Home and auto insurance bundling is the practice of purchasing both your homeowners (or renters) and auto insurance policies from the same carrier to earn a multi-policy discount and simplify your coverage. The industry term for this is a multi-policy discount, though most shoppers know it as bundling. Realistic savings average 8%–15% on your combined premiums, not the “up to 25%” figures you see in ads. State Farm, for example, advertises an average bundle discount of 22%, well above the industry norm. Beyond the savings, bundling cuts down on paperwork, phone calls, and the number of insurers you deal with every year.

What is home and auto insurance bundling and how does it work?

Bundling means your home and auto policies are separate contracts held by the same insurance company. They do not merge into one policy. The insurer links them in its system and applies a multi-policy discount to each.

Here is how the mechanics typically work:

- Unified billing. Most carriers consolidate both premiums into one monthly or annual bill. You write one check or set up one automatic payment.

- Single customer portal. Carriers like State Farm, Allstate, and Travelers give you one online account to manage both policies, view documents, and file claims.

- Split discount application. The discount usually applies partly to your auto premium and partly to your home premium. The auto side often gets the larger share.

- One agent relationship. You work with a single agent or service team for both policies, which speeds up changes and renewals.

- Possible combined deductible. Some carriers offer a single deductible if one event damages both your home and your car. This is not automatic and must be confirmed in your policy documents.

Bundling routes claims through one insurer and, in overlapping events, may assign a single adjuster to both your home and vehicle damage. That coordination alone saves you hours of back-and-forth during an already stressful situation. Insurers also benefit from bundling because it reduces their customer acquisition cost per policy, which is why they share some of that savings with you through the discount.

How much can you realistically save by bundling?

The gap between advertised discounts and actual savings is the most misunderstood part of bundling. Insurers advertise “up to 25%” discounts, but actual total premium savings average 8%–15%. That gap exists because the “up to 25%” figure often applies only to the auto portion of your premium, not your combined total.

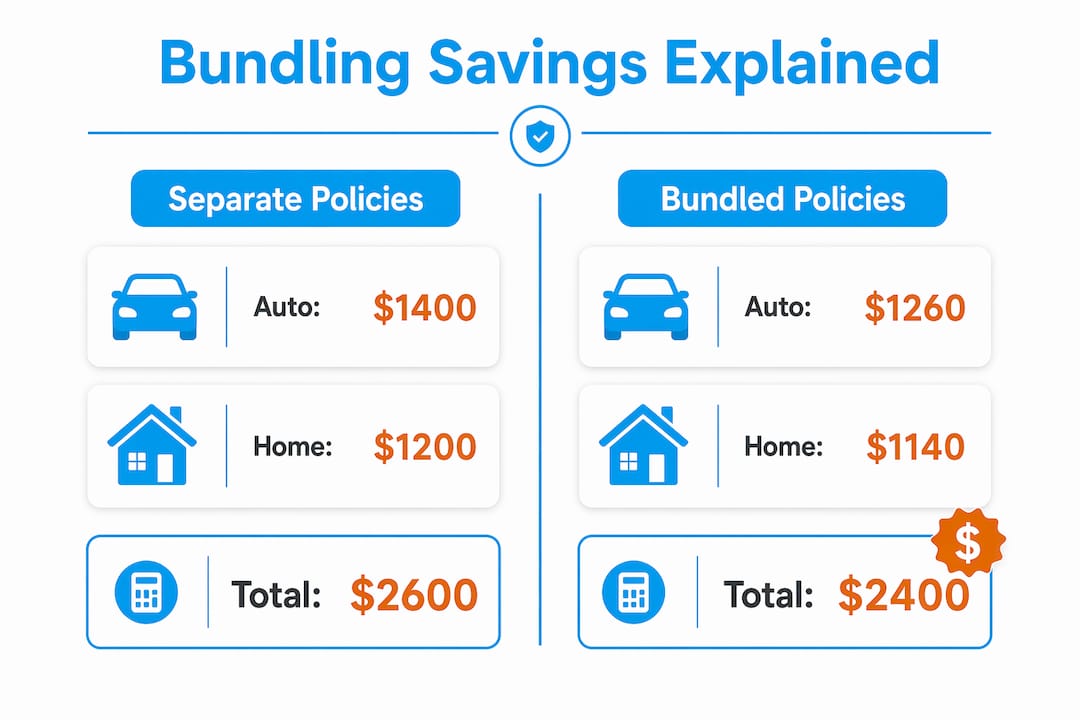

Here is a concrete example. Say your standalone auto premium is $1,400 per year and your standalone home premium is $1,200 per year, for a combined $2,600. A 10% bundle discount on the total saves you $260 annually. A 25% discount only on the auto side saves you $350, but only if your home premium does not increase to offset it.

