A homeowners insurance policy is a legal contract that defines exactly what your insurer will pay, under what conditions, and what it will not cover at all. Most homeowners never read it until a claim is denied. Knowing how to read homeowners insurance policy documents correctly means focusing on five key sections: the declarations page, insuring agreement, exclusions, conditions, and endorsements. The HO-3 special form is the most widely used policy format in the United States, covering roughly 78% of all homeowners. Understanding its structure puts you in control before a loss happens, not after.

What sections make up a homeowners insurance policy?

Every standard homeowners policy follows a predictable structure. Knowing what each section does tells you where to look for the information that matters most.

- Declarations page: The summary page listing your name, property address, coverage limits, deductibles, and premium. Think of it as the headline. The declarations page contains the five numbers that determine 95% of claim outcomes: dwelling limit, personal property limit, liability limit, loss of use limit, and deductible.

- Insuring agreement: The section where the insurer promises to pay for covered losses. It sets the conditions for indemnification.

- Exclusions: The section that lists what is not covered. This is where most claim surprises originate.

- Conditions: Your obligations as a policyholder, including how to report a claim, cooperate with investigations, and maintain the property.

- Endorsements: Attachments that change the base policy. They can add coverage, remove it, or modify how it applies.

- Definitions or glossary: Explains terms used throughout the policy. When a word appears in quotation marks in your policy, its meaning is controlled by this section.

The table below shows how each section affects your coverage outcome.

| Section | Primary function | Why it matters |

|---|---|---|

| Declarations page | Summarizes limits and deductibles | First stop for any coverage question |

| Insuring agreement | States what is covered | Sets the baseline promise |

| Exclusions | Lists what is not covered | Reveals the real coverage boundaries |

| Conditions | States policyholder duties | Violations can void a claim |

| Endorsements | Modifies the base contract | Can expand or restrict coverage |

How do coverage limits and deductibles actually work?

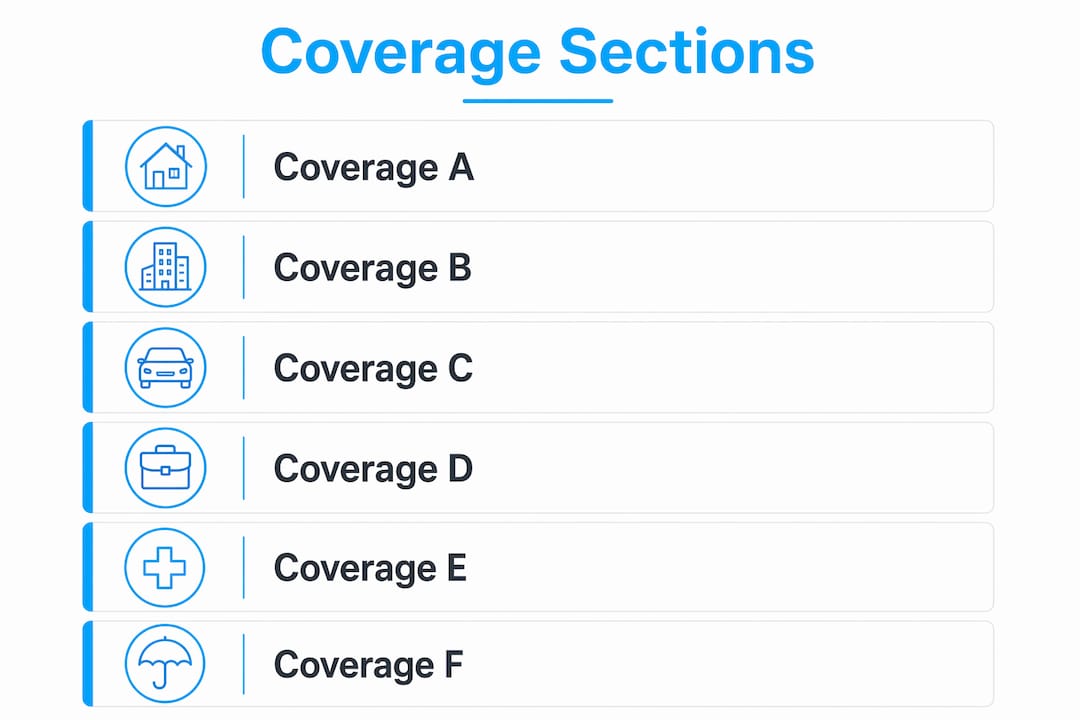

Standard homeowners policies divide coverage into six labeled sections, Coverage A through F. Each has a specific role and a typical dollar range tied to your dwelling value.

