Homeowners insurance is a bundled policy that protects your home’s structure, personal belongings, and personal liability in exchange for a regular premium. Most people know they need it, but far fewer understand what it actually covers until they file a claim. Understanding how home insurance works before a loss occurs is the difference between a smooth recovery and a financial shock. This guide breaks down every layer of a standard policy, from core coverage types to exclusions, claims, and how to set limits that actually protect you.

How home insurance works: the six core coverages

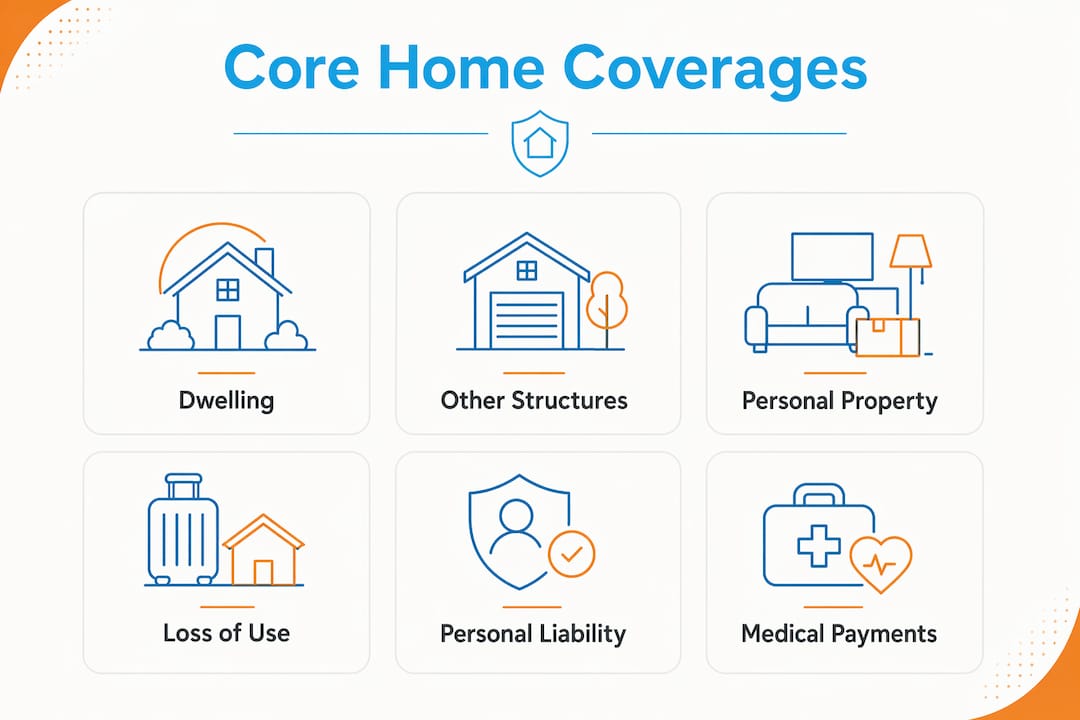

A standard homeowners policy bundles six distinct coverages into one contract. Each one protects a different part of your financial life. Knowing what each covers helps you spot gaps before they cost you.

Here is what each coverage does:

- Coverage A: Dwelling. Pays to repair or rebuild your home’s physical structure after a covered loss, including walls, roof, and built-in appliances.

- Coverage B: Other structures. Covers detached garages, fences, and sheds. This is typically 10% of your dwelling limit.

- Coverage C: Personal property. Protects your furniture, electronics, clothing, and other belongings. Limits usually run 50–70% of your dwelling coverage.

- Coverage D: Loss of use. Pays for hotel stays, restaurant meals, and temporary storage if your home becomes uninhabitable after a covered event. Loss of use is typically set at 20–30% of your dwelling limit.

- Coverage E: Personal liability. Protects you if someone is injured on your property or you accidentally damage someone else’s property. Liability limits commonly start at $100,000 and go up to $300,000 or more. For a deeper look, see liability coverage explained.

- Coverage F: Medical payments. Covers minor medical bills for guests injured on your property, regardless of fault. Limits are typically $1,000–$5,000.

