Builders risk soft costs coverage is defined as insurance protection for indirect, non-physical expenses that accumulate when a construction project faces delays caused by a covered peril. These costs, including construction loan interest, permit fees, and architectural fees, are not part of the physical structure but can drain a project’s budget just as fast. Standard builders risk insurance covers materials, equipment, and physical work in place. Soft costs protection fills the gap that base policies leave open. For property developers and contractors managing tight margins, that gap can determine whether a project stays viable or falls apart.

What types of expenses qualify as soft costs under builders risk insurance?

Soft costs in builders risk insurance are indirect, non-physical expenses that accrue during a delay caused by a covered peril such as fire, windstorm, or vandalism. They are distinct from hard costs, which cover the physical materials, labor, and equipment used to build the structure. Understanding which expenses qualify helps you avoid coverage gaps that can cost tens of thousands of dollars on a single project.

Common expenses that qualify as soft costs include:

- Construction loan interest: Additional interest charges that accrue because the project completion date has been pushed back.

- Real estate taxes: Property taxes that continue to accrue on the land or partially completed structure during the delay period.

- Permits and inspection fees: Re-application or renewal fees for permits that expire because of a covered delay.

- Architectural and engineering fees: Costs for redesign, re-inspection, or additional consultations required after a loss event.

- Legal and accounting fees: Professional fees tied directly to managing the delay, the claim, or contract renegotiations.

- Advertising and leasing costs: Pre-opening marketing expenses that must be repeated because the project’s launch date shifted.

- Project management costs: Fees for extended oversight of the project during the delay period.

These expenses accrue during delays caused by insured events and are reimbursable only when a covered peril triggers the delay. A delay caused by contractor error or poor scheduling does not qualify. The connection between the covered peril and the expense must be direct and documentable.

Pro Tip: Start a dedicated cost log on day one of your project. Record every soft cost category with dates, invoices, and contract references. If a covered loss occurs, this log becomes the backbone of your claim.

How is soft costs coverage structured and added to a policy?

Most builders risk policies do not include soft costs automatically. Coverage is added by endorsement, which is a separate attachment to the base policy that defines which soft costs are covered, up to what limit, and under what conditions. Without this endorsement, your base policy will pay to rebuild the physical structure but will not touch the loan interest or permit fees that pile up during the repair period.

Endorsements for soft costs typically come with sublimits. Default limits often start around $100,000 for soft costs including permits and loan insurance fees, but this amount may be insufficient for large commercial projects. You should calculate your projected soft costs based on your loan balance, expected permit fees, and professional retainer agreements before requesting a limit.

Adding a soft costs endorsement does affect your premium. Endorsements can increase premiums by 10–25%, but the protection they provide far outweighs the added cost on any project with significant financing. Builders risk insurance premiums typically range from 1% to 5% of the total construction budget, or roughly $100 to $300 per month depending on project type, location, and endorsements selected.

The underwriting process for soft costs endorsements requires documentation. Insurers will typically ask for:

- A project budget that itemizes anticipated soft costs by category.

- Loan agreements showing interest rates and outstanding balances.

- Copies of current permits and professional service contracts.

- A project timeline with milestone dates and expected completion.

- Any prior loss history on the developer’s or contractor’s account.

Variation by insurer is significant. Some carriers offer broad soft costs endorsements that cover nearly all indirect expenses. Others use narrow definitions that exclude certain fee categories. Read the endorsement language carefully before binding coverage.

Pro Tip: Negotiate sublimits based on your actual projected soft costs, not the insurer’s default. Ask your agent to run a scenario where the project is delayed by 90 days and calculate the total indirect cost exposure. Use that number as your minimum sublimit.

| Coverage Feature | Base Builders Risk Policy | Soft Costs Endorsement |

|---|---|---|

| Physical materials and equipment | Covered | Not applicable |

| Construction loan interest | Not covered | Covered |

| Permit and inspection fees | Not covered | Covered |

| Architectural and engineering fees | Not covered | Covered |

| Legal and accounting fees | Not covered | Covered |

| Premium impact | Base rate | Additional 10–25% |

How to secure and use soft costs coverage effectively

Securing soft costs protection starts before you submit your insurance application. The steps below walk you through the full process from pre-application to claims resolution.

- Assess your soft cost exposure. Review your construction loan documents, professional service contracts, and permit schedules. Total the indirect costs you would face if the project were delayed by 60 to 90 days.

- Request the endorsement explicitly. When working with your insurance agent, ask specifically for a soft costs endorsement. Do not assume it is included in a standard builders risk quote.

- Review the endorsement language. Confirm that the policy lists each covered expense category by name. Vague language like “other indirect costs” creates disputes at claim time.

- Set an appropriate sublimit. Base your requested sublimit on the exposure calculation from step one. Review the application process details to understand how insurers evaluate these requests.

- Maintain real-time records. Keep invoices, bank statements, and correspondence organized by date and expense category throughout the project.