| Scenario | Auto Premium | Home Premium | Total | Savings |

|---|---|---|---|---|

| Separate policies | $1,400 | $1,200 | $2,600 | — |

| Bundle (10% total) | $1,260 | $1,080 | $2,340 | $260 |

| Bundle (22% auto only) | $1,092 | $1,200 | $2,292 | $308 |

| Bundle (inflated home) | $1,092 | $1,450 | $2,542 | $58 |

The last row is the scenario most shoppers miss. About 30% of insurance bundles cost more than separate policies because the carrier raises the home premium to offset the auto discount. That means roughly one in three bundled customers pays more without realizing it. Always compare the total combined cost, not just the percentage off.

What are the pros and cons of bundling home and auto insurance?

Bundling has real advantages, but it also has traps worth knowing before you commit.

The clear benefits

- Simplified management. One insurer, one bill, one renewal conversation. This matters most when you are busy or managing coverage for a family.

- Single agent for both claims. If a hailstorm damages your roof and your car in the same storm, one agent handles both. That coordination reduces confusion and speeds up payouts.

- Loyalty perks. Many carriers add benefits over time for long-term bundled customers, including accident forgiveness on auto or reduced home deductibles after claim-free years.

- Renters plus auto bundles. Renters insurance costs about $12–$22 per month. Even a modest auto discount of 5%–8% on a $1,200 annual auto premium saves more than the renters policy costs. This is the clearest financial win in the bundling world.

The real drawbacks

- You may overpay on one policy. Carriers sometimes price the home policy higher to compensate for the auto discount. The net result is little or no savings.

- Limited carrier choice. Locking both policies with one insurer means you cannot mix and match the best rates. A competitor might offer a significantly cheaper auto policy that you would miss.

- High-risk properties complicate things. If your home is in a high fire zone, has an older roof, or is in a coastal flood area, carriers may inflate your home premium or decline to bundle at all.

- Young drivers reduce bundle value. Adding a teen driver to your auto policy spikes that premium. The bundle discount rarely offsets the surcharge.

Pro Tip: Before you switch to a bundle, ask your current insurer for itemized premiums on both policies separately. Then compare that total to the bundled quote. The percentage discount means nothing if the base prices are inflated.

How to compare bundled policies vs. separate policies

Shopping a bundle correctly takes a few deliberate steps. Most people skip straight to the discount percentage and miss the full picture. Focus on total cost and coverage limits rather than advertised discount percentages to verify true savings.

-

Get itemized quotes for both policies separately. Call or go online and price your home and auto policies as standalone products with each carrier you are considering. Write down the individual premiums.

-

Request the bundled quote from the same carriers. Ask each insurer to quote both policies together and show you the itemized breakdown. You want to see what each policy costs within the bundle, not just the combined total.

-

Match coverage levels exactly. Compare the same liability limits, deductibles, and coverage types across all quotes. Reviewing types of homeowners insurance coverage before you shop helps you know what to ask for. A cheaper bundle that cuts your dwelling coverage limit is not a deal.

-

Calculate the total annual cost. Add both premiums together for each scenario. The lowest total with equivalent coverage wins, regardless of which carrier offers the biggest percentage discount.

-

Check cancellation timing. If you switch mid-term, your current insurer will prorate a refund. Time your new bundle start date to align with your existing policy renewals when possible to avoid short-rate cancellation fees.

-

Verify the combined deductible feature. If a carrier advertises a single deductible for events that damage both home and car, ask for that in writing. Combined deductibles apply only under specific events covering both home and auto damage, and they are not automatic.

-

Revisit the comparison annually. Rates change at renewal. Set a calendar reminder to re-shop your bundle every 12 months.

Special cases: when bundling helps and when it backfires

Not every situation is a clean win for bundling. Understanding the exceptions helps you make a smarter call.

Renters insurance bundles: usually worth it

Renters insurance is inexpensive by design. At $12–$22 per month, the policy costs less annually than most people spend on streaming services. Bundling it with auto insurance almost always produces net savings because even a small auto discount exceeds the cost of the renters policy. If you rent and own a car, this is the bundle to prioritize.

