Commercial property insurance is defined as a policy that protects your business building, equipment, and inventory against losses from fire, theft, vandalism, and other covered perils. A thorough commercial property insurance comparison goes beyond price shopping. It means evaluating coverage limits, valuation methods, and policy terms side by side to make sure your assets are fully protected. Carriers can charge meaningfully different premiums for equivalent coverage, so comparing policies is one of the most direct ways to save money without sacrificing protection. Mfandtna has helped business owners and property managers navigate these decisions for over 30 years.

What key coverage features to compare in commercial property insurance policies

The foundation of any policy comparison is understanding what each policy actually covers. Commercial property insurance typically protects three asset categories: the building structure itself, business personal property (furniture, equipment, and inventory inside the building), and sometimes improvements you have made to a leased space.

Coverage features vary widely between policies. When you compare options, check each of these elements carefully:

- Building coverage: Protects the physical structure, including walls, roof, and permanently attached fixtures.

- Business personal property: Covers movable assets like computers, machinery, and stock.

- Business interruption: Replaces lost income if a covered event forces you to close temporarily.

- Endorsements: Add-ons that extend coverage for specific risks like equipment breakdown, flood, or earthquake.

- Policy limits and sub-limits: The maximum payout per claim or per category. Bundle policies like BOPs may set sub-limits too low for specialized equipment.

- Deductibles: The amount you pay out of pocket before the insurer pays. Higher deductibles lower your premium but increase your exposure.

One feature that catches many business owners off guard is the coinsurance clause. Coinsurance clauses require you to insure at least 80% of your property’s replacement value. If you fall below that threshold, your insurer reduces your claim payout proportionally. A building worth $1,000,000 insured for only $600,000 triggers a penalty that can cut your settlement by a third or more.

Pro Tip: Ask every insurer to show you the coinsurance clause in writing and confirm the minimum insured value required to avoid penalties before you sign.

Coverage gaps are common in policies that look complete on paper. Flood and earthquake damage are almost never included in standard commercial property policies. Outdoor signage, fencing, and landscaping often have low sub-limits or no coverage at all. Read the exclusions section of each policy, not just the declarations page.

How do valuation methods affect policy comparisons and insurance payouts?

Valuation method is the single most important technical factor in a commercial property insurance comparison. It determines how much money you actually receive after a loss.

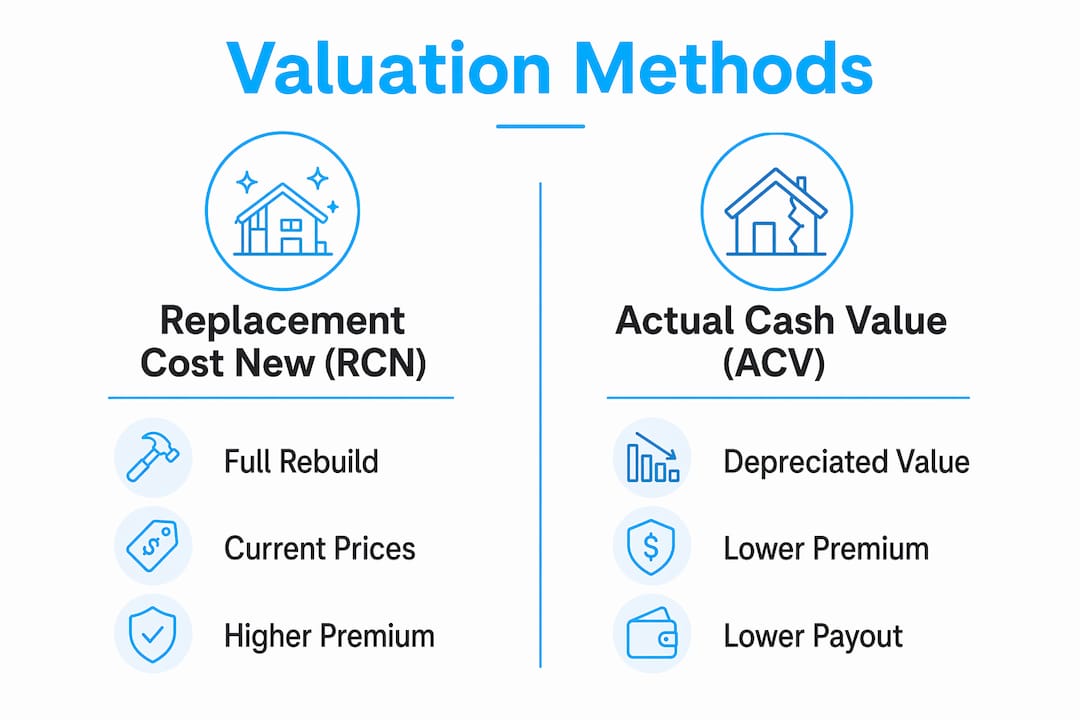

Replacement Cost New (RCN) vs. Actual Cash Value (ACV)

