Builders risk insurance is defined as temporary property insurance for construction, covering direct physical loss or damage to a project from the moment work begins until completion. Understanding the builders risk policy coverage scope upfront saves contractors and developers from costly surprises when a claim is denied. Standard policies cover the structure, on-site materials, and temporary installations against perils like fire, theft, windstorm, and vandalism. What they do not cover, including flood, earthquake, and faulty workmanship, matters just as much as what they do.

What does builders risk insurance actually cover?

Most builders risk policies are open-perils forms, meaning they cover any direct physical loss unless the policy specifically excludes it. Named-perils policies, by contrast, cover only the perils listed in the policy document. If a cause of loss is not on that list, the claim is denied. Open-perils forms give you broader protection, but the exclusions still define the real boundaries of your coverage.

The physical property covered under a standard builders risk policy includes:

- Buildings and structures under construction, including foundations, framing, and installed fixtures

- Materials and supplies stored on-site, such as lumber, piping, and electrical components

- Materials in transit to the job site, up to policy-specified limits

- Temporary structures like scaffolding, construction fencing, and site trailers

Covered perils under most open-perils policies include fire, lightning, explosion, theft, vandalism, windstorm, hail, and water damage from burst pipes. Each of these represents a real and frequent risk on active construction sites. A framing fire on a residential build in Massachusetts, for example, can destroy weeks of work and tens of thousands of dollars in materials in under an hour.

Coverage also extends to debris removal and related expenses when a covered loss occurs. This matters because debris removal after a fire or storm can cost nearly as much as the physical repairs. Without it in your policy, that cost comes out of your project budget.

Pro Tip: Ask your insurer whether your policy covers materials in transit and at what limit. Many contractors assume transit coverage is automatic, but some policies cap it at a fraction of the on-site material value.

What are the common exclusions in builders risk policies?

The builders risk policy exclusions list is where most coverage disputes originate. Knowing these gaps before a loss occurs is the difference between a paid claim and an out-of-pocket expense.

Standard exclusions in builders risk policies include:

- Flood and earthquake. These perils require separate endorsements or standalone policies. A site in a FEMA flood zone without flood coverage is fully exposed.

- Employee theft. Dishonest acts by employees and mechanical breakdown are excluded from standard coverage. A fidelity bond or crime policy fills this gap.

- Faulty workmanship, design, or materials. The policy will not pay to redo defective work. However, physical damage to other property caused by that defect may be covered depending on policy language.

- Wear and tear and mechanical breakdown. Equipment that fails due to age or normal use is not a covered peril.

- Land, government action, and war. These are universal exclusions across virtually all property insurance forms.

- Work stoppage. If construction halts for an extended period, some policies suspend or void coverage entirely.

The faulty workmanship exclusion deserves special attention. Policies typically deny paying to redo defective work but may cover physical damage caused by faulty work if that damage relates to a covered peril. This is called the “resulting damage” clause. Insurers interpret this clause differently, and the outcome of a claim can hinge entirely on the specific policy language.

“Coverage scope depends more on specific policy exclusions and endorsements than the general ‘construction coverage’ label, influencing actual protection boundaries.” — LegalClarity

Read every exclusion in your policy before the project starts. Do not wait until you file a claim to learn what is not covered.

How do endorsements expand your builders risk coverage scope?

Endorsements are add-ons that modify the base policy to cover risks the standard form excludes. They are the primary tool for customizing construction insurance coverage to match your actual project exposure.

| Endorsement | What It Covers | When You Need It |

|---|---|---|

| Flood coverage | Storm surge, heavy rain, rising water | Sites in flood zones or coastal areas |

| Earthquake coverage | Ground movement and resulting structural damage | Projects in seismic risk areas |

| Soft costs | Loan interest, real estate taxes, carrying costs from delays | Any project with financing |

| Testing coverage | Damage during equipment startup and system testing | Commercial and industrial builds |

| Debris removal upgrade | Costs above the base policy limit | Large or complex structures |

Soft cost endorsements cover financial losses like extended loan interest, real estate taxes, and other carrying costs from delays caused by covered perils. On a $2 million commercial project, a three-month delay can generate tens of thousands of dollars in carrying costs alone. Without a soft cost endorsement, those losses are not recoverable.

