Auto insurance liability is defined as the coverage that pays for injuries and property damage you cause to others in a car accident. It does not cover your own vehicle, your medical bills, or your personal property. Liability coverage is the most important and most misunderstood component of auto insurance because it protects your financial future, not your car. Most U.S. states legally require it, and choosing the wrong limits can put your savings, home equity, and future earnings at risk.

Auto insurance liability explained: what it is and how it works

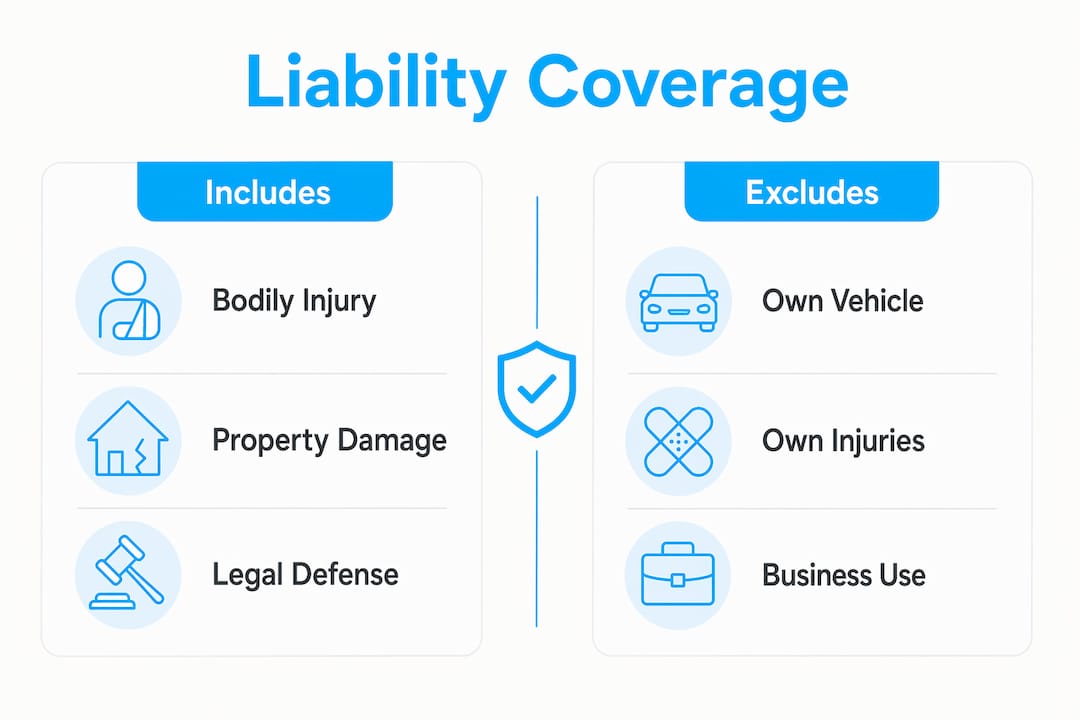

Auto liability coverage splits into two distinct parts: bodily injury liability and property damage liability. Bodily injury liability pays for the other driver’s medical bills, lost wages, and pain and suffering when you are at fault. Property damage liability covers repairs to the other person’s vehicle or any other property you damage, such as a fence or a storefront.

What liability insurance does not do is equally important to understand. It never covers your own vehicle or your own medical expenses after an at-fault accident. That distinction surprises many drivers who assume their policy protects them from all directions.

Your liability limits appear as three numbers on your policy, such as 25/50/25. The first number is the maximum payout per injured person in thousands of dollars. The second is the total payout per accident for all injured people. The third is the maximum for property damage. Knowing how to read these numbers helps you compare policies and spot gaps before an accident happens.

What does auto liability coverage include and exclude?

Liability coverage handles more than just repair bills and hospital costs. Here is what a standard auto liability policy typically covers:

- Bodily injury to others: Medical treatment, emergency care, rehabilitation, lost income, and pain and suffering for people you injure

- Property damage to others: Repairs or replacement of another person’s vehicle, a mailbox, a building, or any other structure you damage

- Legal defense costs: Attorney fees, court costs, and settlement negotiations if the injured party sues you

One detail that catches many policyholders off guard is how legal defense costs work. Under most standard auto policies, defense costs are covered in addition to your liability limits, not subtracted from them. Your full coverage amount stays available for the actual claim payout even while your insurer pays lawyers to defend you.

