Business income insurance is defined as a policy that reimburses your business for lost revenue and ongoing fixed expenses when a covered property loss forces you to suspend or reduce operations. Also called business interruption insurance, it fills the cash flow gap between the moment disaster strikes and the day your doors reopen. Most small businesses access it through a Business Owner’s Policy (BOP), while larger operations add it as an endorsement to a commercial property policy. Without it, a single fire or storm could drain your reserves before repairs are finished.

What is business income insurance and how does it work?

Business income insurance covers the net income your business would have earned, plus the fixed expenses you must keep paying, during the period your operations are interrupted. Think payroll, rent, loan payments, and taxes. The policy does not pay gross revenue. It pays the profit you lost plus the bills that kept coming.

Coverage mechanics follow a specific sequence you need to understand before a claim happens.

- Waiting period: Most policies include a 48 to 72 hour waiting period before benefits begin. This acts as a time deductible. Losses during those first two to three days are yours to absorb.

- Restoration period: After the waiting period, coverage runs for the time needed to repair and reopen. The restoration period often starts at 30 days but can be extended up to 12 months with an endorsement. A restaurant rebuilding after a kitchen fire will likely need the full extension.

- Covered perils: Coverage is triggered by direct physical damage from named perils such as fire, windstorm, or vandalism. Floods, earthquakes, and virus shutdowns are excluded unless you add specific endorsements.

- Extra expense coverage: This companion coverage reimburses costs you would not normally incur, such as renting temporary space or paying overtime to catch up on orders. Extra expense coverage runs alongside your income loss benefits during the restoration period.

Pro Tip: Ask your agent about an extended period of indemnity endorsement. It extends benefits beyond the physical restoration period to cover the time it takes to rebuild your customer base, which standard policies ignore entirely.

What does business income coverage actually cover?

Understanding exactly what gets reimbursed, and what does not, prevents the most painful surprises at claim time.