Builders risk premiums generally range from 1 to 5 percent of total construction project value based on coverage extent and endorsements. A $500,000 project could cost between $5,000 and $25,000 to insure. Adding flood, earthquake, and soft cost endorsements pushes the premium toward the higher end of that range, but the financial protection they provide far exceeds the added cost on most projects.

Pro Tip: Price endorsements individually before bundling. Some carriers charge disproportionately for flood coverage on low-risk sites. Compare quotes with and without each endorsement to identify where you are paying for coverage you genuinely need versus coverage that is unlikely to apply.

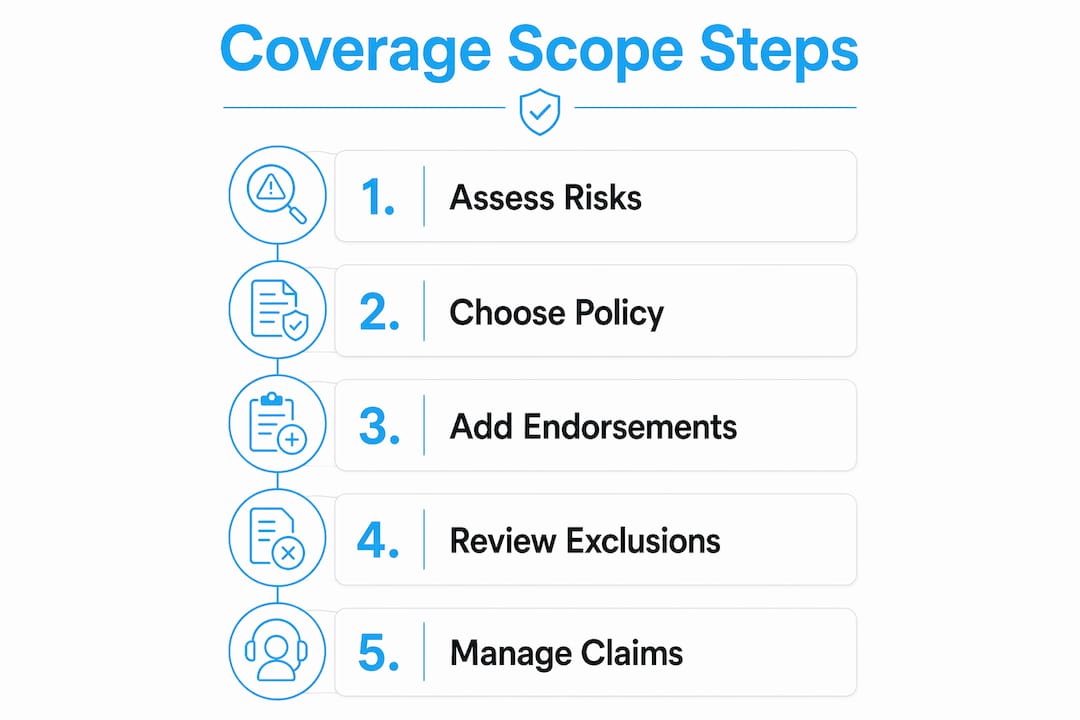

What steps help you manage your builders risk policy effectively?

Getting the right coverage for building projects requires more than signing a policy and moving on. Active management throughout the project lifecycle protects your coverage and supports successful claims.

- Review the declarations page and coverage form together. The declarations page lists limits and named endorsements. The coverage form defines what those terms actually mean. Read both.

- Work with an agent who specializes in construction risks. A generalist agent may not flag the resulting damage clause or recommend a soft cost endorsement. Specialized agents know which exclusions create the most exposure for your project type.

- Declare the full project scope and value accurately. Underreporting the project value to lower premiums creates a coinsurance problem. If you insure a $1 million project for $600,000 and suffer a $300,000 loss, the insurer may only pay a proportional share.

