Builders risk insurance is defined as temporary, first-party property coverage that protects buildings under construction, renovation materials, and on-site equipment from physical loss or damage. Property owners and developers who carry a financial interest in a construction project need this coverage from day one. Standard homeowners or commercial property policies do not fill this gap. The National Association of Surety Bond Producers (NASBP) recognizes builders risk as a distinct and specialized insurance category, separate from general liability or permanent property coverage. Without it, a single fire, theft event, or windstorm can erase months of investment before a project ever reaches completion.

What is builders risk insurance and what does it cover?

Builders risk insurance covers buildings under construction, materials stored on site, and equipment intended to become part of the finished structure. That includes framing lumber, roofing materials, installed fixtures, and temporary structures like scaffolding. The policy activates the moment materials arrive on site and stays in force throughout the build.

Covered perils typically include fire, theft, vandalism, wind, lightning, hail, and vehicle damage. That list covers the most common causes of construction loss. A framing fire, a break-in that strips copper wiring, or a hailstorm that destroys a partially completed roof are all scenarios a builders risk policy addresses directly.

Builders risk policies operate on an all-risk coverage basis. That means coverage applies to any cause of loss unless the policy specifically excludes it. This is broader than a named-peril policy, which only pays for losses from a listed set of causes.

Exclusions still matter. Common ones include:

- Floods and surface water damage

- Earthquakes and earth movement

- Faulty workmanship or design errors

- Employee theft

- Mechanical breakdown

Pro Tip: Add a flood endorsement if your project sits in a FEMA-designated flood zone. Standard builders risk policies exclude flood damage, and that gap can be costly in coastal or low-lying areas.

How long does builders risk coverage last?

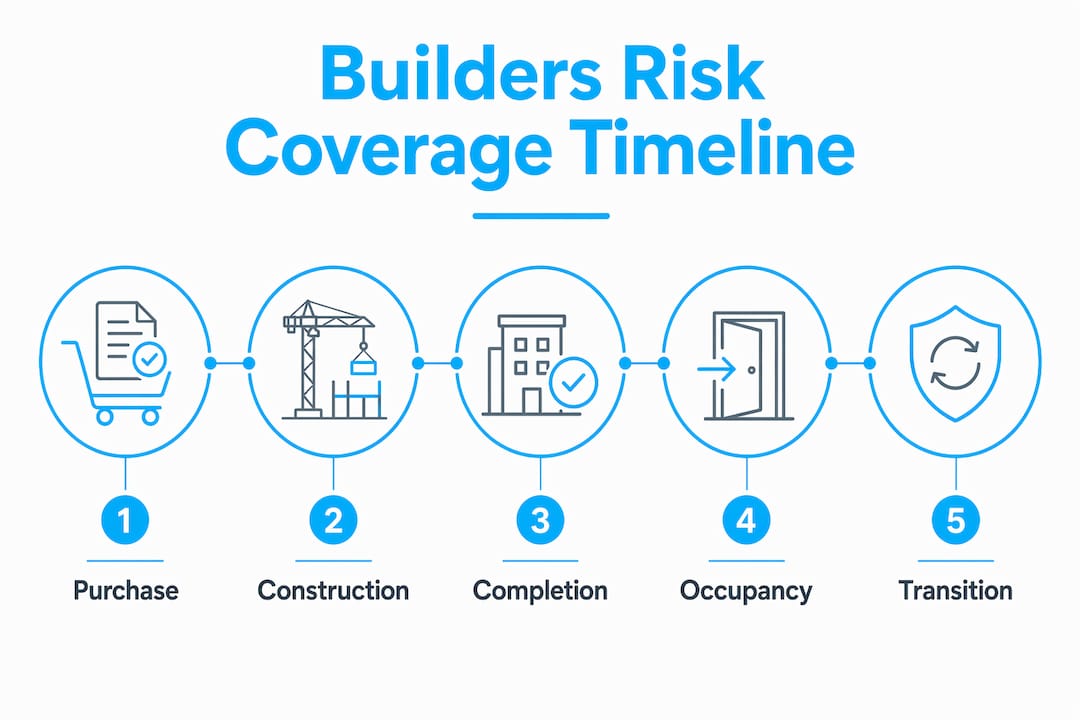

Builders risk coverage is temporary by design. Coverage must be active before materials arrive on site, not after the first wall goes up. Waiting even a few days creates an uninsured window that most developers do not realize exists until a loss occurs.

