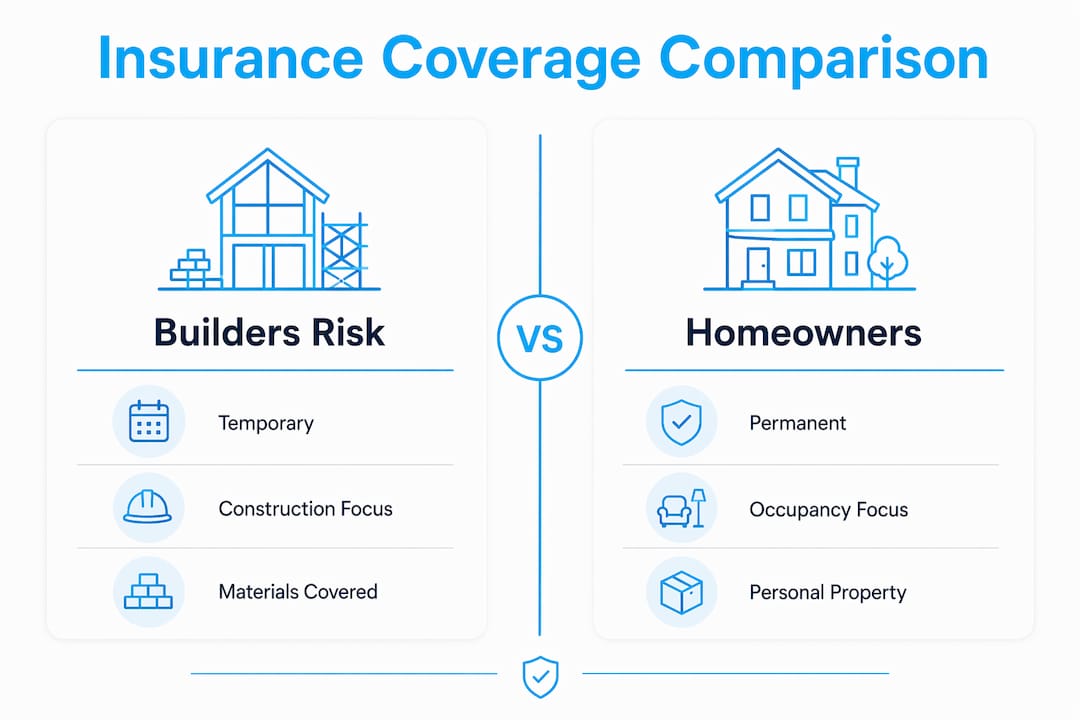

Builders risk insurance is defined as a temporary property policy that covers structures, materials, and equipment during active construction or renovation. Homeowners insurance, by contrast, protects finished, occupied dwellings and is not designed for active job sites. The difference between builders risk and homeowners insurance is not a technicality. It is a coverage gap that can cost you tens of thousands of dollars if you pick the wrong policy before breaking ground. Whether you are a homeowner planning a major addition or a contractor managing a new build, understanding which policy applies at each stage of a project is the most practical thing you can do before work starts.

What does builders risk cover that homeowners insurance does not?

Builders risk insurance covers property and materials while a structure is being built or renovated, paying out for fire, vandalism, theft, and unexpected events during the construction phase. That scope goes well beyond what a standard homeowners policy will touch. The HO-3 policy form, which is the most common homeowners policy in the United States, is written for finished dwellings and restricts or excludes coverage for structures under active construction.

The coverage differences break down into four practical areas:

- Materials on-site, in transit, and in off-site storage. Builders risk covers lumber, fixtures, and equipment whether they sit on the job site, ride in a delivery truck, or wait in a storage unit. Homeowners policies typically exclude uninstalled materials entirely.

- Perils specific to construction sites. Fire, wind, hail, theft, and vandalism are all covered under a standard builders risk form. Homeowners policies may cover some of these perils for the finished structure, but not for an active, partially built project.

- Soft costs via endorsement. Builders risk policies can be extended to cover financial losses caused by covered delays, including additional loan interest, permit fees, and architectural expenses. Homeowners policies have no equivalent.

- Vacancy and unoccupied status. Vacancy clauses in homeowners insurance reduce or void coverage for vandalism, theft, and water damage when a home sits unoccupied during renovations. Builders risk is designed to provide continuous coverage regardless of occupancy status.

Pro Tip: Ask your insurer whether your builders risk policy covers materials in transit. Many base forms do not include transit coverage automatically, and adding it as a rider is far cheaper than replacing a stolen delivery of windows or cabinets.