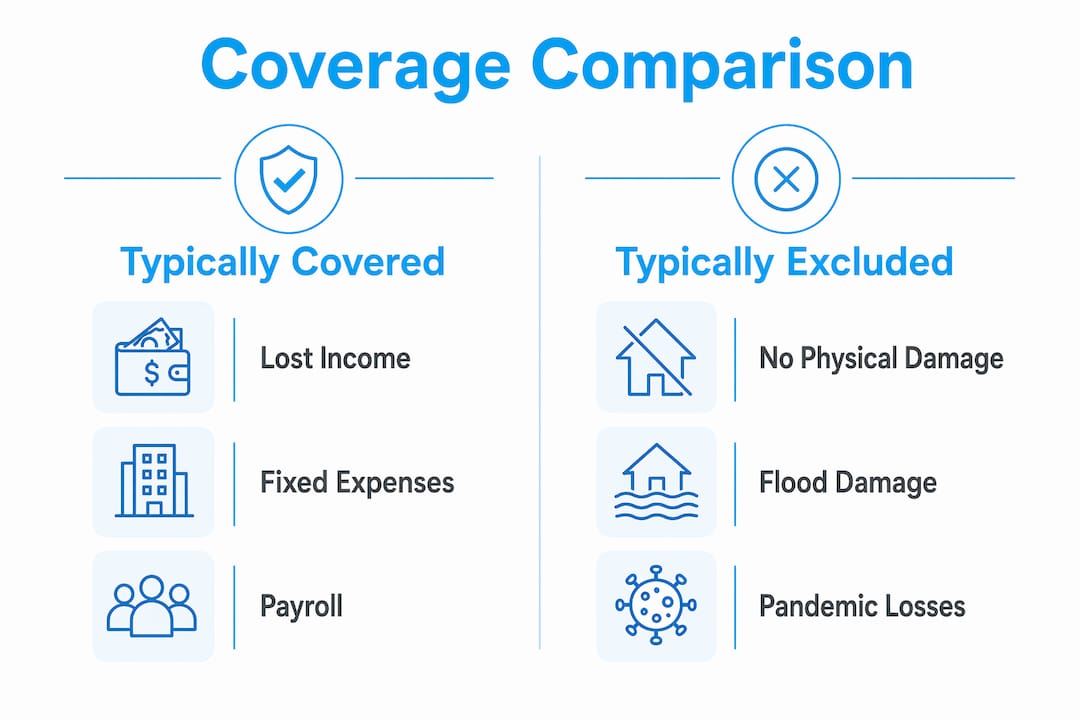

| Typically Covered | Typically Excluded |

|---|---|

| Lost net income during closure | Losses with no physical property damage |

| Payroll for retained employees | Flood or earthquake losses (without endorsement) |

| Rent or mortgage payments | Pandemic or virus-related shutdowns |

| Loan payments and taxes | Utilities in some policy wordings |

| Extra expenses to resume operations | Losses beyond the restoration period |

The distinction between net income and gross revenue matters more than most business owners realize. If your restaurant generates $80,000 per month in revenue but carries $60,000 in variable costs, your covered income loss is roughly $20,000 per month, not $80,000. Sizing your policy on gross revenue leads to overpaying. Sizing it on net income without accounting for fixed costs leads to a gap.

Fixed expenses are treated differently. Rent, payroll for key staff, insurance premiums, and loan payments continue whether you are open or closed. Your policy reimburses those even when net income is zero.

Pro Tip: Read your policy’s definition of “suspension of operations” carefully. Some policies require a complete shutdown to trigger benefits. Others pay for partial suspensions. The difference can be significant for businesses that can operate at reduced capacity after a loss.

For a deeper look at how covered perils affect your policy, Mfandtna’s small business insurance resource breaks down the most common coverage gaps Massachusetts business owners face.

How to calculate the right amount of coverage

Sizing your business income insurance correctly is the step most business owners skip, and it is the one that determines whether a claim actually saves your business.

- List every fixed monthly expense. Include payroll for employees you would retain, rent or mortgage, loan payments, insurance premiums, utilities, and any taxes due. These are the costs that run regardless of revenue.

- Estimate your average monthly net income. Use the last 12 months of financial statements. Average the figure to smooth out seasonal swings.

- Add the two figures together. This is your monthly exposure. A business with $15,000 in fixed costs and $10,000 in average net income needs at least $25,000 per month in coverage.

- Multiply by your expected restoration period. A retail shop in a leased space might realistically reopen in 3 months. A manufacturer with specialized equipment might need 9 to 12 months. Multiply monthly expenses by the restoration period to set your coverage limit.

- Review coinsurance clauses. Many policies include coinsurance requirements ranging from 50% to 125% of estimated annual income. Coinsurance penalties reduce your payout if your coverage limit falls below the required percentage of actual income. Update your business income worksheet every year to stay compliant.

- Consider agreed value options. An agreed value endorsement suspends the coinsurance clause in exchange for an annually updated income estimate. It removes penalty risk but requires discipline to keep the estimate current.

The calculation is not complicated. What makes it hard is that most business owners underestimate their restoration period. A fire that destroys a commercial kitchen does not just require rebuilding. It requires permits, contractor scheduling, equipment lead times, and health inspections. Budget for reality, not the optimistic scenario.

Common misconceptions about business interruption insurance

Several persistent myths lead business owners to buy the wrong coverage or file claims that fall short of their actual losses.

- It is not cash flow insurance. Business income insurance ties coverage to direct physical loss from a covered peril. A supplier going out of business, a key employee leaving, or a slow sales quarter are not covered events. The physical damage trigger is non-negotiable.

- Documentation is everything. Insurers expect detailed, defensible records of pre-loss revenues, payroll, expenses, and repair timelines to support lost income calculations. Businesses that maintain organized financial records before a loss recover faster and more completely than those scrambling to reconstruct records after the fact.

- Claim proceeds are taxable. Business interruption payouts replacing lost profits are treated as ordinary income by the IRS. There is no deferral. Work with a CPA before you file a claim so you understand the tax hit and can plan accordingly.