When bundling often backfires

| Situation | Why Bundling May Cost More |

|---|---|

| Home in high fire or flood zone | Carrier inflates home premium to offset risk |

| Roof older than 20 years | Higher home premium reduces or eliminates auto savings |

| Teen driver on auto policy | Surcharge outweighs bundle discount |

| Liability-only auto coverage | Liability-only policies often qualify for limited or no bundle discounts |

| Recent home claims history | Carrier may price home policy higher regardless of bundle |

The auto coverage type you carry directly affects your bundle savings. If you drive an older car with liability-only coverage, the bundle discount on that policy may be minimal. Full coverage auto policies typically unlock the largest bundle discounts.

Pro Tip: Pull out your declarations page before shopping a bundle. Check whether your current home policy includes a combined deductible provision. If it does not, ask your new carrier whether they offer it and under what conditions it applies.

Key takeaways

Bundling home and auto insurance saves money only when the total combined premium with equivalent coverage is lower than buying each policy separately.

| Point | Details |

|---|---|

| Realistic savings range | Expect 8%–15% off your combined total, not the advertised 25%. |

| One in three bundles costs more | About 30% of bundles are more expensive due to inflated home premiums. |

| Renters bundles are the clearest win | Low renters insurance costs mean even small auto discounts produce net savings. |

| Compare totals, not percentages | Always add both itemized premiums and compare the full annual cost. |

| Coverage type affects discount | Liability-only auto policies often qualify for little or no bundle discount. |

Why i think most people shop bundles the wrong way

I have reviewed hundreds of insurance situations over the years, and the same mistake comes up constantly. A homeowner gets a mailer from State Farm or Allstate showing a 20% bundle discount, calls to switch, and never asks for the itemized breakdown. They see a lower number on the auto side and assume they are winning. They are not always winning.

The home premium is where carriers quietly make up the difference. I have seen home premiums jump $300–$400 per year inside a bundle while the auto discount saves $200. The net result is a $100–$200 annual loss, and the customer feels good about it because the percentage sounds impressive.

My honest recommendation: treat the bundle discount as a starting point, not a conclusion. Get the itemized numbers. Add them up. Then compare that total to what you would pay buying each policy from the best available carrier separately. Sometimes the bundle wins clearly. Sometimes it does not.

For renters, the math is almost always favorable. Renters insurance is cheap enough that any auto discount puts you ahead. For homeowners, especially those with older homes or properties in higher-risk areas, the comparison step is not optional. Checking for common home insurance coverage gaps before you bundle also protects you from trading a discount for reduced protection.

Shop your bundle every year at renewal. Rates shift. Your situation changes. The carrier that offered the best deal two years ago may not be the best deal today.

— Mike

How Mfandtna can help you find the right bundle

Mfandtna has spent over 30 years helping homeowners and renters across Massachusetts find coverage that actually fits their budget and their risk. As an independent agency based in Arlington, MA, Mfandtna works with multiple carriers, which means you get a real comparison instead of a pitch for one company’s bundle.

Whether you are looking to combine home and auto coverage for the first time or want to verify that your current bundle is still the best deal, Mfandtna walks you through the itemized numbers with no pressure. You can also explore auto insurance options in Arlington to see how your current policy stacks up. Request a free quote and get a side-by-side comparison built around your specific home, vehicle, and coverage needs.

FAQ

What does bundling home and auto insurance mean?

Bundling means purchasing your homeowners or renters insurance and your auto insurance from the same carrier to receive a multi-policy discount. The policies remain separate contracts but are linked in the insurer’s system.

How much does bundling home and auto insurance actually save?

Realistic savings average 8%–15% on your combined premiums. Advertised discounts of “up to 25%” typically apply only to the auto portion, not your total bill.

Can bundling ever cost more than separate policies?

Yes. About 30% of bundled policies cost more than buying separately because carriers sometimes raise the home premium to offset the auto discount. Always compare total combined costs before switching.

Does every bundle include a combined deductible?

No. A single combined deductible is only available from select carriers and applies only when one event damages both your home and your vehicle. Confirm this feature in writing before relying on it.

Is bundling renters and auto insurance worth it?

Renters insurance typically costs $12–$22 per month. Even a modest auto discount from bundling usually exceeds that annual cost, making the renters plus auto bundle one of the most straightforward ways to save on insurance.