Liability coverage is insurance that protects your finances when you are found legally responsible for injuring someone or damaging their property. It does not cover your own belongings or medical bills. It covers the costs you owe to others, including medical expenses, lost wages, and legal settlements. Most families carry liability coverage through their auto policy, homeowners policy, or both. Understanding how it works is the first step toward knowing whether you have enough protection.

What is liability coverage and why does it matter?

Liability coverage protects your financial future, not your property. If a guest slips on your icy front steps in Arlington, MA, and sues you for $80,000, your homeowners liability coverage pays that bill. Without it, that judgment comes directly out of your savings, home equity, or future earnings.

The industry term for this protection is “third-party liability insurance.” You are the first party, your insurer is the second, and the person making a claim against you is the third. This structure explains why liability coverage feels different from collision or property coverage. You are not filing a claim for yourself. You are defending yourself against someone else’s claim.

Liability can cover medical bills, lost wages, and legal settlements when you are at fault. That scope is wider than most families realize. A single car accident with injuries can generate costs that run well into six figures before a case ever reaches a courtroom.

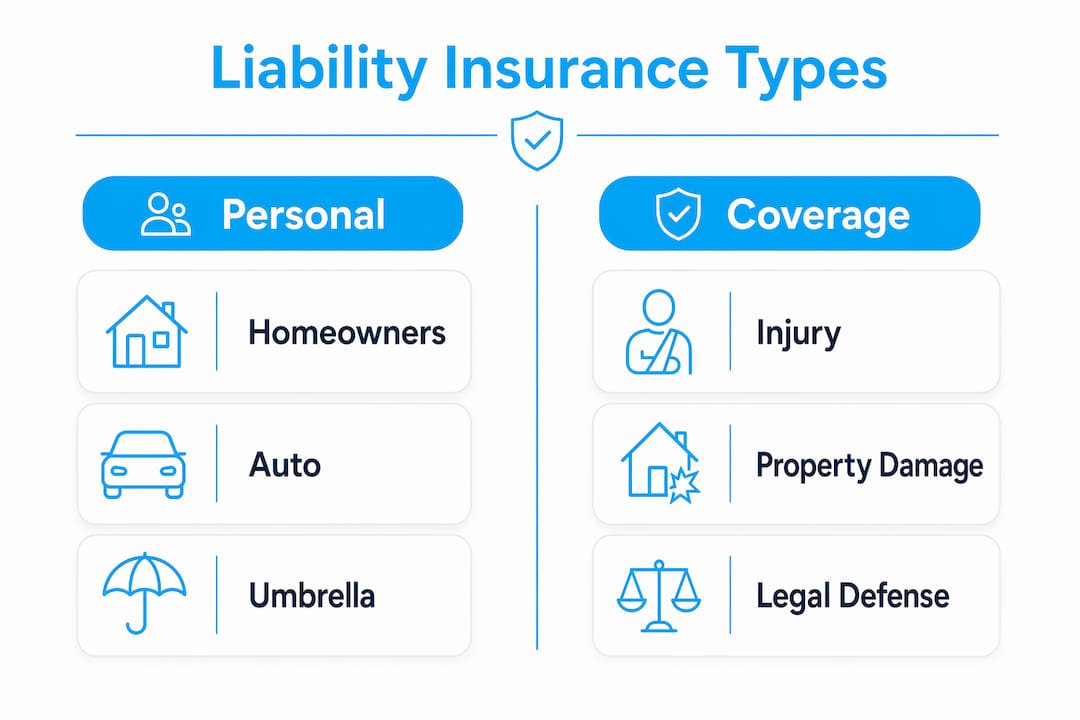

What are the main types of liability insurance for individuals?