- Extra expense claims can stand alone. Many business owners assume extra expense coverage only pays when income loss is significant. In fact, extra expense claims can be valid even when income loss is minimal, as long as the costs were necessary to preserve operations during restoration.

- Flood and pandemic losses require separate coverage. COVID-19 litigation clarified this point across the country. Virus shutdowns without physical property damage do not trigger standard business income policies. If your business faces meaningful flood or pandemic risk, ask about separate endorsements or standalone policies.

Understanding these nuances before you buy is far less painful than discovering them during a claim.

Key takeaways

Business income insurance protects your net income and fixed expenses during the restoration period after covered physical property damage, making accurate sizing and documentation the two most critical factors in a successful claim.

| Point | Details |

|---|---|

| Coverage is tied to physical damage | Only direct property loss from covered perils triggers benefits; cash flow disruptions without damage are excluded. |

| Waiting and restoration periods define timing | A 48–72 hour waiting period applies before benefits start; restoration periods can extend up to 12 months. |

| Size coverage on net income plus fixed costs | Multiply monthly net income and fixed expenses by your realistic restoration period to set your coverage limit. |

| Documentation drives claim outcomes | Maintain organized pre-loss financial records to support income and expense calculations at claim time. |

| Tax planning is required | Claim proceeds replacing lost profits are taxable as ordinary income; consult a CPA before and after filing. |

Why i think most business owners buy this coverage wrong

After working with business owners across Massachusetts for years, the pattern I see most often is this: a business owner buys business income insurance as a checkbox, sets the limit based on a rough guess, and never updates it as the business grows. Then a loss happens, and the payout covers maybe 60% of what they actually needed.

The two things I push every client to do are simple. First, run the coverage calculation every year when you renew. Your payroll, rent, and revenue change. Your coverage limit should too. Second, build a pre-loss documentation habit. Keep a folder, physical or digital, with your last 12 months of profit and loss statements, payroll records, and lease agreements. If you ever file a claim, that folder is worth more than the policy itself.

The extra expense coverage piece is the most underused part of this policy. I have seen businesses rent temporary space, pay for expedited equipment delivery, and run double shifts to serve customers during repairs. All of that is reimbursable. Most business owners do not even ask about it because they do not know it exists.

One more thing: if your business sits in a flood zone or depends on a supply chain with weather exposure, a standard business income policy is not enough. You need to have a direct conversation with your agent about endorsements. Aligning your business income coverage with underlying property perils is the only way to close the gaps before they cost you.

— Mike

Protect your business revenue with Mfandtna

A single covered loss can put months of revenue at risk. Mfandtna has helped Massachusetts business owners build customized commercial coverage for over 30 years, and business income protection is one of the most requested and most misunderstood parts of any commercial policy.

Whether you run a retail shop in Arlington, a contractor operation in Boston, or a service business anywhere in between, Mfandtna can help you size your coverage correctly, identify gaps, and find affordable options that fit your actual risk. Get a free business insurance quote today and find out exactly what your business income coverage should look like. No pressure, just straight answers from people who know commercial insurance.

FAQ

What does business income insurance cover?

Business income insurance covers lost net income and ongoing fixed expenses such as payroll, rent, and loan payments during the period your business is closed due to covered property damage. Extra expense coverage can also reimburse additional costs incurred to resume operations faster.

How long does business income coverage last?

The restoration period typically starts at 30 days but can be extended up to 12 months with an endorsement. Coverage begins after a waiting period of 48–72 hours following the covered loss.

Is business income insurance the same as business interruption insurance?

Yes. Business income insurance and business interruption insurance refer to the same coverage. The terms are used interchangeably across the industry, though policy documents may use either name.

Are business income insurance payouts taxable?

Yes. Proceeds that replace lost profits are treated as ordinary income by the IRS and are taxable in the year received. Consult a CPA to plan for the tax impact before and after filing a claim.

Does business income insurance cover flood or pandemic losses?

Standard policies exclude floods, earthquakes, and virus-related shutdowns unless specific endorsements are added. If your business faces these risks, ask your agent about separate coverage options to fill those gaps.