Commercial property insurance is a policy that protects your business’s physical assets from damage caused by events like fire, theft, vandalism, and storms. Whether you own your building or lease office space, this coverage shields the physical foundation of your operation. Without it, a single fire or burst pipe could force you to pay out of pocket for repairs, replacement equipment, and lost revenue. For business owners and commercial property managers, understanding this coverage is the first step toward protecting what you have built.

What is commercial property insurance and what are its coverage levels?

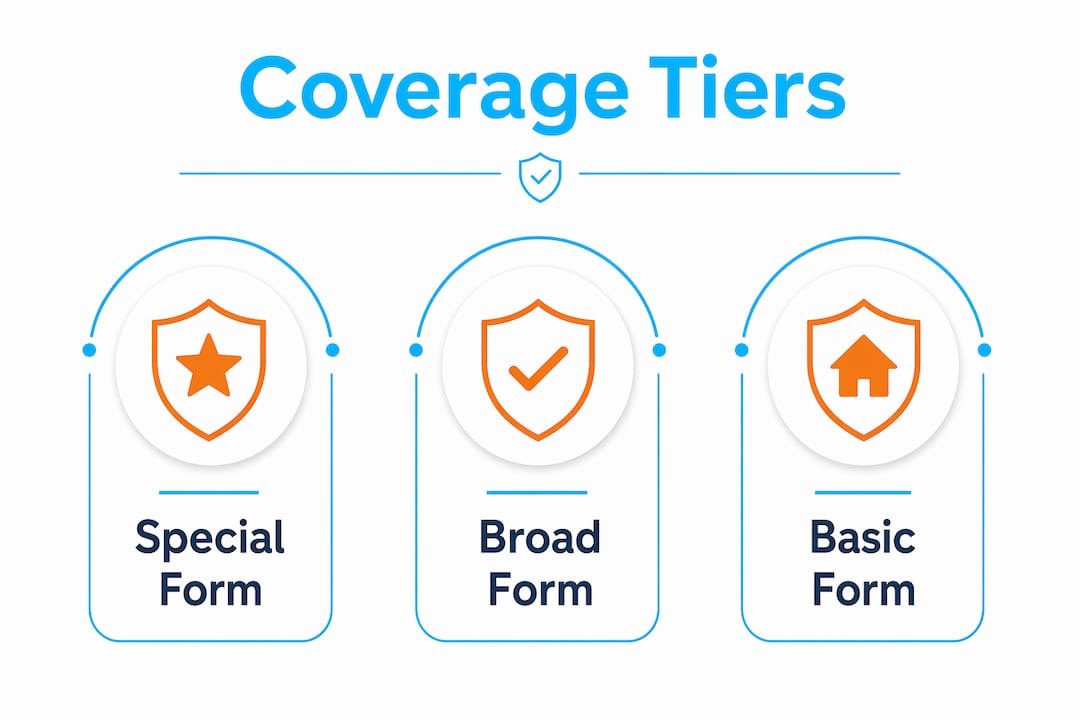

Commercial property insurance comes in three distinct coverage tiers, and the one you choose determines exactly what gets paid after a loss. Knowing the difference between them saves you from expensive surprises at claim time.

Basic form covers a defined list of named perils only. These include fire, windstorm, hail, explosion, vandalism, and smoke damage. If your loss is not on that list, the policy does not pay. Basic form is the most affordable option, but it leaves significant gaps for businesses in areas prone to winter weather or water damage.

Broad form adds several perils on top of Basic. It picks up damage from falling objects, the weight of snow or ice, leaking appliances, and structural collapse. A retail shop in Massachusetts that suffers a roof collapse from heavy snow accumulation would be covered under Broad form but not Basic. That distinction matters enormously when you are filing a claim.