Three types of liability insurance apply most directly to individuals and families: personal liability, auto liability, and umbrella liability. Each one covers a different context, and they work together rather than overlap.

| Coverage Type | Where It Applies | What It Covers |

|---|---|---|

| Personal liability (Coverage E) | Homeowners or renters policy | Injury or property damage you cause on or off your property |

| Auto liability | Auto insurance policy | Bodily injury and property damage from a car accident you cause |

| Umbrella liability | Standalone policy | Excess liability above your auto and homeowners limits |

| Professional liability | Separate policy | Errors or negligence in professional services |

| Product liability | Business or commercial policy | Injury or damage caused by a product you sell or manufacture |

Homeowners personal liability (Coverage E) protects you against claims of injury or property damage for which you are legally responsible. It applies on and off your property. If your dog bites a neighbor at the park, Coverage E responds. Legal defense costs are typically included and do not reduce your coverage limit.

Auto liability is the coverage most families think of first. It pays for bodily injury and property damage you cause in a car accident. Most states require a minimum amount, but those minimums are often far too low to cover a serious crash. You can read a full breakdown of how auto liability limits work in Mfandtna’s auto liability explained guide.

Umbrella liability insurance provides excess coverage once your underlying policy limits are exhausted. Umbrella policies typically start at $1 million and extend your protection without replacing your primary policies. They are one of the most cost-effective ways to protect significant assets.

For a deeper look at how personal and commercial liability differ, Mfandtna’s article on general vs. professional liability explains the key distinctions clearly.

How do liability coverage limits work?

Liability limits define the maximum your insurer will pay for a covered claim. Any amount above that limit becomes your personal responsibility. This is the detail most families miss until it is too late.

Auto liability limits are written as three numbers, such as 100/300/100. The first number is the per-person bodily injury limit in thousands. The second is the per-accident bodily injury limit. The third is the property damage limit. So 100/300/100 means $100,000 per person, $300,000 per accident, and $100,000 for property damage.

Here is why those numbers matter in practice:

| Scenario | Claim Amount | Your Limit | You Owe |

|---|---|---|---|

| Minor fender bender | $8,000 | $100,000 | $0 |

| Serious injury, one person | $100,000 | $100,000 | $0 |

| Serious injury, one person | $250,000 | $100,000 | $150,000 |

| Multi-vehicle accident | $400,000 | $300,000 | $100,000 |

Liability limits represent the maximum the insurer will pay. A $100,000 limit against a $250,000 judgment leaves $150,000 owed personally. That gap can force the sale of assets or garnish future wages.

Legal defense costs are covered under most liability policies and generally do not count against your policy limit. That means your insurer pays your attorney even while the claim is being disputed, without eating into the money available for a settlement.

Pro Tip: Review your homeowners liability limit annually. Many policies default to $100,000, but financial advisors commonly recommend $300,000 or more for families with meaningful assets.

How do you choose the right liability coverage level?

Choosing the right coverage level starts with an honest look at what you own and what you earn. Assessing your net worth and potential future income is the recommended starting point, not simply matching state minimums.

Here are the key factors to weigh:

- Your assets. Savings accounts, home equity, investment accounts, and retirement funds are all at risk in a lawsuit. Your coverage should be at least equal to your total net worth.

- Your income. Courts can garnish future wages if a judgment exceeds your assets. High earners face greater exposure even if their current savings are modest.

- Your risk profile. A family with a teenage driver, a swimming pool, or a large dog faces higher liability exposure than average.

- State minimums. Carrying minimum state limits is risky. Financial advisors recommend higher limits to prevent catastrophic out-of-pocket costs.

Once your primary auto and homeowners limits are set, an umbrella policy fills the gap above them. Umbrella coverage is a cost-effective way to substantially increase protection for individuals with assets exceeding primary policy limits. A $1 million umbrella policy typically costs a few hundred dollars per year.

Pro Tip: Coordinate your umbrella policy with your auto and homeowners insurer. Umbrella policies require minimum underlying limits, so confirm your primary policies meet those thresholds before you buy.

One common pitfall is treating each policy as separate. Your auto, homeowners, and umbrella policies should function as a layered system. Gaps between them can leave you exposed in ways that are not obvious until a claim occurs. Mfandtna’s guide on homeowners coverage types explains how personal liability fits within the broader homeowners policy structure.

What does liability coverage typically exclude?

Liability coverage has clear boundaries. Knowing what it does not cover is just as important as knowing what it does.

Common exclusions across personal liability policies include:

- Intentional acts. If you deliberately cause harm, no liability policy will cover the resulting claim. Coverage applies only to accidents and negligence.

