An independent insurance agency is defined as a licensed insurance producer that works with multiple insurance companies to offer clients a range of coverage options tailored to their needs. Unlike agents tied to a single insurer, independent agents can compare policies across carriers and recommend the best fit for your situation. This distinction matters because it directly affects your choices, your pricing, and the quality of advice you receive. Mfandtna has operated as an independent agency for over 30 years, helping families and individuals across Massachusetts find coverage that actually fits their lives.

What is an independent insurance agency and how does it differ from captive agencies?

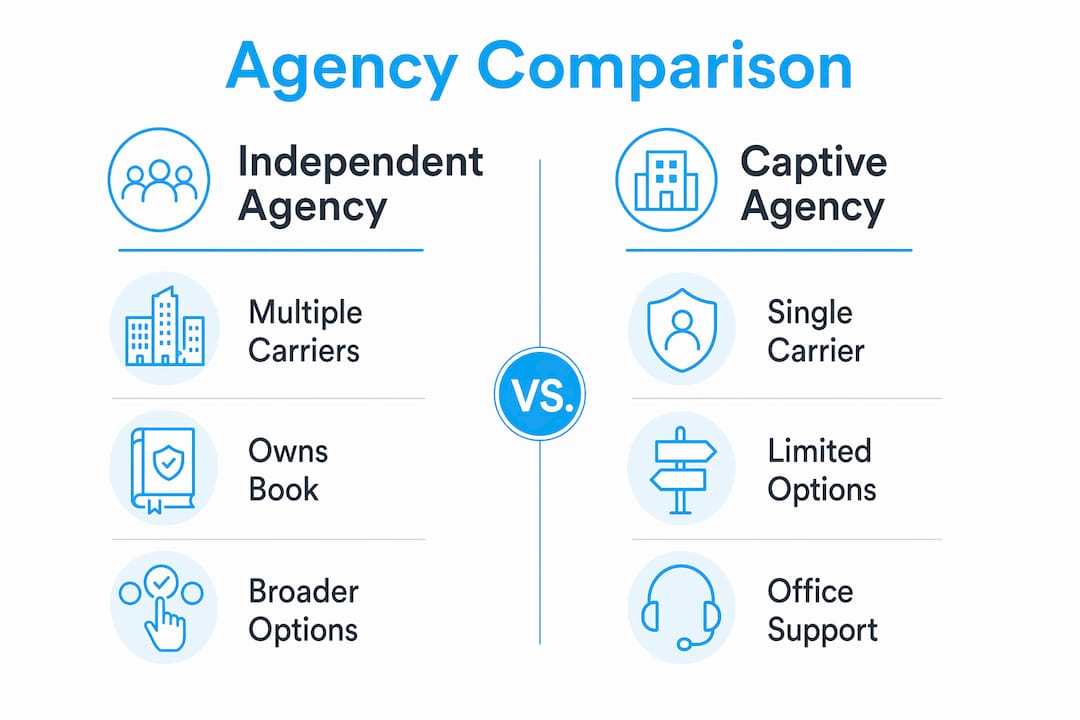

An independent insurance agent is a licensed producer who works with multiple insurance companies, offering clients diverse choices and pricing options. A captive agent, by contrast, represents only one insurer and can only sell that company’s products. That single-carrier limitation means captive agents cannot shop the market for you, even if a better policy exists elsewhere.

Independent agencies contract with several carriers at once. This lets them compare coverage terms, deductibles, and premiums side by side before making a recommendation. The result is a more complete picture of what the market offers for your specific risk profile.

The operational differences go beyond product variety. Independent agents own their book of business, meaning they can move clients between carriers when a better option becomes available. Captive agents cannot do this. That flexibility is one of the clearest advantages of working with an independent agency.

| Feature | Independent agency | Captive agency |

|---|---|---|

| Carrier access | Multiple insurers | Single insurer only |

| Policy comparison | Side-by-side quotes | One company’s options |

| Client portability | Can switch carriers freely | Cannot move clients |

| Ongoing advocacy | Policy reviews and claims support | Limited to one carrier’s process |

| Ownership of client relationships | Agent owns the book of business | Carrier owns the relationship |

Pro Tip: When you request quotes, ask your agent how many carriers they actively work with. An agency with access to a broad panel of insurers gives you more real options, not just the appearance of choice.