Replacement Cost New (RCN) pays what it costs to rebuild or replace your property with new materials at current prices. Actual Cash Value (ACV) pays RCN minus depreciation. That difference is significant. ACV claim payments can run up to 30% lower than RCN payouts because depreciation deductions shrink the settlement. A 15-year-old roof that costs $80,000 to replace might only receive $50,000 under ACV after depreciation is applied.

| Feature | Replacement Cost New (RCN) | Actual Cash Value (ACV) |

|---|---|---|

| Payout basis | Full rebuild cost at current prices | Rebuild cost minus depreciation |

| Premium level | Higher | Lower |

| Out-of-pocket risk after loss | Low | Can be significant |

| Best for | Most commercial properties | Properties with low-value contents |

| Depreciation impact | None | Reduces payout by age and wear |

ACV policies carry lower premiums, which makes them look attractive when you compare quotes. The real cost only becomes clear after a major loss, when you discover the gap between what the insurer pays and what rebuilding actually costs.

Insurance valuation is also distinct from market value. Insurance valuation must reflect replacement cost, including soft costs like permits, architectural fees, and debris removal. Those soft costs alone add 15–20% on top of hard rebuild costs. A property with a market value of $800,000 may cost $1,100,000 to rebuild when you factor in code compliance upgrades and contractor fees.

Professional appraisals correct this problem. Proper valuation leads to premium savings of 5–15% by aligning your insured value with actual replacement cost. You avoid paying for coverage you do not need, and you avoid the coinsurance penalty trap.

Pro Tip: Update your commercial property appraisal every two to three years. Construction costs shift with inflation, and an outdated valuation quietly creates underinsurance without any warning.

What factors influence commercial property insurance rates and how to compare costs effectively

Commercial property insurance rates are not set by a single formula. Business type, occupancy, and property specifics all influence which carrier fits your risk profile and what premium you will pay. A restaurant carries different fire risk than a law office in the same building. A property in a flood-prone area costs more to insure than an identical building on high ground.

The average small business premium runs about $125 per month, but that figure masks wide variation. Carriers use different rating models, and the annual premium difference for equivalent coverage can exceed $480 between carriers. That gap is real money, and it is why comparing at least three quotes is a minimum standard, not a bonus step.

Here is a numbered approach to comparing costs without making price the only factor:

- Gather your property data first. Square footage, construction type (wood frame vs. masonry), roof age, and occupancy type all drive your quote. Inaccurate inputs produce inaccurate quotes.

- Request quotes on identical coverage terms. Compare RCN to RCN, not RCN to ACV. Mixing valuation methods makes quotes look similar when they are not.

- Check the insurer’s financial strength rating. An “A” rating from AM Best signals the carrier can pay large claims. A lower-rated carrier may offer a cheaper premium but carry more risk of delayed or denied payments.

- Look beyond the base premium. Factor in deductibles, coinsurance requirements, and endorsement costs. A policy with a $500 lower annual premium but a $5,000 higher deductible is not actually cheaper.

- Ask about discounts. Sprinkler systems, monitored alarms, and updated electrical panels often qualify for premium reductions. Many carriers do not volunteer these discounts unless you ask.

Understanding what factors affect your quote before you call an insurer puts you in a much stronger position to evaluate the numbers you receive.

Step-by-step process to compare commercial property insurance policies

A structured comparison process produces better results than collecting quotes at random. Follow these steps to run a thorough evaluation.

Step 1: Assemble your property information

Collect your current policy, any existing appraisal reports, your property’s square footage, construction details, and a list of major equipment and inventory values. Incomplete information leads to inaccurate quotes and coverage gaps. If you have never had a professional appraisal, schedule one before requesting quotes.

Step 2: Define your coverage requirements

Decide which coverage types you need before you contact any insurer. Do you need business interruption coverage? Do you have specialized equipment that requires an endorsement? Knowing your requirements prevents you from being sold coverage you do not need or missing coverage you do.

Step 3: Request quotes from multiple sources

Contact at least three sources: a local independent agency, a regional carrier, and a national carrier. No single insurer fits every business, and the right fit depends on your property type and risk profile. An independent agency like Mfandtna can access multiple carriers simultaneously, which saves time.