Coverage A (Dwelling) is the most critical number in your policy. It should reflect the full cost to rebuild your home at current labor and material prices, not its market value. Underinsuring here is the most expensive mistake homeowners make. Coverage B (Other Structures) covers detached garages, fences, and sheds, and is typically 10% of Coverage A. Coverage C (Personal Property) covers your belongings and usually runs 50–70% of Coverage A. Coverage D (Loss of Use) pays living expenses if you cannot occupy your home after a covered loss, typically 20–30% of Coverage A.

Coverage E (Personal Liability) protects you if someone is injured on your property and sues. Many standard policies set this at $100,000, but experts recommend $300,000 or higher. A serious injury claim can easily exceed $100,000 in medical bills and legal fees alone. Coverage F (Medical Payments) covers minor medical costs for guests injured on your property, regardless of fault.

Replacement cost vs. actual cash value

The loss settlement section of your policy tells you how a claim payout is calculated. This single distinction can change your check by tens of thousands of dollars. ACV vs. replacement cost wording creates a 40–70% variance in payouts on older homes. Actual Cash Value (ACV) pays what your property was worth at the time of loss, after depreciation. Replacement Cost pays what it actually costs to rebuild or replace it today. On a 20-year-old roof, the difference between ACV and replacement cost can be dramatic.

Pro Tip: Search your policy PDF for the phrase “loss settlement.” The paragraph that follows tells you whether you have ACV or replacement cost coverage. If it says “depreciation,” you have ACV.

Deductibles also come in two forms. A standard flat deductible (for example, $1,000 or $2,500) applies to most claims. A percentage deductible, often 1–2% of your dwelling value, applies specifically to wind, hail, or named-storm damage. On a $400,000 home, a 2% wind deductible means you pay the first $8,000 out of pocket before insurance contributes.

Why do exclusions and endorsements deserve your closest attention?

Exclusions define the real edges of your coverage. Standard policies exclude flood, earthquake, sewer backup, mold, wear and tear, pest damage, and business activity losses. Each of these is a common source of costly damage that homeowners assume is covered until a claim is denied.

Reading exclusions before the insuring agreement is the most practical approach. It lets you frame your coverage realistically rather than building false confidence from the broad promises in the insuring agreement. Here is what to look for:

- Flood and earthquake: Always excluded from standard policies. Both require separate policies or riders.

- Sewer or drain backup: Excluded by default but often available as an endorsement for a modest additional premium.

- Mold: Typically excluded unless caused by a covered peril like a sudden pipe burst.

- Wear and tear: Never covered. Maintenance failures are your responsibility.

- Business activity: Running a home-based business can void coverage for business property and liability.

- High-value personal property: Jewelry, art, and electronics often have sub-limits under Coverage C. A $5,000 jewelry collection may only receive $1,500 under a standard policy.

Endorsements are contract amendments, not summaries. Reading the full endorsement text is the only way to understand what changed. A label like “Water Backup Endorsement” sounds reassuring, but the actual text may limit coverage to $10,000 or exclude certain pipe types. Never rely on the endorsement title alone.

Pro Tip: Search your policy PDF for the words “water,” “backup,” “mold,” and “wear and tear.” Every paragraph those words appear in is a potential coverage gap worth discussing with your agent.

An extended replacement cost endorsement is one of the most valuable additions available. It increases dwelling coverage 20–25% above your stated limit, protecting you when construction costs spike after a major disaster.

How to read your homeowners policy step by step

Treat your policy as a risk map, not a document to read front to back. This focused method takes about 30–45 minutes and gives you a clear picture of your coverage.

- Start with the declarations page. Write down your five key numbers: dwelling limit, personal property limit, liability limit, loss of use limit, and your deductible(s). These numbers answer most coverage questions before you read another word.

- Go directly to the exclusions section. Mark every exclusion that applies to a realistic risk for your home. If you live near water, flag flood. If you are in a seismically active area, flag earthquake.

- Find the loss settlement section. Confirm whether your policy pays ACV or replacement cost for the dwelling and for personal property. These can differ within the same policy.

- Review the endorsements list. Read the full text of each endorsement, not just its title. Note any coverage limits, sub-limits, or conditions attached.

- Search for common claim drivers. Use your PDF search function for “water,” “mold,” “theft,” “collapse,” and “liability.” Each result shows you exactly how your policy handles that risk.

- Check personal property sub-limits. Find the schedule of special limits for jewelry, electronics, firearms, and cash. If any category is underinsured, a scheduled personal property rider can fix it.

- Write down your questions. Bring a specific list to your agent. Vague questions get vague answers. Specific questions get specific answers.

Common mistakes to avoid when reviewing your policy:

- Assuming “open perils” means everything is covered. Open perils coverage still has exclusions.

- Ignoring the conditions section. Failing to report a claim promptly or cooperate with an investigation can void your right to payment.