Here is what liability coverage does not include:

- Your own medical bills (covered by Medical Payments coverage or Personal Injury Protection)

- Damage to your own vehicle (covered by collision insurance)

- Theft or vandalism to your car (covered by comprehensive insurance)

- Injuries or damage that occur during business use of your personal vehicle

Pro Tip: If you drive for a rideshare service like Uber or Lyft, your personal auto liability policy likely excludes those trips. You need a rideshare endorsement or a separate commercial policy to stay protected.

Business use of personal vehicles is excluded under personal liability policies. Drivers frequently discover this gap only after an accident during a delivery or rideshare shift, which is far too late to fix it.

What are the legal requirements for liability insurance?

Nearly every U.S. state requires drivers to carry a minimum level of auto liability insurance. The most common minimum is 25/50/25, meaning $25,000 per person for bodily injury, $50,000 per accident, and $25,000 for property damage. New Hampshire and Virginia are the only states that allow drivers to opt out under specific financial responsibility conditions.

The table below compares typical state minimums with the limits financial advisors actually recommend:

| Coverage Type | State Minimum (Typical) | Recommended Limits |

|---|---|---|

| Bodily Injury Per Person | $25,000 | $100,000 |

| Bodily Injury Per Accident | $50,000 | $300,000 |

| Property Damage | $25,000 | $100,000 |

State minimums are insufficient to cover the full costs of serious accidents. A single serious crash can generate claims exceeding $200,000, which means a driver carrying only 25/50/25 limits could owe the difference out of pocket.

Financial advisors recommend carrying at least 100/300/100 liability limits to protect personal assets beyond what state minimums require. If a judgment against you exceeds your policy limits, creditors can pursue your savings, home equity, and future wages.

Pro Tip: Check your state’s Department of Insurance website to confirm your specific minimum requirements. States update these figures periodically, and what was compliant three years ago may no longer meet today’s legal standard.

You can check auto insurance costs in your area to see how higher limits affect your premium before you commit to a change.

How does liability differ from collision and comprehensive?

Liability, collision, and comprehensive are three separate coverages that serve completely different purposes. Understanding the difference helps you build a policy that actually protects you.

Liability pays for harm you cause to others. It does not touch your own vehicle or your own injuries.

Collision pays to repair or replace your own car after an accident, regardless of who is at fault. If you rear-end another driver, collision coverage fixes your car while liability pays for theirs.

Comprehensive covers damage to your own vehicle from events that are not collisions. Theft, hail, flooding, fire, and animal strikes all fall under comprehensive.

| Coverage | Protects Your Car | Protects Others | Required by Law |

|---|---|---|---|

| Liability | No | Yes | Yes (most states) |

| Collision | Yes | No | No (lenders may require) |

| Comprehensive | Yes | No | No (lenders may require) |

The phrase “full coverage” is not an official insurance term. It typically refers to a policy that bundles liability, collision, and comprehensive together. Lenders financing a vehicle almost always require collision and comprehensive in addition to liability. Once your car is paid off, you decide whether to keep those coverages based on your vehicle’s value.

Liability-only policies are significantly cheaper than full coverage, with annual premiums typically ranging from a few hundred dollars to about $750 depending on your state and driving record. The trade-off is real: you save on premiums but absorb all costs if your own car is damaged or stolen.

For drivers who use their vehicles for business purposes, a commercial vs. personal auto policy comparison is worth reviewing before assuming personal liability covers every situation.

How do you choose the right liability limits?

Selecting liability limits is not a one-size-fits-all decision. Your personal financial situation determines how much coverage you actually need.

- Calculate your net worth. Add up your savings, home equity, retirement accounts, and other assets. Your liability limits should be high enough to protect that total. A judgment can reach beyond your policy limits and into your personal assets.

- Consider your risk exposure. Drivers with long commutes, teen drivers on the policy, or high-traffic routes face statistically higher accident risk. Higher risk justifies higher limits.