How are independent insurance agencies regulated and licensed?

Independent agencies are not unregulated intermediaries. They are licensed professionals subject to state insurance laws, continuing education requirements, and suitability standards. The NAIC reports over 2 million licensed insurance producers and more than 236,000 business entities operating under state regulatory oversight in the U.S. That scale reflects a mature, well-governed profession.

Each state’s insurance commission sets the rules for licensing, renewal, and conduct. Agents must pass licensing exams, complete ongoing education, and follow consumer protection guidelines. Failing to meet these standards puts their license at risk.

NARAB II enables licensed producers to sell insurance across multiple states through a streamlined multistate licensing process. This matters for families who move or own property in more than one state. It preserves each state’s consumer protection authority while reducing the administrative burden on agents who serve clients across state lines.

Key regulatory protections you have as a consumer include:

- The right to verify your agent’s license through your state’s insurance department website

- Suitability requirements that obligate agents to recommend coverage appropriate for your situation

- Continuing education mandates that keep agents current on products, laws, and market changes

- Complaint processes through state insurance commissioners if a dispute arises

Independence from a single carrier does not mean independence from oversight. It means your agent has more tools to serve you while still operating within a regulated framework.

How do independent insurance agents get paid?

Independent agents earn commissions primarily through premiums on policies placed and renewed, with opportunities for growth through performance bonuses. The commission percentage varies by carrier and product type. Renewal commissions are a key part of the model. They give agents a financial reason to keep you satisfied and your coverage current year after year.

This structure creates a natural alignment between agent income and client retention. An agent who keeps you well-covered and happy earns renewal income. An agent who places you in the wrong policy risks losing you at renewal. That said, you should understand how the model works so you can ask the right questions.

Consumers should confirm that agent recommendations prioritize coverage suitability, not only the lowest premiums. Commission rates differ across carriers, which means an agent could theoretically favor a higher-commission product. Being informed reduces the risk of underinsurance or policies that do not match your actual needs.

Pro Tip: Ask your agent to explain why they are recommending a specific carrier over others. A confident, specific answer about coverage terms and pricing is a good sign. A vague answer focused only on price is worth probing further.

What practical benefits do families and individuals get from independent agencies?

Independent agents provide one advisor to shop across multiple insurers, offering side-by-side coverage options and ongoing advocacy including claims guidance. That single point of contact simplifies what would otherwise require you to contact several companies on your own. You save time and get a more complete comparison.

The benefits of local independent insurance agents go beyond convenience. A local agent understands area-specific risks, whether that means coastal flooding exposure, winter weather damage, or local traffic patterns that affect auto rates. That context shapes better coverage recommendations than a national call center can provide.

Independent agents act as advocates during claims and policy questions, explaining coverage details and negotiating with carriers on your behalf. This is where the relationship pays off most clearly. Filing a claim is stressful. Having someone who knows your policy and can speak directly with the carrier on your behalf changes the experience significantly.

Additional practical benefits include:

- Access to homeowners insurance options from multiple carriers, giving you real pricing competition

- Annual policy reviews that catch coverage gaps before they become costly

- Ability to bundle home, auto, and other lines through one agency for coordinated coverage

- Flexibility to adjust coverage as your family’s needs change, such as adding a teen driver or purchasing a new home

How can you choose and work with an independent insurance agency effectively?

Choosing the right agency starts with verifying credentials. Every licensed agent’s status is publicly searchable through your state’s insurance department. Confirming licensure takes two minutes and confirms you are working with a regulated professional.

Here are five steps to select and engage with an independent insurance agency:

- Verify the agent’s license through your state insurance department’s online lookup tool before any conversation about coverage.