The most common policy form is the HO-3, which covers your dwelling on an open-perils basis and your personal property on a named-perils basis. Open-perils means everything is covered unless specifically excluded. Named-perils means only the events listed in the policy are covered.

| Coverage | What it protects | Typical limit |

|---|---|---|

| Dwelling (A) | Home structure | Your chosen rebuild cost |

| Other structures (B) | Detached buildings | 10% of Coverage A |

| Personal property © | Belongings | 50–70% of Coverage A |

| Loss of use (D) | Temporary living costs | 20–30% of Coverage A |

| Personal liability (E) | Lawsuits and damages | $100,000–$300,000+ |

| Medical payments (F) | Guest injuries | $1,000–$5,000 |

Pro Tip: Ask your agent to confirm whether your personal property is covered on a replacement cost or actual cash value basis. The difference in payout can be significant after a major loss.

What does home insurance cover, and what does it exclude?

Standard policies cover a defined list of perils. Knowing both sides of that list protects you from surprises.

Typically covered perils include:

- Fire and smoke

- Wind and hail

- Lightning strikes

- Theft and vandalism

- Falling objects

- Weight of ice or snow

- Accidental water discharge from plumbing

Common exclusions you need to know:

Floods are excluded from every standard homeowners policy. This is not a technicality. Over 25% of flood claims come from properties in low-risk flood zones, meaning the risk is real even if you do not live near a river or coast. Separate flood insurance through the National Flood Insurance Program (NFIP) or a private insurer is the only way to fill that gap. Learn more about flood and storm coverage gaps.

Earthquakes are also excluded universally. If you live in a seismically active state like California or Oregon, a separate earthquake policy is worth pricing out.

Sewer backup and sump pump failure are two of the most overlooked exclusions. Water backing up through a drain can cause tens of thousands of dollars in damage, yet sewer backup coverage costs only about $40–$75 per year as an endorsement. That is one of the best values in personal insurance.

Mold, wear and tear, and general maintenance issues are also excluded. Insurance covers sudden and accidental damage, not gradual deterioration.

Pro Tip: Review your exclusions list every year. Adding a sewer backup endorsement and confirming flood coverage status takes about 10 minutes and can save you from a five-figure out-of-pocket loss.

How does the home insurance claims process work?

Filing a claim is straightforward when you know the steps. The process starts the moment you discover a covered loss.

- Document the damage immediately. Take photos and video of everything before any cleanup or repairs begin. A thorough visual record strengthens your claim and speeds up the adjuster’s review.

- Contact your insurer. Report the loss as soon as possible. Most insurers have 24-hour claims lines and mobile apps for filing.

- Meet with the adjuster. Your insurer sends an adjuster to assess the damage. Having your own contractor estimate ready gives you a useful comparison point.

- Receive your payout. The insurer calculates your settlement based on your policy’s valuation method, either Actual Cash Value or Replacement Cost Value.

Actual cash value vs. replacement cost value

This distinction matters more than most homeowners realize. Replacement Cost Value (RCV) pays what it costs to replace a damaged item with a new equivalent today. Actual Cash Value (ACV) subtracts depreciation first. A five-year-old sofa worth $1,200 new might pay out only $400 under ACV. Industry guidance favors RCV for most homeowners because it closes the gap between what you lose and what you recover.

Your CLUE report also plays a role here. CLUE stands for Comprehensive Loss Underwriting Exchange. CLUE reports track your claims history for 5–7 years and directly affect your premiums and renewal eligibility. Filing multiple small claims, even ones under your deductible, can trigger premium increases or non-renewal notices. The practical rule is to use insurance for large, genuine losses and self-insure smaller repairs when you can afford to.

Pro Tip: Create a home inventory video once a year. Walk through every room and open every drawer on camera. Store the video in cloud storage. This single habit can dramatically speed up your claims settlement.

How to choose the right coverage amount for your home

Setting the right coverage limits is where most homeowners make costly mistakes. The most common error is insuring a home for its market value instead of its reconstruction cost.

Dwelling coverage must reflect what it would cost to rebuild your home from the ground up, not what you paid for it or what it would sell for today. Market value includes the land beneath your home, which is not insurable property. Reconstruction costs depend on local labor rates, materials, and your home’s square footage and features. In many Massachusetts markets, reconstruction costs run significantly higher than purchase price.

Here is how to set your limits correctly:

- Get a replacement cost estimator. Many insurers provide one free. Independent tools from Marshall and Swift or local contractors give you a second opinion.

- Set Coverage B at 10% of dwelling. This is the standard ratio for detached structures and works for most properties.

- Set Coverage C at 50–70% of dwelling. If you own high-value items, consider whether this is enough.

