free insurance quote directly through the Mfandtna website. A quick policy review today can prevent a costly coverage gap tomorrow.

FAQ

Why do insurance policies exclude maintenance-related damage?

Standard policies exclude maintenance damage because insuring predictable wear would make premiums unaffordable for all policyholders. Insurance is designed for sudden, accidental losses, not for the foreseeable results of deferred upkeep.

Can a denied claim raise my insurance premiums?

Yes. A denied claim tied to neglect signals a higher risk profile to your insurer, which can trigger premium increases lasting 5–7 years or even a policy non-renewal.

What home improvements should I report to my insurer?

Report any major update, including a new roof, replaced plumbing, updated electrical panel, or finished basement. Notifying your insurer about improvements can lower your premium and prevent underinsurance.

How much should I budget for home maintenance each year?

Experts recommend setting aside 1%–3% of your home’s value annually. On a $350,000 home, that means budgeting $3,500–$10,500 per year for upkeep.

Does keeping maintenance records actually help with claims?

Yes. Adjusters examine the duration and nature of damage to classify it as sudden or gradual. A documented maintenance history showing regular inspections and repairs supports your case that damage was unexpected, not the result of neglect.