The policy ends automatically when one of these milestones happens:

- The project reaches substantial completion

- The building is occupied, even partially

- The property is sold and the closing is finalized

- The policy term expires without a renewal

Coverage terminates on occupancy or project completion, requiring a transition to permanent homeowners or commercial property insurance. That transition must be planned in advance. A gap of even one week between builders risk expiration and a new permanent policy leaves the property fully exposed.

Timing is the most overlooked part of builders risk management. Developers who run projects on tight schedules sometimes let coverage lapse during punch-list phases, assuming the hard risk is behind them. A fire or theft during finishing work can still cause significant losses. Coordinate your policy end date with your project manager and your insurance agent well before the final inspection.

Who buys builders risk insurance and who should be covered?

Purchasing responsibility is set by contract, not by a universal rule. The construction contract between the owner and general contractor specifies who must purchase the policy. Failing to verify this before the project starts creates coverage disputes that are difficult to resolve after a loss.

The property owner generally holds the policy because they control the insured property and have the right to direct how insurance proceeds are used. When a contractor holds the policy instead, disputes can arise over how claim payments are applied, especially if the owner-contractor relationship deteriorates mid-project.

All parties with a financial interest in the project should be named on the policy. That typically includes:

- The property owner

- The general contractor

- Subcontractors with significant on-site exposure

- The lender, if the project is financed

Lender-required builders risk is a real compliance issue. Most construction lenders require proof of builders risk coverage before releasing funds. Lender-required builders risk compliance means the policy must meet specific coverage minimums, name the lender as an additional insured, and remain in force for the full loan term. Missing any of these conditions can trigger a loan default clause.

Pro Tip: Ask your lender for their builders risk requirements in writing before you bind coverage. Some lenders have specific carrier rating requirements or minimum coverage limits that standard policies do not automatically meet.

How does builders risk differ from other construction insurance?

Builders risk and contractors general liability insurance cover completely different risks. Builders risk strictly protects property damage, not liability claims. General liability covers bodily injury and property damage caused to third parties. If a subcontractor falls on site, general liability responds. If a fire destroys the framing, builders risk responds.

Standard commercial property policies exclude structures under construction. This surprises many first-time developers who assume their existing business property policy extends to a new build. It does not. The gap between commercial property coverage and builders risk is one of the most common and expensive misconceptions in construction risk management.

| Coverage type | What it protects | What it excludes |

|---|---|---|

| Builders risk | Property under construction, materials, equipment | Liability, floods, faulty workmanship |

| Contractors general liability | Third-party injury and property damage | First-party property loss |

| Commercial property | Completed, occupied structures | Structures under active construction |

| Workers compensation | Employee injury on the job | Property damage of any kind |

Each policy fills a specific slot. Builders risk is the one that protects your actual investment in the structure while it is being built. The others protect against liability, employee injury, or completed property. You need all of them, but builders risk is the one most often missing from a developer’s coverage stack.

Key considerations when securing builders risk coverage

Getting the right builders risk policy requires more than picking a coverage limit. The policy coverage scope must match the actual project, including its timeline, location, and construction method. A policy written for a six-month build does not automatically extend if the project runs long.

Key steps to take before binding coverage:

- Read the construction contract and identify who is required to purchase the policy

- Confirm lender-required builders risk compliance requirements in writing

- Match the coverage limit to the completed project value, not just the construction cost

- Review exclusions and add endorsements for flood, earthquake, or soft costs if needed

- Set the policy start date to coincide with the first material delivery, not the groundbreaking

Coordinating coverage timing closely with project milestones prevents uninsured gaps. Builders risk costs typically run about 1%–5% of the total construction budget. That range reflects project size, location, and risk profile. For most developers, that cost is a fraction of what a single uninsured loss would set back the project.