- Ask how many carriers they work with and which lines of insurance they specialize in. An agency focused on personal lines should have strong carrier relationships in home, auto, and umbrella coverage.

- Request a written comparison of at least two carrier options for your primary coverage need. This shows you the agent is actually shopping the market, not defaulting to one carrier.

- Ask about their claims support process. A good agency explains exactly how they assist clients when a claim is filed, not just at the point of sale.

- Schedule an annual review. Your coverage needs change. A proactive agency reaches out before renewal to confirm your policy still fits your situation.

You can also review questions to ask your insurance agency before your first meeting to prepare a stronger conversation. The goal is a long-term relationship, not a one-time transaction.

Key Takeaways

An independent insurance agency gives you access to multiple carriers, licensed professional advice, and ongoing advocacy that a single-carrier agent cannot match.

| Point | Details |

|---|---|

| Core definition | Independent agents are licensed producers who work with multiple insurers, not tied to one carrier. |

| Regulatory oversight | State insurance commissions, NAIC standards, and NARAB II govern all licensed independent agents. |

| Commission transparency | Agents earn renewal commissions, so ask why a specific carrier is recommended to confirm suitability. |

| Consumer benefits | You get side-by-side quotes, claims advocacy, and annual policy reviews through one trusted contact. |

| Choosing an agency | Verify licensure, request written comparisons, and confirm the agency’s claims support process upfront. |

Why independence is the feature that matters most

After working in this industry for over 30 years, the single thing I keep coming back to is this: independence is not just a business model. It is a service commitment.

When I sit down with a family to review their coverage, I am not limited to one company’s product sheet. I can look at what five or six carriers are offering and tell you honestly which one fits your situation best this year. That changes the conversation entirely. It shifts the dynamic from “here is what we have” to “here is what the market offers and here is what I recommend for you.”

What surprises most people is how much the relationship matters after the sale. Placing a policy is the easy part. The real value shows up when something goes wrong. A roof claim, a fender bender, a liability question. That is when having someone who knows your policy, knows the carrier, and is willing to make calls on your behalf makes a real difference. Most people do not realize that until they need it.

My honest advice: do not choose an agency based on the first quote you receive. Choose based on how well the agent explains your options, how clearly they answer your questions about commissions, and whether they commit to reviewing your coverage every year. Those three things tell you more about the quality of the relationship than any single premium number.

— Mike

How Mfandtna can help you find the right coverage

Mfandtna is an independent insurance agency based in Arlington, MA, with over 30 years of experience helping individuals, families, and businesses find coverage that fits their needs and budget. The agency works with multiple carriers to deliver competitive quotes on home, auto, builders’ risk, and commercial insurance across Massachusetts and beyond.

When you work with Mfandtna, you get a licensed agent who compares real options across carriers, explains your choices clearly, and stays with you through claims and renewals. There is no pressure to accept the first number. The goal is coverage that makes sense for your life. Get started with a free insurance quote and see what the market actually offers for your situation.

FAQ

What is an independent insurance agency?

An independent insurance agency is a licensed insurance producer that works with multiple insurance companies to offer clients a range of coverage options. Unlike captive agents, independent agents are not tied to a single insurer and can compare policies across carriers on your behalf.

How does an independent agency differ from a captive agent?

A captive agent represents one insurance company and can only sell that company’s products. An independent agent contracts with multiple carriers, compares options side by side, and can move clients between carriers when a better fit becomes available.

Are independent insurance agents regulated?

Yes. Independent agents are licensed by state insurance commissions, subject to continuing education requirements, and governed by consumer protection rules. The NAIC oversees producer licensing standards across all U.S. states.

How do independent agents get paid?

Independent agents earn commissions from the premiums on policies they place and renew. Renewal commissions create a financial incentive for agents to maintain long-term client relationships and keep coverage current and appropriate.

What should I ask before choosing an independent insurance agency?

Ask how many carriers the agency works with, request a written comparison of at least two options, and confirm how the agency supports clients during claims. Verifying the agent’s license through your state insurance department is also a practical first step.