Spec home insurance is defined as a two-phase coverage system: builder’s risk insurance during construction and a standard homeowners policy once the property is complete. Most homeowners and real estate investors focus on the finished product and miss the critical handoff between these two phases. That gap costs money. Understanding spec insurance basics before you break ground or sign a closing contract is the single most important step you can take to protect your investment.

What is spec home insurance and how does it work?

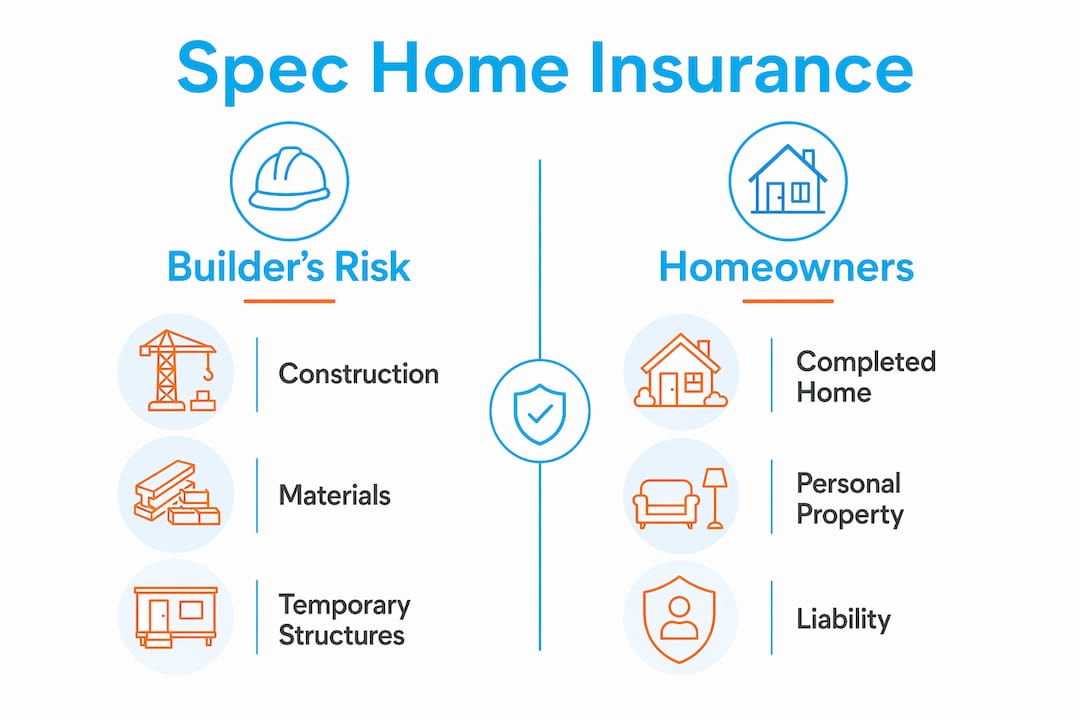

Spec home insurance covers a speculative home, meaning a property built for resale rather than for a specific buyer. The industry term you will hear most often is “builders risk insurance” for the construction phase, followed by a standard homeowners policy at completion. These two policies cover entirely different risks, and neither one automatically transitions into the other.

Builder’s risk insurance protects the structure, materials on site, and temporary structures during active construction. Once the project is complete and ownership transfers, builders risk coverage ends immediately. A homeowners policy must be active at that exact moment to avoid any uninsured period. This is not a technicality. It is the central risk in spec home insurance coverage considerations.

What coverage does builder’s risk insurance provide for spec homes?

Builder’s risk insurance protects the physical structure and materials from the first day of construction through project completion. Coverage typically applies on an “open perils” basis, meaning it covers all causes of loss unless specifically excluded. Named-peril policies exist but offer narrower protection and are less common for spec builds.

The policy term is typically 12 months, and insurers require formal notification if construction delays exceed 30 days. Missing that notification can trigger policy cancellation. That is a risk most developers do not anticipate until it is too late.