How do coverage duration and policy limits differ?

Builders risk policies are temporary and project-based. They typically cover 3–12 months, ending once construction completes or the certificate of occupancy is issued. Homeowners insurance is ongoing and renews annually as long as the home is occupied and premiums are paid.

Policy limits also follow different logic. Builders risk limits are tied to the total construction value or the completed value of the project. If you are building a $400,000 addition, your builders risk limit should reflect that budget, not the current market value of your land. Homeowners insurance limits are based on the replacement cost of the finished home and its contents.

| Feature | Builders risk | Homeowners insurance |

|---|---|---|

| Coverage period | 3–12 months, project-based | Ongoing, annual renewal |

| Policy limit basis | Construction budget or completed value | Replacement cost of finished home |

| Occupancy requirement | None. Covers vacant or unoccupied sites | Requires occupancy. Vacancy clauses apply |

| Materials coverage | On-site, in transit, off-site storage | Excludes uninstalled materials |

| Soft costs | Available via endorsement | Not available |

The transition between policies matters as much as the policies themselves. When construction ends, your builders risk policy expires. You need a homeowners policy in place before that date, not after. A gap of even a few days leaves your newly completed home unprotected.

What do builders risk premiums cost compared to homeowners insurance?

Builders risk premiums typically range from 1% to 5% of the total construction budget. That means a $300,000 residential build could cost $3,000–$7,500 per year in builders risk premiums. A larger $5 million commercial project can reach $50,000–$150,000. Homeowners insurance premiums are generally lower for finished homes because the risk profile of a completed, occupied structure is more predictable than an active job site.

Several factors push builders risk premiums up or down:

- Project size and construction value. Larger budgets mean higher limits and higher premiums.

- Location. Sites in flood zones, high-crime areas, or hurricane-prone regions carry higher rates.

- Building materials. Wood-frame construction costs more to insure than steel or concrete.

- Contractor experience and licensing. Insurers view licensed, experienced contractors as lower risk.

- Site security. Fencing, lighting, and on-site cameras reduce theft exposure and can lower your rate.

The cost-benefit case for builders risk is straightforward. A single theft event on a job site, a fire that destroys framing, or a windstorm that collapses a partially built roof can easily exceed the total annual premium. Relying on a homeowners policy to cover those losses is not a cost-saving move. It is a coverage gap waiting to become a financial loss.

When should you choose builders risk vs homeowners insurance?

The right policy depends on the scope of your project. Not every renovation requires a standalone builders risk policy, but most significant construction projects do.

- New construction. A homeowners policy does not apply to a home that does not yet exist. Builders risk is the only appropriate coverage from groundbreaking through certificate of occupancy.

- Major renovations. Additions, gut renovations, and structural changes that leave a home vacant for more than 30–60 days will trigger vacancy clauses in a standard homeowners policy. Builders risk fills that gap.

- Cosmetic updates. Painting, flooring, and minor fixture replacements on an occupied home generally stay within homeowners policy coverage. A standalone builders risk policy is usually not necessary.

- Contractor-managed projects. Construction contracts should specify who purchases builders risk coverage and who is named as an insured. Do not assume your contractor carries it. Verify before work starts.

- Dwelling-under-construction endorsement. Some homeowners policies allow you to add a dwelling-under-construction endorsement that waives vacancy exclusions. This option works for limited renovations but typically excludes theft of uninstalled materials and lacks the full property protections of a standalone builders risk policy.

Pro Tip: If your contractor says they carry builders risk, ask to be named as an additional insured on their policy. A contractor’s policy protects their interests. Being named as an additional insured protects yours.

Working with an experienced insurance agent before your project starts is the most reliable way to identify which policy applies, what endorsements you need, and how to time the transition from builders risk to homeowners coverage at project completion.

Common misconceptions about homeowners insurance during construction

The most expensive misconception is that an existing homeowners policy automatically covers a home under renovation. It does not. Standard HO-3 policies exclude or limit coverage for structures under construction, and vacancy clauses can void coverage after just 30–60 days of unoccupancy.

Several other gaps catch homeowners and contractors off guard:

- Uninstalled materials are excluded. A homeowners policy will not pay for stolen lumber, cabinets, or appliances that have not yet been installed. Builders risk covers these items from the moment they arrive on-site.

- Contractor tools and equipment are not covered. Your homeowners policy does not cover a contractor’s tools or equipment stored on your property. The contractor needs their own inland marine or equipment floater policy.