- Skipping endorsements because they look like fine print. Each one changes your contract.

- Never updating your coverage after a renovation. Adding a finished basement or new addition without updating Coverage A creates an underinsurance gap that shows up at claim time.

What coverage gaps should you address proactively?

Most homeowners discover gaps at the worst possible time: during a claim. Addressing them before a loss is far less expensive. Regular policy reviews with your agent are the most effective way to stay ahead of coverage gaps, especially after life changes or property improvements.

The most common gaps to check for:

- Flood coverage: The National Flood Insurance Program (NFIP) and private flood insurers offer standalone policies. Standard homeowners coverage never includes flood damage.

- Earthquake coverage: Required as a separate policy or endorsement in most states. California homeowners can access coverage through the California Earthquake Authority (CEA).

- Sewer backup: Inexpensive to add as an endorsement. Cleanup from a single backup event can cost thousands of dollars.

- Scheduled personal property: If you own jewelry, collectibles, or high-end electronics, a personal articles floater or rider removes the sub-limit and often covers accidental loss too.

- Liability limits: If your net worth exceeds your liability limit, you are exposed. A personal umbrella policy typically adds $1 million or more in liability coverage at a low annual cost.

- Home-based business: If you work from home, confirm whether your business equipment and any client liability are covered. Most standard policies exclude both.

Reviewing your home insurance coverage after any renovation, major purchase, or life change keeps your limits aligned with your actual exposure.

Key takeaways

Understanding your homeowners insurance policy requires focusing on the declarations page, exclusions, loss settlement terms, and endorsements. These four sections determine the outcome of nearly every claim.

| Point | Details |

|---|---|

| Start with the declarations page | Your five key numbers control 95% of claim outcomes. |

| Read exclusions before the insuring agreement | Exclusions reveal the real coverage boundaries, not the promises. |

| Know your loss settlement basis | ACV vs. replacement cost can create a 40–70% variance in your payout. |

| Read every endorsement in full | Endorsement titles are summaries. The text is the contract. |

| Review coverage after any major change | Renovations, new purchases, and life changes create gaps if limits are not updated. |

Why I think most homeowners read their policy backwards

After more than 30 years in the insurance business, I have seen the same pattern repeat. A homeowner files a claim, and the first time they read their policy is when they are sitting across from an adjuster. That is the worst possible time to learn what “wear and tear exclusion” means.

The instinct is to start at the beginning, read the insuring agreement, and feel reassured by the broad coverage language. The problem is that the exclusions section quietly takes back a significant portion of what the insuring agreement appears to give. Reading exclusions first is not pessimistic. It is accurate.

I also think homeowners underestimate how much endorsements matter. I have seen clients with a “Water Backup Endorsement” assume they had full protection, only to find the endorsement capped coverage at $5,000. The label sounded right. The text told a different story.

The most practical shift you can make is treating your policy as a living document. Review it every year, especially after a kitchen remodel, a new roof, or a significant purchase. The policy you bought three years ago may not reflect the home you live in today. A 30-minute annual review with your agent is the cheapest risk management tool available to you.

— Mike

How Mfandtna can help you review your coverage

Mfandtna has spent over 30 years helping homeowners in Massachusetts and beyond get coverage that actually matches their needs. If reading through your policy raises more questions than answers, that is exactly the kind of conversation Mfandtna is built for.

The team at Mfandtna reviews your existing policy, identifies gaps, and helps you compare options across multiple carriers. Whether you need to add a sewer backup endorsement, increase your liability limits, or rebuild your coverage from scratch, Mfandtna provides personalized guidance without pressure. Visit the homeowners insurance page to learn more, or request a free coverage quote to see what better protection looks like for your home.

FAQ

What is the HO-3 policy form?

The HO-3 is the most common homeowners insurance policy format in the United States, used by approximately 78% of homeowners. It provides open perils coverage for the dwelling and named perils coverage for personal property.

What is the difference between ACV and replacement cost?

Actual Cash Value pays the depreciated value of damaged property, while replacement cost pays what it costs to rebuild or replace it at current prices. The difference can create a 40–70% variance in your claim payout, particularly on older homes.

What does a homeowners policy typically exclude?

Standard policies exclude flood, earthquake, sewer backup, mold, wear and tear, pest damage, and business activity losses. Each of these requires a separate policy or endorsement to cover.

How much liability coverage do I actually need?

Many standard policies include $100,000 in personal liability coverage, but experts recommend a minimum of $300,000. If your assets exceed that amount, a personal umbrella policy adds cost-effective protection above your base limit.

How often should I review my homeowners insurance policy?

Review your policy at least once a year and after any major home renovation, significant purchase, or life change. Coverage limits that made sense three years ago may no longer match your home’s current rebuild cost or your personal asset exposure.