Coverage under a standard builders risk policy includes:

- The structure itself, including framing, roofing, and exterior finishes

- Building materials stored on site or in transit

- Temporary structures like scaffolding and site offices

- Damage from fire, wind, theft, vandalism, and certain water events

- Soft costs in some policies, such as architect fees after a covered loss

Builder’s risk does NOT cover:

- Faulty workmanship or design errors

- Employee theft

- Damage that occurs before construction begins or after completion

- General liability for injuries on the construction site (that falls under the contractor’s general liability policy, which covers third-party bodily injury and property damage claims)

Builder’s risk premiums range from 1% to 4% of the completed project value. On a $500,000 spec home, that means annual premiums between $5,000 and $20,000 depending on location, construction type, and coverage scope.

Pro Tip: Set your builder’s risk coverage limit at the projected completed value of the home, not the current construction cost. This protects you against mid-build losses when the structure is partially complete but materials are already on site.

How does homeowners insurance differ from builder’s risk for a completed spec home?

Once construction ends and the property transfers to a buyer, a standard homeowners insurance policy takes over. This policy covers an occupied dwelling, not a structure under development. The two policies serve completely different purposes and cannot substitute for each other.

A standard homeowners policy is organized into Coverage A through F:

| Coverage | What it protects |

|---|---|

| Coverage A: Dwelling | The physical structure of the home |

| Coverage B: Other structures | Detached garages, fences, sheds |

| Coverage C: Personal property | Furniture, electronics, clothing |

| Coverage D: Loss of use | Additional living expenses if the home is uninhabitable |

| Coverage E: Personal liability | Legal costs if someone is injured on your property |

| Coverage F: Medical payments | Medical bills for guests injured on your property |

One of the most consequential decisions in a homeowners policy is choosing between actual cash value and replacement cost coverage. Replacement cost pays to rebuild without applying depreciation, while actual cash value deducts for age and wear. For a brand-new spec home, replacement cost is the correct choice. The payout difference can be significant.

Spec homes with premium finishes present another challenge. High-value homes often require endorsements to cover custom flooring, imported stone countertops, specialty cabinetry, and other materials that a standard policy will not fully reimburse. If your spec home includes upgrades above standard builder-grade finishes, a standard homeowners policy likely underinsures it.

Pro Tip: Ask your agent to run a replacement cost estimator on the finished spec home before binding the homeowners policy. Builder-grade estimates often miss the true cost of custom materials.

What are common coverage gaps in spec home insurance?

The most dangerous gap in spec home insurance occurs at the closing table. Spec home developers carry blanket builder’s risk policies that terminate the moment ownership transfers. If your homeowners policy is not active at that exact moment, the property is uninsured. Even a one-day lapse leaves you fully exposed.

“Scheduling insurance coverage to avoid lapses at closing is one of the most overlooked yet critical insurance management tasks for spec home buyers.” — Home Insurance Authority

Other coverage gaps that catch buyers off guard include:

- Detached structures: A detached garage or workshop may need separate coverage under Coverage B if the limit is too low.

- Custom finishes: Imported tile, specialty hardware, and custom millwork often exceed standard policy limits without a scheduled endorsement.

- Contents coverage: A spec home sold furnished needs personal property coverage from day one.

- Rebuild cost volatility: Labor and material costs fluctuate sharply. A policy written at today’s rebuild cost may fall short after a loss six months later.

Guaranteed replacement cost coverage addresses that last point directly. Extended replacement cost endorsements can cover 125% to 150% of the Coverage A limit, giving you a buffer when construction costs spike between policy issuance and a covered loss. For new spec homes, this endorsement is not optional. It is a necessity.

Coordinate with your insurance agent at least two weeks before closing. Confirm the exact date and time the builder’s risk policy terminates. Bind your homeowners policy to start simultaneously. This single step prevents the most common and costly mistake in spec home insurance.

How do cost factors and location influence spec home insurance premiums?

Several variables drive the cost of both builder’s risk and homeowners insurance for spec homes. Understanding them helps you budget accurately and identify where you can reduce premiums without cutting coverage.

- Construction type and materials. Wood-frame construction costs more to insure than steel or concrete. Fire-resistant materials lower risk and reduce premiums.

- Location and local hazards. Homes in flood zones, wildfire corridors, or high-crime areas carry higher premiums. Coastal properties in Massachusetts, for example, face wind and water exposure that inland builds do not.