- Look at umbrella insurance. Umbrella policies provide excess liability coverage starting at $1 million, with premiums typically costing $200–$400 per year. That is a low cost for a substantial safety net above your standard auto policy.

- Review your policy annually. Life changes such as buying a home, getting married, or starting a business all shift your financial exposure. Your coverage should keep pace.

- Ask about bundling discounts. Many insurers reduce premiums when you combine auto and home policies. Higher limits often cost less than drivers expect once discounts are applied.

Pro Tip: Liability coverage protects your net worth and future earnings, not just your car. Think of it as protecting everything you have worked to build, not just the vehicle in your driveway.

Liability coverage shields your assets and future earnings against lawsuits and claims. That framing changes how most people think about the cost of higher limits. Paying an extra $15–$30 per month for 100/300/100 coverage is far less painful than a six-figure judgment against your personal savings.

Key takeaways

Auto liability coverage is the financial shield between an at-fault accident and your personal assets, and state minimums rarely provide enough protection for drivers with real financial exposure.

| Point | Details |

|---|---|

| Liability covers others, not you | It pays for injuries and property damage you cause, never your own car or medical bills. |

| State minimums fall short | The typical 25/50/25 minimum leaves you exposed when accident costs exceed $200,000. |

| Defense costs are separate | Legal defense fees are covered in addition to your limits, not deducted from them. |

| Recommended limits are 100/300/100 | Financial advisors set this as the baseline for protecting personal assets and savings. |

| Umbrella policies add affordable protection | A $1 million umbrella policy typically costs just $200–$400 per year above your auto policy. |

What i’ve learned after 30 years of watching drivers get this wrong

Most drivers pick their liability limits the same way they pick a phone plan: they choose the cheapest option that meets the minimum requirement and move on. I have seen that decision cost people their savings, their home equity, and years of financial stability.

The most common misconception I encounter is that state minimums are “enough.” They are not. A single serious accident with injuries can generate bills that blow past $200,000 without much effort. A 25/50/25 policy leaves you personally responsible for everything above that threshold.

The second misconception is about legal defense costs. Many policyholders assume that if their insurer spends $40,000 defending them in court, that money comes out of their coverage limits. It does not. Defense costs are typically paid on top of your limits. That is genuinely good news that most people never hear.

My honest advice: treat liability limits as asset protection, not just a legal checkbox. If you own a home, have retirement savings, or earn a steady income, you have something worth protecting. A 100/300/100 policy with a $1 million umbrella on top costs far less per year than most people assume, and it covers the kind of catastrophic scenarios that actually threaten financial security.

Review your limits every year. Your life changes, and your coverage should too.

— Mike

How Mfandtna can help you get the right liability coverage

Choosing the right liability limits is easier when you have an experienced agency in your corner. Mfandtna has spent over 30 years helping drivers across Massachusetts and beyond find auto insurance coverage that fits their real financial situation, not just the state minimum.

Whether you are reviewing your current policy, shopping for the first time, or wondering if an umbrella policy makes sense for your situation, Mfandtna’s team can walk you through your options without pressure. You can also explore tailored auto insurance options for drivers in the Arlington area and request a personalized quote. Getting the right coverage now costs far less than the alternative.

FAQ

What is auto insurance liability coverage?

Auto insurance liability coverage pays for bodily injury and property damage you cause to others in an at-fault accident. It does not cover your own vehicle or your own medical expenses.

What does 25/50/25 mean on an auto policy?

The numbers represent your coverage limits in thousands of dollars: $25,000 per injured person, $50,000 total per accident for bodily injury, and $25,000 for property damage. Most financial advisors recommend raising these to 100/300/100 for adequate asset protection.

Does liability insurance cover legal fees?

Yes. Legal defense costs are covered in addition to your liability limits under most standard auto policies. Attorney fees and court costs do not reduce the amount available for the actual claim payout.

Is liability insurance required in every state?

Nearly every state requires a minimum level of auto liability insurance. New Hampshire and Virginia allow limited exceptions under specific financial responsibility rules, but all other states mandate at least a minimum liability policy.

What happens if my liability limits are too low?

If a judgment against you exceeds your policy limits, you are personally responsible for the difference. Creditors can pursue your savings, home equity, and future wages to satisfy the remaining balance.