Step 4: Build a comparison table

Organize your quotes side by side. Track these fields for each policy:

| Comparison factor | Policy A | Policy B | Policy C |

|---|---|---|---|

| Annual premium | |||

| Valuation method (RCN or ACV) | |||

| Building coverage limit | |||

| Business personal property limit | |||

| Deductible | |||

| Coinsurance requirement | |||

| Business interruption included | |||

| Key exclusions |

Step 5: Evaluate claims handling and financial strength

Price and coverage terms matter, but so does the insurer’s track record. Check AM Best ratings and read customer reviews focused on claims experience. A carrier that delays or disputes claims costs you more than a slightly higher premium ever would.

Pro Tip: Ask each insurer directly: “What is your average time to settle a commercial property claim?” A carrier that cannot answer that question clearly is telling you something important.

Reviewing common insurance mistakes before finalizing your policy helps you catch errors that are easy to overlook when you are focused on price.

What I have learned from 30 years of commercial property comparisons

The biggest mistake I see business owners make is treating commercial property insurance as a commodity. They collect three quotes, pick the lowest number, and move on. That approach works fine until a claim reveals that the cheapest policy had an ACV valuation clause, a coinsurance trap, or a flood exclusion that nobody mentioned.

The second mistake is relying on market value instead of replacement cost for the insured value. A property manager once told me her building was worth $900,000 because that was what it sold for three years earlier. The actual rebuild cost, including soft costs and current contractor rates, was closer to $1,300,000. She was significantly underinsured and did not know it.

Working with a professional appraiser and an independent agent who can access multiple carriers changes the outcome. The appraiser sets the right insured value. The agent shops the market and explains what the policy language actually means. Together, they close the gaps that a direct quote comparison misses.

The insurance market also shifts. Construction costs, reinsurance pricing, and carrier appetite for certain property types all change year to year. A policy that was competitive two years ago may no longer be the best option. Reviewing your coverage annually, not just at renewal, keeps you ahead of those changes.

Choosing between national and local agencies is worth thinking through carefully. Local independent agents often have deeper knowledge of regional risks and carrier relationships that produce better outcomes for complex commercial properties.

— Mike

How Mfandtna helps you compare commercial property coverage

Mfandtna is an independent insurance agency with over 30 years of experience helping business owners and property managers find coverage that fits their actual risk profile, not just their budget.

When you work with Mfandtna, you get access to multiple carriers through a single conversation. The team reviews your property details, walks you through valuation options, and explains policy terms in plain language. You can get free commercial insurance quotes directly through the website and compare options without pressure. If you are starting from scratch or want to understand what commercial property insurance covers before requesting quotes, Mfandtna has resources for that too. The goal is always to match your coverage to your real exposure, at a price that makes sense for your business.

Key takeaways

A thorough commercial property insurance comparison requires evaluating valuation methods, coverage limits, coinsurance terms, and insurer financial strength together, not price alone.

| Point | Details |

|---|---|

| Valuation method drives payout | ACV policies can pay up to 30% less than RCN after depreciation; choose RCN for most commercial properties. |

| Coinsurance clauses carry real risk | Insuring below 80% of replacement value triggers proportional claim reductions that can cost tens of thousands. |

| Soft costs inflate rebuild costs | Permits, debris removal, and code upgrades add 15–20% to hard rebuild costs and must be included in your insured value. |

| Quotes must use identical terms | Comparing an ACV quote to an RCN quote produces a misleading price difference; always match valuation methods. |

| Annual appraisals prevent underinsurance | Construction costs shift with inflation; outdated valuations silently create coverage gaps without any warning. |

FAQ

What is commercial property insurance?

Commercial property insurance is a policy that protects business buildings, equipment, and inventory against losses from fire, theft, vandalism, and other covered perils. It is distinct from general liability insurance, which covers third-party injury or damage claims.

What is the difference between RCN and ACV in commercial property policies?

Replacement Cost New (RCN) pays the full cost to rebuild or replace property at current prices, while Actual Cash Value (ACV) deducts depreciation from that amount. ACV payouts can be up to 30% lower than RCN settlements for the same loss.

How much does commercial property insurance cost for a small business?

The average small business pays about $125 per month for commercial property insurance, but premiums vary significantly by property type, location, and coverage terms. Annual premiums for equivalent coverage can differ by more than $480 between carriers.

What is a coinsurance clause and why does it matter?

A coinsurance clause requires you to insure your property for at least 80% of its replacement value. If your insured value falls below that threshold, your insurer reduces your claim payout proportionally, which can result in a significant out-of-pocket loss.

How often should I update my commercial property insurance valuation?

Update your commercial property appraisal every two to three years, or sooner after major renovations or significant changes in construction costs. Outdated valuations create underinsurance gaps that trigger coinsurance penalties and reduce claim settlements.