- Document construction stages and material values. Maintain a running record of materials delivered, installed, and stored. This documentation supports your claim value if a loss occurs mid-project.

- Monitor your coverage end date. Builders risk policies terminate on project completion. If the project runs long, you need to extend the policy before it lapses. A gap in coverage, even for a few days, leaves the project fully exposed.

- Avoid common mistakes. The most frequent errors are undervaluing the project, skipping soft cost endorsements on financed builds, and failing to add flood coverage on sites with any water exposure.

The builders risk insurance application guide from Mfandtna walks through each of these steps in detail, including how to document project values and select the right endorsements for your build type.

Key takeaways

Builders risk policy coverage scope is defined by the combination of covered perils, physical property included, and the exclusions and endorsements that modify the base form.

| Point | Details |

|---|---|

| Open-perils vs. named-perils | Open-perils policies cover all losses except exclusions; named-perils cover only listed causes. |

| Core exclusions to know | Flood, earthquake, employee theft, and faulty workmanship are excluded from standard policies. |

| Endorsements fill the gaps | Soft cost, flood, and earthquake endorsements extend coverage for the most common exposure gaps. |

| Accurate project valuation matters | Underreporting project value can reduce your claim payout proportionally at the time of loss. |

| Policy ends at completion | Builders risk coverage terminates when construction finishes; transition to permanent property insurance immediately. |

What I’ve learned from watching builders risk claims go sideways

After more than 30 years of placing construction insurance coverage across Massachusetts and beyond, the pattern I see most often is this: contractors buy a policy, assume it covers everything construction-related, and never read the exclusions. Then a loss happens, and the denial letter arrives citing a clause they never knew existed.

The resulting damage clause is the one that surprises people most. I have seen claims where a subcontractor’s error caused a pipe to fail, which then flooded two floors of a partially built commercial building. The insurer denied the cost to fix the faulty pipe work but covered the water damage to the structure and materials. That distinction saved the contractor a significant amount, but only because the policy language supported it. A different carrier’s form might have denied the entire claim.

Soft cost endorsements are the second most overlooked protection. Developers with construction loans rarely think about what happens to their financing costs when a fire pushes the project back four months. Those carrying costs are real losses. They belong in your coverage.

My advice is straightforward: sit down with a construction-focused insurance agent before you break ground, not after. Bring your project plans, your financing documents, and your subcontractor list. A good agent will identify the gaps before they become claims.

— Mike

Mfandtna’s builders risk insurance solutions for contractors

Mfandtna has specialized in builders risk insurance for contractors and developers across Massachusetts for over 30 years. The team helps you identify coverage gaps, select the right endorsements, and get a policy that matches your actual project scope, not a generic form that leaves you exposed.

Whether you are building a single-family home in Arlington or managing a multi-unit commercial project in Boston, Mfandtna provides affordable, customized builders risk coverage options with clear explanations of what is and is not covered. Get a free insurance quote today and work with an agent who understands construction risk from the ground up.

FAQ

What does builders risk insurance cover?

Builders risk insurance covers direct physical loss or damage to a structure under construction, including materials on-site, in transit, and temporary installations. Covered perils typically include fire, theft, windstorm, vandalism, and explosion under open-perils forms.

What are the most common builders risk policy exclusions?

The most common exclusions are flood, earthquake, employee theft, faulty workmanship, mechanical breakdown, and wear and tear. These exclusions require separate endorsements or standalone policies to fill the coverage gap.

How does a soft cost endorsement work?

A soft cost endorsement covers financial losses like extended loan interest and carrying costs caused by construction delays from a covered peril. It does not cover delays from excluded causes like faulty workmanship.

When does builders risk coverage end?

Builders risk coverage ends when the project reaches completion. After that point, you need a commercial property or homeowners policy to cover the finished structure and its contents.

How much does builders risk insurance cost?

Premiums typically range from 1 to 5 percent of the total construction project value. A $500,000 project could cost between $5,000 and $25,000 depending on the coverage scope and endorsements selected.