- Notify your insurer immediately after a covered loss. Prompt notification preserves your rights and gives the insurer time to assign an adjuster before costs escalate.

- Submit a structured claim package. Include a timeline of the delay, a categorized list of soft costs incurred, and supporting documentation for each line item.

Common mistakes that derail soft costs claims include poor documentation, waiting too long to notify the insurer, and exceeding sublimits without prior authorization. Exceeding a sublimit without insurer approval is one of the fastest ways to have a portion of your claim denied.

- Avoid mixing personal or unrelated business expenses with project-specific soft costs in your records.

- Do not authorize additional professional fees after a loss without confirming coverage with your insurer first.

- Keep a written log of all communications with your insurer, adjuster, and legal counsel after a loss event.

Pro Tip: Assign one person on your team to manage all post-loss documentation. Fragmented records across multiple team members are the leading cause of incomplete claim submissions.

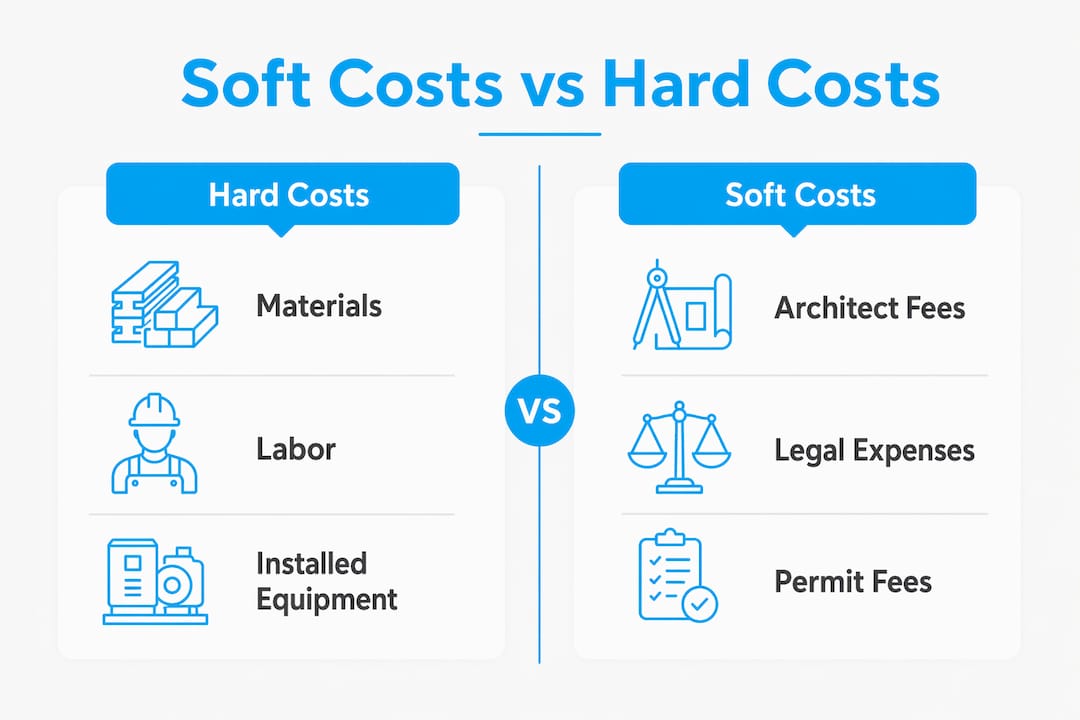

Soft costs coverage vs. other builders risk protections

Hard costs in builders risk insurance cover direct construction expenses: lumber, concrete, steel, labor, and installed equipment. Soft costs cover the indirect expenses that run in the background. Both are necessary for full project protection, but they operate under different policy mechanisms.

Delay in Start-Up (DSU) coverage, sometimes called business income coverage for construction projects, is a related but distinct product. DSU covers lost revenue or profit that the completed project would have generated, starting from the original planned opening date. Soft costs coverage reimburses expenses already incurred. DSU compensates for income not yet earned. A developer building a commercial rental property may need both.

| Coverage Type | What It Covers | Trigger | Typical Limit Basis |

|---|---|---|---|

| Hard costs (base policy) | Physical materials, labor, equipment | Direct physical loss | Total construction value |

| Soft costs endorsement | Loan interest, permits, professional fees | Covered peril causing delay | Projected indirect cost exposure |

| Delay in Start-Up (DSU) | Lost revenue from delayed project opening | Covered peril causing delay | Projected income during delay |

| General liability | Third-party bodily injury and property damage | Occurrence during construction | Per-occurrence and aggregate limits |

Contractors working on projects with significant pre-leasing agreements or forward sale contracts should evaluate DSU coverage alongside soft costs protection. The two products together address both the cost side and the revenue side of a delay event.

Troubleshooting common claims issues with soft costs coverage

Claims disputes involving soft costs are more common than most developers expect. The most frequent source of conflict is ambiguous policy language around which expenses qualify and whether mitigation costs fall within the endorsement’s scope.