- Criminal conduct. Any act that results in a criminal charge is excluded from liability coverage.

- Auto accidents under homeowners policies. Your homeowners liability does not cover car accidents. Auto liability is a separate coverage for that purpose.

- Business activities. Running a business from home does not extend your homeowners liability to business-related incidents. A separate commercial or professional liability policy is required.

- Professional errors. A doctor, lawyer, or financial advisor who makes a professional mistake needs professional liability coverage, not general personal liability.

Umbrella policies follow the form of the underlying policy and do not cover gaps excluded by primary policies. An umbrella will not broaden your coverage. It only extends the dollar amount of protection you already have. If your homeowners policy excludes a specific incident, your umbrella will exclude it too.

Understanding these exclusions helps you spot coverage gaps before a claim reveals them. A liability insurance overview from a legal perspective can also clarify how claims play out after an accident.

Key Takeaways

Liability coverage is your primary financial defense against lawsuits, and the right limits depend on your assets, income, and risk exposure, not on state minimums.

| Point | Details |

|---|---|

| Core definition | Liability coverage pays others when you are legally at fault for injury or property damage. |

| Three main types | Personal (Coverage E), auto liability, and umbrella policies form a layered protection system. |

| Limits matter | A claim above your limit becomes a personal debt, potentially affecting savings and future wages. |

| Defense costs included | Legal fees are typically covered and do not reduce your available settlement limit. |

| Umbrella fills the gap | Umbrella policies start at $1 million and extend protection beyond primary policy limits cost-effectively. |

Why liability coverage deserves more attention than most families give it

Most people I talk with think of insurance as protection for their stuff. Their car, their house, their furniture. Liability coverage protects something more important: your financial future. A single lawsuit can wipe out decades of savings if your limits are too low.

The misunderstanding I see most often is families who carry the state minimum on their auto policy and assume they are covered. State minimums exist to protect other drivers, not to protect your assets. If you own a home, have a retirement account, or earn a solid income, those minimums leave you exposed in any serious accident.

The other gap I see regularly is the disconnect between auto and homeowners policies. Families buy both but never think about how they work together. Adding an umbrella policy is the fix, and it costs far less than most people expect. For the price of a dinner out each month, you can add $1 million or more in coverage above your existing limits.

My honest recommendation: review your liability limits once a year, especially after major life changes like buying a home, having a child, or getting a pay raise. Your coverage needs to grow with your assets. If you have not looked at your limits recently, there is a good chance they no longer reflect your actual exposure.

— Mike

Liability coverage options from Mfandtna

Mfandtna has helped individuals and families across Massachusetts find the right liability coverage for over 30 years. Whether you need to review your auto liability limits, add personal liability to a homeowners policy, or explore umbrella coverage for broader protection, the team at Mfandtna can walk you through your options without pressure.

Getting started is straightforward. You can request a free insurance quote and speak with an advisor who understands both personal and family coverage needs. Mfandtna works with multiple carriers to find coverage that fits your budget and your risk profile. If you want to review your current auto or homeowners liability limits, the auto insurance services and homeowners insurance services pages are a good place to start.

FAQ

What is the difference between liability and full coverage?

Liability coverage pays for injuries and property damage you cause to others. Full coverage adds collision and comprehensive protection for your own vehicle.

Does homeowners insurance include liability coverage?

Yes. Standard homeowners policies include personal liability coverage (Coverage E), which applies to injury or property damage claims made against you on or off your property.

What happens if a claim exceeds my liability limit?

The amount above your limit becomes your personal financial responsibility. A $250,000 judgment against a $100,000 limit leaves $150,000 owed out of pocket.

Do I need an umbrella policy if I already have auto and homeowners insurance?

An umbrella policy is worth considering if your assets exceed your primary liability limits. Umbrella policies start at $1 million and provide cost-effective excess coverage above your existing policies.

Does liability coverage pay my own medical bills?

No. Liability coverage pays the medical bills of others when you are at fault. Your own medical expenses are covered by health insurance or, in auto accidents, by personal injury protection (PIP) if your state requires it.