- Schedule high-value items separately. Jewelry sub-limits in standard policies typically run only $1,500–$2,500. A diamond engagement ring or a coin collection worth $10,000 needs a scheduled floater to be fully covered at appraised value.

- Review after renovations. A kitchen remodel or addition increases your rebuild cost. Policy reviews after improvements are the only way to keep your coverage current.

| Coverage question | Wrong approach | Right approach |

|---|---|---|

| Dwelling limit | Set to market value | Set to reconstruction cost |

| Personal property | Accept default limit | Inventory and adjust |

| High-value items | Rely on sub-limits | Schedule separately |

| Annual review | Skip unless premium changes | Review after any major change |

Understanding coverage limits for property is a discipline, not a one-time task. Your coverage should grow with your home’s value and your possessions.

Key takeaways

Home insurance works by bundling six coverages into one policy that pays for covered losses to your structure, belongings, and liability in exchange for a premium.

| Point | Details |

|---|---|

| Six core coverages | Every standard policy includes dwelling, other structures, personal property, loss of use, liability, and medical payments. |

| Flood is always excluded | Separate NFIP or private flood insurance is required; over 25% of flood claims come from low-risk zones. |

| RCV beats ACV | Replacement Cost Value policies pay more after a loss because they skip depreciation deductions. |

| Insure rebuild cost, not market value | Dwelling limits must reflect reconstruction costs, not purchase price or current sale value. |

| CLUE reports matter | Claims history follows you for 5–7 years and affects your premiums and renewal eligibility. |

What I’ve learned after 30 years of watching homeowners get this wrong

Most homeowners treat their policy like a smoke detector. They install it, forget it, and only think about it when something goes wrong. That habit creates real financial risk.

The biggest mistake I see repeatedly is underinsurance on the dwelling. A homeowner buys a policy, sets the limit at the purchase price, and never touches it again. Five years later, construction costs have risen, they have added a deck and finished the basement, and their coverage is $80,000 short of what a rebuild would actually cost. That gap comes out of their pocket.

The second mistake is filing small claims without thinking about the CLUE consequences. A $900 water damage claim today can cost you $300 per year in premium increases for the next five years. That is a $1,500 loss on a $900 recovery. Think carefully before you file anything under $2,000.

The third thing most articles skip is the value of endorsements. A sewer backup endorsement at $50 per year is one of the smartest $50 you can spend. Scheduled floaters for jewelry or art are inexpensive relative to the coverage they add. These are not upsells. They are genuine gaps in a standard policy that most homeowners do not know exist until it is too late.

My honest advice: read your declarations page once a year, update your home inventory, and call your agent after any renovation. Thirty minutes of attention per year is all it takes to keep your coverage working the way you expect it to.

— Mike

Get personalized home insurance coverage from Mfandtna

Mfandtna has spent over 30 years helping homeowners across Massachusetts and beyond find coverage that actually fits their homes and budgets. Whether you are buying your first home, renovating an existing one, or simply wondering if your current policy has gaps, the team at Mfandtna can review your coverage and recommend the right limits, endorsements, and policy type for your situation.

Getting a quote takes minutes, and there is no pressure to switch. Mfandtna works with multiple carriers, which means you get options rather than a single take-it-or-leave-it offer. Visit the homeowners insurance page to start a free review or get a personalized quote today. You can also browse the homeowners insurance FAQ for quick answers to common coverage questions.

FAQ

What does a standard homeowners insurance policy cover?

A standard HO-3 policy covers your home’s structure, other structures, personal property, loss of use, personal liability, and medical payments for guests. It covers your dwelling on an open-perils basis and personal property on a named-perils basis.

Is flood damage covered by homeowners insurance?

Flood damage is excluded from every standard homeowners policy. You need a separate flood insurance policy through the NFIP or a private insurer to cover flood-related losses.

What is the difference between ACV and RCV in a home insurance claim?

Actual Cash Value pays the depreciated value of a damaged item, while Replacement Cost Value pays what it costs to replace it new today. RCV policies result in higher payouts and are recommended for most homeowners.

How often should I review my homeowners insurance policy?

Review your policy at least once a year and immediately after any home renovation, major purchase, or significant life change. Reconstruction costs and personal property values shift over time, and your coverage limits need to keep pace.

What is a CLUE report and why does it matter?

A CLUE report is a record of your insurance claims history maintained for 5–7 years. Insurers use it to set your premiums and decide whether to renew your policy, so frequent small claims can raise your rates or trigger non-renewal.