Special form, also called all-risk coverage, covers every cause of loss except those the policy specifically excludes. This is the most protective option and the one most insurance professionals recommend for businesses with significant physical assets. You are covered unless the policy says otherwise, which reverses the burden compared to Basic and Broad form.

| Coverage Level | Covered Perils | Best For |

|---|---|---|

| Basic form | Fire, windstorm, vandalism, explosion | Low-asset businesses, tight budgets |

| Broad form | Basic perils plus snow, falling objects, leaking appliances | Mid-size operations with moderate risk |

| Special form | All perils except listed exclusions | Businesses with high-value assets or complex operations |

Pro Tip: If your business holds expensive equipment, inventory, or irreplaceable records, Special form is worth the higher premium. The cost difference between Broad and Special form is often smaller than business owners expect.

What does commercial property insurance typically cover?

Commercial property coverage extends well beyond the four walls of your building. Most policies protect several categories of property and loss simultaneously.

Physical structures and business personal property

The policy covers the building itself if you own it, including permanently installed fixtures, flooring, and built-in systems. It also covers business personal property, which includes furniture, computers, machinery, tools, and inventory. If a customer leaves equipment in your care and it gets damaged in a covered event, many policies extend coverage to that property as well.

Business income and extra expense coverage

Business income coverage pays the net earnings your business loses while it cannot operate after a covered loss. Extra expense coverage pays the additional costs you incur to resume operations faster, such as renting temporary space or equipment. These two coverages together are what allow a business to survive a major disruption rather than close permanently.

What commercial property insurance does not cover

Knowing the exclusions is just as important as knowing what is covered. Standard policies exclude:

- Flood damage (requires a separate flood policy)

- Earthquake and earth movement damage

- War and nuclear incidents

- Wear and tear or gradual deterioration

- Damage from vermin or insects

Most exclusions involve natural disasters that require their own standalone policies. If your business sits in a flood zone or earthquake-prone region, you need separate coverage for those risks. Checking your policy’s exclusion list before a loss occurs is the only way to avoid a denied claim.

For a broader look at how coverage gaps appear in property policies, the guide on common coverage gaps offers useful context that applies to commercial situations as well.

Why is commercial property insurance important for business owners?

No state legally requires commercial property insurance as of 2026. That fact surprises many business owners. The real pressure to carry coverage comes from contracts, not laws.

Landlords, mortgage lenders, and the Small Business Administration all impose insurance requirements through agreements. SBA loans over $25,000 typically require the borrower to carry commercial property insurance as a condition of funding. Commercial leases almost always include an insurance clause specifying minimum coverage amounts. Violating those clauses can trigger lease termination or loan default.

The distinction between owner and tenant coverage is one area where business owners frequently get caught off guard. Landlord insurance covers the building structure, but it does not cover your equipment, furniture, inventory, or leasehold improvements. As a tenant, you are responsible for insuring everything you bring into the space and any improvements you make to it.

Here is what you need to review before signing any commercial agreement:

- Your lease’s insurance requirements section

- The minimum coverage limits your landlord specifies

- Your lender’s collateral protection requirements

- Whether your improvements are covered under your policy or the landlord’s

Pro Tip: Ask your landlord for a copy of their insurance certificate before you sign a lease. Knowing what their policy covers tells you exactly where your own coverage needs to begin.

For business owners navigating commercial lease insurance clauses, understanding what your landlord requires in writing protects you from gaps that only surface after a loss.

Avoiding common small business insurance mistakes starts with reading every contract clause before you agree to it.

How do valuation methods affect your claim payout?

The way your policy values property at the time of a claim determines how much money you actually receive. Two methods dominate commercial property insurance: replacement cost and actual cash value (ACV).

Replacement cost coverage pays what it costs to repair or replace damaged property at today’s prices, with no deduction for age or wear. If a fire destroys a five-year-old commercial oven, replacement cost pays for a new equivalent oven at current market prices.