- Project scope and timeline. Larger projects with longer build times carry more exposure. Builder’s risk premiums between 1% and 4% of completed value mean a $1 million spec home costs $10,000 to $40,000 annually to insure during construction.

- High-value finishes. Custom materials raise the replacement cost, which raises the homeowners premium. A spec home with $150,000 in premium finishes needs a policy that reflects that value.

- Loss prevention features. Security systems, leak detection, and updated plumbing can earn premium discounts on homeowners insurance. Smart home monitoring systems are increasingly recognized by insurers as risk-reduction tools.

The types of homeowners coverage you select also affect your final premium. Replacement cost coverage costs more than actual cash value, but the payout difference after a total loss justifies the higher premium on a new construction.

Key takeaways

Spec home insurance requires two separate policies at two distinct stages, and the transition between them is where most coverage failures happen.

| Point | Details |

|---|---|

| Two-phase coverage | Builder’s risk covers construction; homeowners insurance covers the completed, occupied property. |

| Policy transition risk | Builder’s risk ends at closing; bind your homeowners policy to start at the same moment. |

| Replacement cost coverage | Choose replacement cost over actual cash value to avoid shortfalls when rebuilding a new spec home. |

| Custom finishes need endorsements | Standard homeowners policies often underinsure high-value materials; schedule specialty items separately. |

| Premium range for builder’s risk | Expect to pay 1%–4% of the completed project value annually during the construction phase. |

What I have learned after years of spec home insurance cases

Spec home insurance is one of those topics where the gap between what people assume and what is actually true costs real money. I have seen buyers walk into closing confident their coverage was handled, only to discover the builder’s risk policy terminated at noon and their homeowners policy did not start until the following business day. That 18-hour window left a $700,000 property completely uninsured.

The other mistake I see constantly is underinsuring custom finishes. A spec home with $80,000 in kitchen upgrades and $40,000 in custom flooring is not a standard home. A standard homeowners policy treats it like one. The claim settlement after a kitchen fire will not cover what it actually costs to rebuild to the original spec.

My honest recommendation: start the insurance conversation before the foundation is poured, not the week before closing. Get your builder’s risk policy in place on day one of construction. Then, about 30 days before your projected closing date, work with your agent to structure the homeowners policy so it activates the moment the deed transfers. Ask specifically about guaranteed replacement cost and whether your custom materials need scheduled endorsements.

The coverage gaps in homeowners policies are predictable. They are also entirely avoidable with the right planning.

— Mike

Spec home insurance coverage from Mfandtna

Mfandtna has spent over 30 years helping homeowners and real estate investors in Massachusetts and beyond get the right coverage at every stage of a property’s life. Whether you are mid-construction or days away from closing on a finished spec home, the team at Mfandtna can review your current coverage, identify gaps, and structure a policy that matches your actual rebuild cost and finish specifications.

Get a free insurance quote and speak directly with an agent who understands both the construction phase and the homeowners transition. Mfandtna also offers dedicated builders risk insurance for spec home developers who need coverage from groundbreaking through sale. No generic policies. No coverage surprises at closing.

FAQ

What is spec home insurance?

Spec home insurance is a two-phase coverage approach: builder’s risk insurance during construction and a standard homeowners policy after the property is complete and ownership transfers.

When does builder’s risk insurance end on a spec home?

Builder’s risk insurance terminates at the moment of closing when ownership transfers to the buyer. The buyer’s homeowners policy must be active at that exact moment to avoid an uninsured gap.

Do I need replacement cost coverage on a new spec home?

Yes. Replacement cost coverage pays to rebuild without depreciation deductions. For a new spec home, actual cash value coverage will almost always pay out less than the true cost to rebuild.

Are custom finishes covered under a standard homeowners policy?

Standard homeowners policies often do not fully cover specialty materials like imported stone, custom cabinetry, or premium flooring. You need scheduled endorsements or a high-value home policy to cover those items at their true replacement cost.

How much does builder’s risk insurance cost for a spec home?

Builder’s risk premiums typically range from 1% to 4% of the completed project value annually, depending on location, construction type, and coverage scope.