- Liability coverage differs. Builders risk insurance typically excludes liability, meaning it will not pay if a visitor is injured on your job site. Homeowners policies include liability coverage, but that coverage may be limited or excluded during active construction. Contractors should carry their own general liability policy.

- Delays and financial losses are not covered by homeowners policies. If a fire destroys your framing and delays your project by three months, a homeowners policy will not cover the additional loan interest or permit renewal fees. A builders risk policy with a soft costs endorsement will.

- Assuming coverage without verifying it is the most common and costly mistake. Always review your existing homeowners policy with your agent before starting any construction project, no matter how minor it seems.

Understanding these gaps before your project starts gives you time to fill them. Discovering them after a loss does not.

Key Takeaways

Builders risk insurance is the correct coverage for active construction, while homeowners insurance is designed exclusively for finished, occupied homes. Relying on a homeowners policy during construction creates coverage gaps that can result in significant financial loss.

| Point | Details |

|---|---|

| Builders risk covers construction phases | It protects structures, materials, and equipment from groundbreaking through project completion. |

| Homeowners policies have vacancy clauses | Coverage for vandalism, theft, and water damage can be voided after 30–60 days of unoccupancy. |

| Premiums reflect construction risk | Builders risk costs 1%–5% of the construction budget, reflecting the higher risk of an active job site. |

| Policy limits follow different logic | Builders risk limits tie to construction value; homeowners limits tie to finished replacement cost. |

| Transition timing is critical | Your homeowners policy must be in place before your builders risk policy expires to avoid a coverage gap. |

What I have learned after 30 years of placing construction coverage

After three decades of placing insurance for homeowners and contractors across Massachusetts and beyond, the pattern I see most often is not ignorance. It is assumption. Homeowners assume their existing policy covers the renovation. Contractors assume the homeowner has builders risk. Nobody checks. Then a theft or a fire happens, and the claim gets denied.

The vacancy clause issue is the one that surprises people most. A homeowner starts a gut renovation, moves out for four months, and assumes their HO-3 policy is still fully active. It is not. Most standard policies begin limiting or voiding coverage for vandalism and water damage after 30–60 days of vacancy. That is a fact most policyholders never read in their policy documents.

The other thing I tell every contractor I work with: get named as an additional insured on the property owner’s builders risk policy, and carry your own general liability coverage. Builders risk does not cover liability. If someone gets hurt on that job site, you need your own policy to respond.

The dwelling-under-construction endorsement is a useful middle ground for smaller projects, but it is not a substitute for a full builders risk policy on a major renovation or new build. The gaps in transit coverage and uninstalled materials alone make it inadequate for most significant projects.

My advice is simple. Call your agent before you pull the permit. Not after the framing goes up.

— Mike

Get the right construction coverage with Mfandtna

Choosing between builders risk and homeowners insurance is not a decision to make on your own, especially when a construction project represents one of the largest financial commitments you will make.

Mfandtna has placed builders risk and homeowners insurance for clients across Massachusetts and multiple states for over 30 years. The team helps homeowners and contractors identify coverage gaps, select the right policy for each project phase, and time the transition from construction coverage to a permanent homeowners policy. Get a free insurance quote and speak with an agent who knows construction risk from the ground up. You can also explore Mfandtna’s builders risk insurance services to see what coverage options are available for your specific project.

FAQ

What is the main difference between builders risk and homeowners insurance?

Builders risk insurance covers structures and materials during active construction, while homeowners insurance covers finished, occupied homes. Using a homeowners policy during construction creates significant coverage gaps, particularly for uninstalled materials and vacant properties.

Does homeowners insurance cover construction projects?

Standard homeowners insurance does not cover active construction. Vacancy clauses can void coverage after 30–60 days, and uninstalled materials are typically excluded. A dwelling-under-construction endorsement offers limited protection but lacks the full scope of a standalone builders risk policy.

How long does a builders risk policy last?

Builders risk policies are temporary and project-based, typically lasting 3–12 months. The policy ends when construction completes or the certificate of occupancy is issued, at which point a homeowners policy should take over.

Who buys builders risk insurance, the homeowner or the contractor?

Either party can purchase builders risk insurance. Construction contracts should specify who is responsible and who is named as an insured. Never assume the other party has coverage. Verify it in writing before work begins.

Can I add builders risk coverage to my existing homeowners policy?

Some insurers offer a dwelling-under-construction endorsement that extends limited coverage during renovation. This option waives vacancy exclusions but typically excludes theft of uninstalled materials and does not provide the full protections of a standalone builders risk policy.