Actual cash value subtracts depreciation from that same calculation. That five-year-old oven might be worth 40% less than its replacement cost after depreciation. ACV policies cost less in premiums, but they can leave you significantly short of what you need to rebuild after a major loss.

| Valuation Method | How It Works | Risk |

|---|---|---|

| Replacement cost | Pays current price to replace property | Higher premium, full recovery |

| Actual cash value | Pays replacement cost minus depreciation | Lower premium, potential shortfall |

Coinsurance clauses add another layer of complexity. Coinsurance requirements typically require you to insure your property to at least 80–90% of its total value. If you insure below that threshold, the insurer reduces your claim payout proportionally, even if your loss is smaller than your policy limit. A business that insures $500,000 worth of property for only $300,000 will face a penalty on every claim it files.

Pro Tip: Choose replacement cost over ACV whenever your budget allows. The premium difference is real, but the gap between ACV and full recovery after a total loss is far larger.

Key Takeaways

Commercial property insurance protects your business’s physical assets, income, and contractual standing, and choosing the right valuation method and coverage form determines whether a claim fully rebuilds your operation.

| Point | Details |

|---|---|

| Three coverage tiers exist | Basic, Broad, and Special form offer increasing protection levels for different risk profiles. |

| Coverage goes beyond buildings | Policies protect equipment, inventory, and lost income, not just physical structures. |

| Contracts drive requirements | Landlords, lenders, and SBA loans require coverage even though no state law mandates it. |

| Valuation method matters | Replacement cost pays full current value; ACV deducts depreciation and can leave you short. |

| Exclusions require separate policies | Flood and earthquake damage are not covered and need standalone policies. |

What I have learned after 30 years of placing commercial policies

Business owners consistently underestimate how much their physical assets are worth until they file a claim. I have seen clients insure a property for what they paid for it years ago, only to discover that rebuilding costs have risen significantly since then. That gap between insured value and actual replacement cost is where businesses get hurt the most.

The other mistake I see regularly is treating commercial property insurance as a checkbox item. Owners buy the minimum required by their lease, never review it again, and then discover their coverage has not kept pace with their growth. A business that adds $200,000 in new equipment over three years needs to update its policy to match. Annual reviews are not optional if you want your coverage to actually work.

Cookie-cutter policies are another problem. A restaurant has completely different risk exposures than a law office or a warehouse. The right policy reflects your specific operations, your lease terms, and your asset values. Generic coverage packages often miss the details that matter most when you file a claim.

My honest advice: work with an independent agency that will sit down with you, review your lease and loan documents, and build coverage around your actual situation. The premium savings from a bare-bones policy rarely justify the exposure.

— Mike

How Mfandtna helps you protect your business assets

Mfandtna has spent over 30 years helping business owners across multiple states find commercial property coverage that fits their actual operations, not just their budget.

Getting the right policy starts with a conversation, not a form. Mfandtna’s team reviews your lease terms, loan requirements, and asset values to build coverage that holds up when you need it. Whether you need a standalone commercial property policy or want to bundle it with general liability through a Business Owner’s Policy, Mfandtna can compare options across multiple carriers to find the right fit. Request your free commercial insurance quote today and get personalized advice from an experienced independent agent.

FAQ

What does commercial property insurance cover?

Commercial property insurance covers physical structures, business personal property such as equipment and inventory, and business income lost during a covered interruption. Most policies also extend to customer property in your care during a covered event.

Is commercial property insurance legally required?

No state legally requires commercial property insurance as of 2026. However, landlords, mortgage lenders, and SBA loans over $25,000 commonly require it as a condition of their agreements.

What is the difference between replacement cost and actual cash value?

Replacement cost pays the current price to repair or replace damaged property. Actual cash value pays that amount minus depreciation, which can leave you with less money than you need to fully recover.

Does commercial property insurance cover floods?

Standard commercial property policies exclude flood damage. Businesses in flood-prone areas need a separate flood insurance policy to cover that risk.

Can commercial property insurance be bundled with other coverage?

Yes. Commercial property coverage can be combined with general liability in a Business Owner’s Policy or a Commercial Package Policy, which often provides better pricing and simplified management for small and mid-size businesses.