Pro Tip: Work with an insurance agent who specializes in construction coverage. Builders risk policies are not standardized, and the differences between carriers on exclusions, sublimits, and endorsement options are significant. A generalist agent may miss coverage gaps that a specialist catches immediately.

The role of insurance in construction goes beyond compliance. It protects the financial viability of the entire project. A well-structured builders risk policy, combined with general liability and workers compensation, gives property owners and developers a complete risk management foundation.

Key takeaways

Builders risk insurance is the only policy specifically designed to protect a construction project’s physical assets from the first material delivery through project completion.

| Point | Details |

|---|---|

| Temporary, specialized coverage | Builders risk protects property under construction and ends automatically at occupancy or sale. |

| All-risk basis with exclusions | Coverage applies unless excluded, but floods, earthquakes, and faulty workmanship are commonly excluded. |

| Contract determines who buys | The construction contract specifies whether the owner or contractor purchases the policy. |

| Lender compliance is mandatory | Lenders require builders risk as a loan condition, with specific coverage minimums and named insured requirements. |

| Timing is critical | Coverage must start before materials arrive and transition to permanent insurance without any gap. |

Why builders risk is the coverage most developers underestimate

After working in construction insurance for years, I have seen one pattern repeat itself more than any other. Developers who are meticulous about budgets, timelines, and contractor vetting treat insurance as an afterthought. They buy a policy the week before the groundbreaking, skip the exclusion review, and assume the coverage matches the project. It rarely does.

The most painful losses I have seen were not caused by catastrophic events. They were caused by timing gaps. A developer lets the policy lapse two weeks before the certificate of occupancy because the project “is basically done.” Then a pipe burst or a break-in happens during the final walkthrough. No coverage. The entire finishing phase is out of pocket.

My honest advice is this: treat builders risk as a project management task, not just an insurance task. Put the policy start date, renewal dates, and termination triggers on your project schedule alongside your framing inspection and final walkthrough. Verify the insurance regulations for your project before you sign the construction contract, not after. And name every party with a financial stake on the policy from day one.

Builders risk is not expensive relative to what it protects. The developers who skip it or underinsure are not saving money. They are self-insuring a risk they have not priced or planned for.

— Mike

Mfandtna’s builders risk insurance expertise

Mfandtna has spent over 30 years helping property owners and developers in Massachusetts and beyond secure the right coverage for construction projects of every size.

Whether you are managing a residential renovation or a large commercial build, Mfandtna’s team understands the contract requirements, lender compliance standards, and coverage gaps that matter most. Getting the right builders risk insurance policy means matching coverage to your specific project timeline, location, and risk profile. Mfandtna does that work with you, not for you in a one-size-fits-all way. Reach out for a personalized coverage review and make sure your next project is protected from the first nail to the final inspection.

FAQ

What is builders risk insurance in simple terms?

Builders risk insurance is temporary property coverage that protects a building under construction, along with its materials and equipment, from damage caused by fire, theft, wind, and similar perils. It ends when the project is complete or the property is occupied.

Does builders risk insurance cover faulty workmanship?

No. Builders risk policies exclude faulty workmanship, design errors, and mechanical breakdown. The policy covers physical damage from external causes, not defects in the construction itself.

Who is required to carry builders risk insurance?

The construction contract defines who must purchase the policy, typically the property owner or the general contractor. Lenders also require builders risk as a condition of construction financing, with specific coverage minimums and named insured requirements.

How much does builders risk insurance cost?

Builders risk insurance typically costs about 1%–5% of the total construction budget, depending on project size, location, and risk profile. Most developers pay between $1,000 and $5,000 annually for standard projects.

When does builders risk insurance end?

Coverage ends automatically when the project reaches substantial completion, when the building is occupied, or when the property is sold. At that point, the owner must transition to a permanent homeowners or commercial property policy to maintain protection.