Key issues that trigger disputes include:

- Mitigation and expediting costs: Insurers may deny reimbursement for overtime labor or expedited material shipping if these costs are not clearly tied to shortening the delay period.

- Sublimit exhaustion: Once a sublimit is reached, the insurer stops paying regardless of additional qualifying expenses. Developers who underestimate their exposure face this problem frequently.

- Expense categorization: An expense labeled “project management” may be covered under one policy and excluded under another, depending on how the endorsement defines the category.

- Timing of documentation: Expenses incurred before formal loss notification are harder to recover, even when they are directly tied to the covered event.

“Claims disputes hinge on whether incremental spending for mitigation qualifies under soft costs sublimits. Insurers may deny expenses if they are not clearly tied to shortening project delays or if they fall outside endorsement definitions.” — Advise & Consult, Inc.

Pre-claim alignment with your insurer is the most effective way to prevent these disputes. Before authorizing any mitigation spending after a loss, contact your insurer and get written confirmation that the planned expenditure falls within your coverage. This one step prevents the majority of sublimit denial disputes.

Pro Tip: If a dispute arises, engage a public adjuster or construction insurance attorney early. Waiting until the insurer issues a formal denial makes resolution significantly harder and more expensive.

Key Takeaways

Builders risk soft costs coverage is an endorsement, not a base policy feature, and its value depends entirely on how well you document costs and align with your insurer before and after a loss.

| Point | Details |

|---|---|

| Soft costs require an endorsement | Base builders risk policies do not cover indirect expenses; you must add a soft costs endorsement explicitly. |

| Sublimits drive your exposure | Default sublimits may start around $100,000; calculate your actual exposure and request a matching limit. |

| Documentation is non-negotiable | Real-time records of every indirect expense are required to support a successful claim. |

| Mitigation costs need pre-approval | Confirm with your insurer before spending on expediting or overtime to avoid denial at claim time. |

| DSU coverage fills the revenue gap | Soft costs cover expenses already incurred; Delay in Start-Up coverage addresses lost income from a delayed opening. |

Why soft costs coverage is the most underestimated line on a construction policy

I have reviewed hundreds of builders risk policies over the years, and the soft costs endorsement is the one line item developers consistently undervalue until they need it. A fire that sets a project back four months does not just cost you the rebuild. It costs you four months of loan interest on a $3,000,000 construction draw, re-permit fees, extended architect retainers, and the marketing budget you spent on a launch date that no longer exists. None of that shows up in a hard costs claim.

The industry challenge I see most often is developers who request the endorsement but accept the insurer’s default sublimit without question. A $100,000 sublimit sounds substantial until you calculate 120 days of interest on a large commercial loan. The math closes fast. Proactive policy review, done before the project breaks ground, is the only way to set a sublimit that actually matches your exposure.

Insurer practices around soft costs are also evolving. More carriers are tightening endorsement language to exclude mitigation costs unless they are pre-approved in writing. That shift puts the burden squarely on the developer and contractor to communicate early and document everything. The developers I have seen navigate claims successfully treat their insurer as a project partner from day one, not as an adversary they call after a loss.

Treat soft costs coverage as a core part of your project finance plan, not an afterthought on your insurance checklist. The premium increase is modest. The protection is not.

— Mike

Mfandtna can help you build the right coverage

Protecting a construction project means covering more than just the physical structure. Indirect costs from delays can threaten a project’s financial viability just as much as physical damage.

Mfandtna specializes in builders risk insurance in Boston and the surrounding Massachusetts area, with over 30 years of experience helping developers and contractors build policies that include the right soft costs endorsements, appropriate sublimits, and clear coverage terms. The team at Mfandtna works with you to assess your actual indirect cost exposure and match it to a policy that holds up at claim time. Request a free quote today and get a builders risk policy structured around your project, not a generic template.

FAQ

What is builders risk soft costs coverage?

Builders risk soft costs coverage is an endorsement added to a standard builders risk policy that reimburses indirect, non-physical expenses such as loan interest, permits, and professional fees that accrue when a covered peril delays a construction project.

Are soft costs automatically included in builders risk insurance?

Most builders risk policies do not include soft costs automatically. Coverage must be added by endorsement, and specific sublimits and terms apply depending on the insurer and project details.

What is the difference between hard costs and soft costs in builders risk?

Hard costs cover direct construction expenses like materials, labor, and installed equipment. Soft costs cover indirect expenses tied to financing, permits, and professional fees that accumulate during a project delay caused by a covered peril.

How much does a soft costs endorsement increase my premium?

Adding a soft costs endorsement typically increases a builders risk premium by 10–25%. The base premium for builders risk insurance generally ranges from 1% to 5% of the total construction budget.

What causes soft costs claims to be denied?

The most common reasons for denial include ambiguous policy language, expenses that exceed the endorsement sublimit, and mitigation costs that were not pre-approved by the insurer before being incurred.